Poland Today Business Review+ No. 013

18

No. 013 / 2nd December 2013 / www.poland-today.pl / magazine, conferences, portal, newsletter 1 year subscription: EUR 690 (PLN 2760) Newsletter Editor: Lech Kaczanowski [email protected] tel. +48 607 079 547 Sales Contact: James Anderson-Hanney [email protected] tel. +48 881 650 600 MANUFACTURING & PROCESSING Portuguese adhesives maker Colquimica sets up shop near Poznań page 2 BANKING & FINANCE Santander Consumer Bank to become part of BZ WBK Group page 2 Regulator objects to BPH TFI takeover by Investors Holding & Abris Capital page 3 PROPERTY & CONSTRUCTION HB Reavis signs major office lease and secures financing for Warsaw projects page 5 New business park in Katowice to be Skanska's largest office project in Poland to-date page 6 SERVICES & BPO Finnish Barona brings Nordic staff to Polish outsourcing centers page 7 TRANSPORT & LOGISTICS Szymany airport project one step closer to becoming reality page 10 CONSUMER GOODS & RETAIL Balmain & NBGI building EUR 25m retail project in Starachowices page 11 Textile discounter KiK to speed up expansion in Poland next year page 12 HEALTHCARE & PHARMA US medical equipment company enters Warsaw bourse page 13 POLITICS & ECONOMY Official Q3 GDP figures show modest recovery in consumption and investments page 14 KEY FIGURES Up-to-date macroeconomic figures, currency & stock market data and lots of other hard-to-find info pages 16-18 San Leon said the result of Lewino refracking "exceeded expectations." Photo: San Leon Shale gas production to launch in 2014 Shale gas production to launch in 2014 Shale gas production to launch in 2014 Shale gas production to launch in 2014 Poland will likely begin commercial extraction of shale gas in 2014, announced deputy Environment Minister Piotr Woźniak at last week's "Shale Gas World Europe" conference in Warsaw, citing a successful fracking by upstream firm San Leon. page 4 Train manufacturer Train manufacturer Train manufacturer Train manufacturer Newag goes public Newag goes public Newag goes public Newag goes public One of Poland's leading rail stock maintenance and production firms Newag has successfully closed a PLN 400m IPO on the Warsaw Stock Exchange. Newag's owners sold 43% of shares in the Nowy Sącz-based company. page 9

-

Upload

poland-today-business-review -

Category

Documents

-

view

220 -

download

3

description

Poland Today's Business Review+ newsletter is your indispensable weekly English-language resource for business in Poland – providing essential news, unique interviews, revealing data and insightful analysis.

Transcript of Poland Today Business Review+ No. 013

No. 013 / 2nd December 2013 / www.poland-today.pl / magazine, conferences, portal, newsletter

1 year subscription: EUR 690 (PLN 2760)

Newsletter Editor: Lech Kaczanowski

tel. +48 607 079 547

Sales Contact: James Anderson-Hanney

tel. +48 881 650 600

MANUFACTURING & PROCESSING

Portuguese adhesives maker Colquimica sets up shop near Poznań page 2

BANKING & FINANCE

Santander Consumer Bank to become part of BZ WBK Group page 2 Regulator objects to BPH TFI takeover by Investors Holding & Abris Capital page 3

PROPERTY & CONSTRUCTION

HB Reavis signs major office lease and secures financing for Warsaw projects page 5

New business park in Katowice to be Skanska's largest office project in Poland to-date page 6

SERVICES & BPO

Finnish Barona brings Nordic staff to Polish outsourcing centers page 7

TRANSPORT & LOGISTICS

Szymany airport project one step closer to becoming reality page 10

CONSUMER GOODS & RETAIL

Balmain & NBGI building EUR 25m retail project in Starachowices page 11 Textile discounter KiK to speed up expansion in Poland next year page 12

HEALTHCARE & PHARMA

US medical equipment company enters Warsaw bourse page 13

POLITICS & ECONOMY

Official Q3 GDP figures show modest recovery in consumption and investments page 14

KEY FIGURES

Up-to-date macroeconomic figures, currency & stock market data and lots of other hard-to-find info pages 16-18

San Leon said the result of Lewino refracking "exceeded expectations." Photo: San Leon

Shale gas production to launch in 2014Shale gas production to launch in 2014Shale gas production to launch in 2014Shale gas production to launch in 2014 Poland will likely begin commercial extraction of shale gas in 2014, announced deputy Environment Minister Piotr Woźniak at last week's "Shale Gas World Europe" conference in Warsaw, citing a successful fracking by upstream firm San Leon. page 4

Train manufacturerTrain manufacturerTrain manufacturerTrain manufacturer Newag goes publicNewag goes publicNewag goes publicNewag goes public One of Poland's leading rail stock maintenance and production firms Newag has successfully closed a PLN 400m IPO on the Warsaw Stock Exchange. Newag's owners sold 43% of shares in the Nowy Sącz-based company. page 9

weekly newsletter # 013 / 2nd December 2013 / page 2

MANUFACTURING & PROCESSING

Portuguese adhesives Portuguese adhesives Portuguese adhesives Portuguese adhesives maker Colquimica sets maker Colquimica sets maker Colquimica sets maker Colquimica sets up shop near Poznańup shop near Poznańup shop near Poznańup shop near Poznań

Portuguese producer of industrial adhesives Colquimica has established its first production unit in Eastern Europe at SEGRO Logistics Park Poznań. With an annual production capacity of 10,000 tons, the factory has been fully operational since late Novem-ber, producing a range hot-melt adhesives used in per-sonal hygiene and food packaging industry. "Our aim was to increase the quality of services we of-fer our customers in the region as well as optimize lo-gistics in Poland and neighboring countries. SEGRO Logistics Park Poznań offers appropriate infrastruc-ture and perfect location between Berlin and Moscow, one that also ensures access to qualified workforce. We have plans to further ramp up the production ca-pacity in the middle of 2014,"says João Pedro Koehler CEO Colquimica. Colquimica has rented rent 3,500 sq.m in one of SEGRO Logistics Park Poznań's buildings, including nearly 2,000 sq.m of warehouse space, a 1,100 sq m of production area space as well as an office and social unit of approximately 350 sq.m. "Our factory has been built according the highest standards and it incorporates state-of-the-art equip-ment, which shall enable a very high degree of auto-mation and productivity. Colquimica Poznań is cur-rently manned by a mixed team of Polish and Portu-guese employees. Our staff, which was recruited local-ly, had undergone intensive training in Portugal and is composed of young and qualified employees, with a

high degree of technical knowledge. The Portuguese co-workers will bring to the team the necessary expe-rience they accumulated over many years at the facto-ry in Portugal."

SEGRO Logistics Park Poznań will one day offer 250,000 sq.m of industrial and warehousing. Image: SEGRO

Established more than 60 years ago, Colquimica re-mains a family-owned business. The company oper-ates in more than 50 countries, selling hot-melt adhe-sives for the nonwoven industry, such as absorbent hygiene products, plasters, disposable surgical prod-ucts, filters, pocket springs and packaging of medical products. SEGRO Logistics Park Poznań is located in Komorniki municipality, close to Poznań, next to A2 motorway and national road no. 5 to Wrocław. The park is de-signed to accommodate warehousing and production activity and is intended to eventually provide 250,000 sq.m of space on over 56 ha of land.

DATA BOX: POZNAŃ INDUSTRIAL PROPERTY MARKET IN 1H 2013 The total warehouse stock in the Poznań region cur-

rently stands at 1.041m sq.m. Most warehouses are lo-

cated along the A2 motorway, in the city’s suburbs

and the S11 expressway. In the first half of 2013 some

13,600 sq.m of warehouse space came to market

(phase II of Panattoni Faurecia BTS in Gorzów

Wielkopolski). Around 50,000 sq.m is currently under

construction. The largest project is the extension to

Doxler Business Park (32,500 sq.m). Warehouse take-

up in the region totaled 66,000 sq.m in 1H 2013, 25%

less than that in the preceding six months. Despite rel-

atively modest occupier interest, the vacancy rate

stands at 3.6%, one of the lowest in the country. Rents

remained at the same level.

Existing stock (sq.m) 1,041,000

Stock under construction (sq.m) 50,000

Take-up (sq.m) 66,000

Vacancy rate (%) 3.6

Major landlords Panattoni, Prologis, SEGRO

Headline rent (EUR/sq.m/month) 3-3.6

Effective rent (EUR/sq.m/month) 2.3-2.9

Source: Cushman & Wakefield Valuation & Advisory July 2013

BANKING & FINANCE

Santander Consumer Santander Consumer Santander Consumer Santander Consumer Bank to become part of Bank to become part of Bank to become part of Bank to become part of BZ WBK Group BZ WBK Group BZ WBK Group BZ WBK Group

Poland's third largest lender, the Warsaw-listed BZ WBK has signed an investment agreement with its Spanish parent Banco Santander on the acquisition of 60% of shares in Santander's retail unit Santander

weekly newsletter # 013 / 2nd December 2013 / page 3

Consumer Bank (SCB) in a for-equity deal pricing SCB at PLN 2.16bn, the bank announced last week in a market filing. The transaction, which is subject to sev-eral conditions, including regulatory approvals, is ex-pected to be completed by end-Q1 2014, BZ WBK said in a presentation on the transaction. "With this transaction Banco Santander seeks to clari-fy the structure and operations of its subsidiaries in Poland by making SCB a direct subsidiary of BZ WBK. This was one of the promises we made when Banco Santander applied for permission to merge BZ WBK and Kredyt Bank. As a result, the combined assets of the BZK WBK group will increase to PLN 120bn, strengthening our position as Poland's third largest fi-nancial institution. Our combined customer numbers will come to 5.8m," said Artur Sikora, head of BZ WBK's communications and marketing department. At end-Q3 2013, SCB had PLN 13.77bn in assets, PLN 10.9bn in net loan portfolio, including PLN 5.3bn in mortgage loans, and PLN 6.83bn in deposits. Specializ-ing mainly in simple consumer finance products, such as car loans, as well as long-term deposits, SCM has 240 branches and 2,500 employees. Its C/I was at 46.5% in 1H 2013, whereas its Q1-Q3 profit came to PLN 290m. The deal prices SCB at PLN 2.16bn, which based on BZ WBK's average price for the last three months would translate into issuance of 6.1m new shares, the banks said in the presentation. Under such conditions, San-tander would control 71.8% of BZ WBK after the transaction, although the final number of shares to be issued will be determined after the regulator KNF gives green light for the deal. BZ WBK used to be a highly profitable division of Al-lied Irish Banks (AIB). Squeezed by the financial crisis, the Irish ended up selling the Polish business to Spain's Santander, and the latter chose to merge it

with Kredyt Bank, a Polish arm of Belgium's KBC which likewise pulled out of Poland by selling the local unit to the Spaniards. Consequently, in merely two years, Banco Santander has built a unit in Poland that is the third bank in terms of market share, with shares of 7.5% of loans and 8.7% of deposits, respectively. Bank Zachodni WBK Group has 889 branches, of which 370 came from Kredyt Bank, and about 4.1m customers, of which 3.8mare individuals, 274,500 are small or medium-sized enterprises 7,300 are corporate clients. Bringing SCB, its original Polish business, into the Group, seems like a natural move for Santander, and one that has long been anticipated by the market. Earlier this year, Santander and KBC sold 21.4% of BZ WBK for PLN 4.89bn, increasing the bank's free float to approximately 30%. Belgium's KBC sold its entire 16.17% stake for PLN 3.7bn, while Santander sold a 5.2% stake for PLN 1.19bn. Poland's financial regulator made returning BZ WBK to a significant free float of 25% a condition of its approval of the BZ WBK-Kredyt Bank merger.

BANKING & FINANCE

Regulator objects to Regulator objects to Regulator objects to Regulator objects to BPH TFI takeover by BPH TFI takeover by BPH TFI takeover by BPH TFI takeover by Investors & Abris Investors & Abris Investors & Abris Investors & Abris

One of the largest transactions in Poland's fund man-agement segment in recent years, the acquisition of BPH TFI by independent Polish operator Investors Holding, has failed to obtain regulatory clearance from the market watchdog KNF. According to media reports, the regulator did not approve of the planned structure of the transaction, which were to see private equity firm Abris Capital Partners become a majori-ty owner of the business through an equity increase.

BPH TFI's owners, GE Capital Corporation and its Polish subsidiary Bank BPH, had been hoping cash in PLN 170m from the sale transaction that were to make Investors Holding one of the leading players in Po-land's fund management business.

Poland's top 20 fund managers Asset under management in PLN bn as of end of October 2013

0 5 10 15 20

25

Open Finance TFI

Investors TFI

Noble Funds TFI

ALTUS TFI

TFI Allianz

BPH TFI

Millennium TFI

Legg Mason TFI

Quercus TFI

KBC TFI

Union Investment TFI

Forum TFI

Copernicus Capital TFI

ING TFI

Skarbiec TFI

BZ WBK TFI

Aviva Investors Poland TFI

PKO TFI

Ipopema TFI

Pioneer Pekao TFI

TFI PZU

Source: IZFA

weekly newsletter # 013 / 2nd December 2013 / page 4

As of end of October 2013 BPH TFI had PLN 3.2bn worth of assets under management and ranked as number 16 among Polish fund managers. Investors TFI was number 20 last year with PLN 2.2bn worth of assets. Their combined portfolio thus came in excess PLN 5.4bn, making the potential merged entity the 11th largest player on the market with a 3% market share. KNF's decision puts an end to Investors Holding's am-bitious expansion plans, leaving organic growth as the most likely scenario for the company in the near fu-ture. Investors Holding set up Investors TFI back in early 2005, as one of Poland's very first independent fund management companies. The founders included a number of seasoned asset management professionals, with years of experience from major banks and in-vestment funds. The already successful development of Investors TFI took a great leap forward with its ac-quisition of DWS Polska TFI in 2011 from Deutsche Bank. Besides Investors TFI, the Investors Holding in-cludes a corporate finance and private equity man-agement company DI Investors. International private equity company Abris Capital Partners, were to participate in the BPH TFI deal to help Investors Holding become one of Poland's top ten fund managers in.. Abris, which has offices in Warsaw, Kiev and Bucharest were to become a majority share-holder in Investors Holding through an equity boost, but its involvement was conditional on the BPH TFI deal going through. Due to KNF's objections, Investors Holding and Abris will now part ways. As of end of 2012, Polish fund managers had a total of PLN 145.8bn (EUR 35.6bn) under management, mark-ing a 27% increase on the prior year. This was the highest ever result recorded by the sector. The previ-ous record was made in October 2007, when the figure totaled PLN 144.3bn. Fuelled by rallying stocks and low interest rates, the market has grown by a further

22% since the beginning of the year, to PLN 178.3bn as of end of October. Debt funds represented 24% of the total portfolio, followed by share funds (17.9%) and non-public asset funds (16.6%). The leading players in the sector are PZU TFI (PLN 22.4bn), Pioneer Pekao TFI (PLN 16.9bn), and Ipopema TFI (PLN 13.6bn).

ENERGY & RESOURCES

Commercial extraction Commercial extraction Commercial extraction Commercial extraction of shale gas of shale gas of shale gas of shale gas maymaymaymay launch launch launch launch in 2014, in 2014, in 2014, in 2014, minister minister minister minister says says says says

Poland will likely launch commercial extraction of shale gas next year, announced deputy Environment Minister Piotr Woźniak at last week's "Shale Gas World Europe" conference in Warsaw, citing a suc-cessful fracking by upstream firm San Leon in Lewino. According to Woźniak, who is also Poland's chief geologist, the country will see many shale gas exploration drillings and hydraulic fracturing proce-dures next year. "Based on the results I've seen [at Lewino], initial commercial extraction will be launched in Poland next year," Woźniak said, adding that commercial extrac-tion may be pioneered by San Leon or other firms with shale gas concessions. Woźniak said the result attained by San Leon was "very good" after the company had reported that it had conducted a successful re-fracking of its Lewino-1G2 well in northern Poland and record-ed initial gas flows. "The behavior of the well during these fracture treat-ments and throughout the subsequent initial clean-up period has far exceeded expectations, and we look forward to finishing the clean up after running the well completion, and to the subsequent flow testing,"

San Leon's Executive Chairman, Oisin Fanning, com-mented on the fracks.

The hydraulic fracking in Lewino was carried out by the Łowicz-based United Oilfield Services, in which the private equity company Enterprise Investors holds a substantial stake. Image: UOS

According to a June report by US Energy Information Administration (EIA), Poland's risked, technically re-coverable shale gas resources are estimated at 4.13 tril-lion cb.m, while shale oil resources are seen at 1.8bn barrels. The new estimate constitutes a 20% reduction vs. 2011 report. The report calls the Baltic Basin in northern Poland, where San Leon's Lewino site is lo-cated, "the most prospective region," while "Podlasie and Lublin basins in eastern Poland also have potential but are structurally complex, with closely spaced faults which may limit horizontal shale drilling." A fourth area in southwest Poland, is less recognized but has non-marine coaly shale potential, the report said. While the report mentioned problems of the Polish shale gas industry, including exits of a number of play-ers, it says it's too early to play down prospects of shale gas extraction in Poland. "Yet, it is too soon to dismiss Poland’s extensive shale potential," EIA wrote. "Derisking shale plays in North America typically re-

weekly newsletter # 013 / 2nd December 2013 / page 5

quires drilling about 100 wells, while achieving econ-omies of scale requires many hundreds more."

Assessing Poland's shale riches Estimated recoverable shale gas reserves in bn cb.m

0

1,000

2,000

3,000

4,000

5,000

6,000

*PIG (2012)

Wood Mackenzie (2010)

EIA (2013)

EIA (2011)

*) Poland's Geological Institute PIG estimates the country's recovera-

ble shale gas reserves at 346-768bn cb.m

Source: Municipalities, PT archives There were 105 valid exploration licenses as of Sep-tember 1, 2013, held by 35 Polish and foreign entities. So far nearly 50 exploration boreholes have been made. Altogether the licensees plan to make 335 bore-holes by 2021. Several international explorers have di-vested or reduced their positions in Polish shale in re-cent months, including ExxonMobil, Marathon Oil and Talisman Energy, which has dented investor confidence although none of the explorers attributed their decision directly to exploration results. Poland, which consumes 15bn cb.m of gas a year, most-ly imported from Russia, has estimated its recoverable shale gas reserves at up to 768bn cb.m. The Polish government, which sees domestic extraction as a way to reduce the country's dependence on Russian gas imports, has been streamlining regulations governing Polish shale to speed up the permitting process, and

the country's Treasury has described shale develop-ment as a priority of Polish national interest. So far, however, the proposed regulation has been repeatedly delayed whereas the geology is proving more difficult than anticipated.

PROPERTY & CONSTRUCTION

HB Reavis HB Reavis HB Reavis HB Reavis signs major signs major signs major signs major office leaseoffice leaseoffice leaseoffice lease and secures and secures and secures and secures financing for Warsaw financing for Warsaw financing for Warsaw financing for Warsaw projectsprojectsprojectsprojects

Two weeks ago, when we last spoke to Stanislav Frnka, head of the Polish arm of Slovakian developer HB Reavis, we asked about the high vacancy level at their ongoing office project Gdański Business Center (see PT Business Review+ No. 011, page 7). Although the property is to reach completion next year, until re-cently HB Reavis had pre-leased only 2,000 sq.m of its planned 47,000 sq.m of GLA, with Canada's SNC Lavalin as the first tenant. "We have since signed a second tenant and I am sure other deals will follow soon," Mr. Frnka told Poland Today in mid-November, and now we learn that the mysterious second tenant is the global consultancy KPMG, which will take up to 10,000 sq.m in the BREEAM-certified Gdański Business Center. KPMG, which provides audit, tax and advisory ser-vices, will move into the new office in H2 2015. The Warsaw office is one of seven KPMG locations in Po-land along with Gdańsk, Łódź, Katowice, Kraków, Poznań and Wrocław that together employ a total of 1,200 staff. The company's Warsaw office is currently

located in the Warsaw Trade Tower building on Chłodna street. Gdański Business Center is located near the Dworzec Gdański railway station in the north of the Śródmieście district of the Polish capital and will comprise two buildings offering a combined 47,000 sq.m of leasable space. According to Karol Patynowski, senior consultant, tenant representation, at Jones Lang LaSalle the area's key assets include excellent ac-cess to public transport, well-developed road infra-structure and proximity to the Arkadia shopping mall and Ibis hotel. He added that under-construction resi-dential projects and a number of planned schemes will further foster the development of that part of Warsaw. The railway station itself is expected to be redevel-oped in cooperation with a private investor in the coming years.

Gdański Business Center will offer 47,000 sq.m of GLA and 430 parking spaces. Image: JLL

Besides Gdański Business Center, HB Reavis is work-ing on a 34,000 sq.m office project Park Postępu in Warsaw Mokotów district, not far from its first War-saw development, Konstruktorska Business Center (48,000 sq.m). The Slovakians are also gearing up for another two major projects in Warsaw. The first one will see HB Reavis develop some 90,000 sq.m of offic-es, including a 130-m tall tower, on a 1.7ha vacant lot

weekly newsletter # 013 / 2nd December 2013 / page 6

on Chmielna Street, across from the Warsaw Central Station, purchased from railway operator PKP. The company has also struck a deal with PKP to build a new Warsaw West train station along with seven of-fice buildings totaling 54,000 sq.m in a project that's expected to cost EUR 110m. Successful bond issue in Warsaw Last week HB Reavis placed a PLN 111m (EUR 26.5m) bond issue on Warsaw's Bondsport market to finance its development activities in Poland. The bonds, ma-turing in November 2017, were sold to Polish institu-tional investors including mutual and pension funds, insurance companies and asset management compa-nies. The bonds bear floating coupon with a margin of 3.95% over Wibor, which after swapping the transac-tion into Euro corresponds to 4.75% total fixed inter-est rate. "It was strategic decision of the group to enter the debt capital markets to complement our traditional bank fi-nancing approach," Jiří Hrbáček, CFO of HB Reavis, tells Poland Today. "Although there is strong interest on the part of banks to finance our projects, we seek to diversify our funding sources and broaden our inves-tor universe. Out of the core countries where we oper-ate, the Warsaw capital market is the most active and liquid. On top of this, a major part of our development pipeline is currently in Warsaw. Bondspot was chosen as the best available option with respect to size of the issue and targeted investors," Mr. Hrbáček says, deny-ing, however, any plans for an IPO in Warsaw. "Very good quality of the issuer's credit and transac-tion structure that met expectations of investors were deciding factors behind the success of this bond issue. Despite challenging times for the pension funds sector and strict pricing target set by the issuer, the transac-tion represents one of the largest bonds placements for a property developer on Warsaw market this year," added Łukasz Knap, Head of Debt Capital Markets

and Board Member of NWAI Dom Maklerski, which provided its brokerage services in the transaction.

Warsaw office market Key indicators as of end of 1H 2013

Office zones Stock

sq.m

Vacan-

cy

Central locations 1,287,000 9.9%

CBD-Central Business District 501,000 11.4%

CCF-City Centre Fringe 786,000 8.9%

Non-central locations 2,724,000 10.8%

E-East (Praga) 172,000 9.8%

LS-Lower South (Puławska) 176,000 13.0%

N-North (Żoliborz) 135,000 9.0%

SE-South East (Wilanów & Sadyba) 188,000 2.2%

SW-South West (Jerozolimskie & Okęcie) 660,000 15.6%

US-Upper South (Mokotów) 1,105,000 10.5%

W-West (Wola) 288,000 6.4%

Total 4,011,000 10.5%

Source: CBRE H1 2013 Warsaw Office MarketView

Headquartered in Luxembourg, HB Reavis operates in Slovakia, Poland, Hungary, the Czech Republic, Great Britain and Turkey. Since its establishment in 1993, it has executed projects in the office, commercial and lo-gistics real estate segment with total leasable space ex-ceeding 670,000 sq.m. With a staff of 400 profession-als and more than EUR 860m in equity, HB Reavis is managing and developing assets worth EUR 1.4bn, based on an integrated business model that combines development, construction, property management and investment management.

PROPERTY & CONSTRUCTION

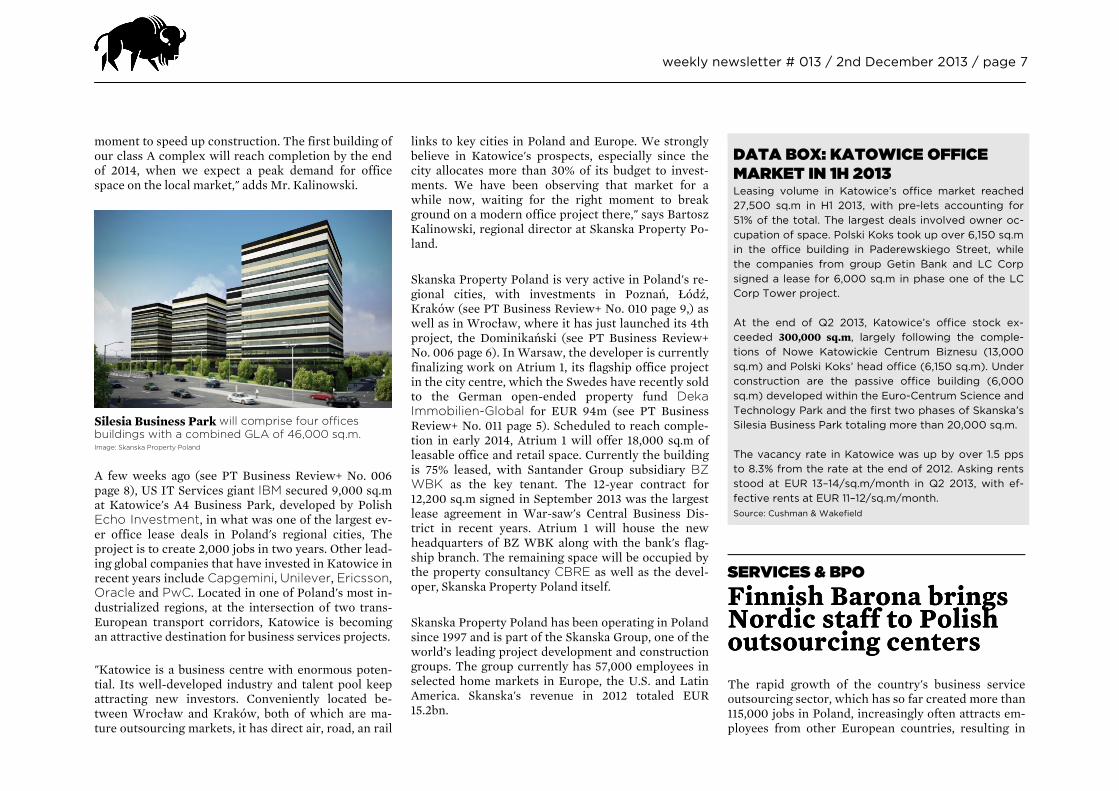

New business park in New business park in New business park in New business park in Katowice is Skanska's Katowice is Skanska's Katowice is Skanska's Katowice is Skanska's largest office project in largest office project in largest office project in largest office project in Poland toPoland toPoland toPoland to----date date date date

Nearly four years after the company first unveiled plans for the project, Swedish developer Skanska Property Poland is speeding up work on Silesia Business Park in Katowice. With a GLA of 46,000 sq.m the Katowice project will be Skanska's largest office development in Poland to-date. "We have completed the shell of an underground park-ing lot that will make up a portion of the first two buildings of the complex. Work is underway on the first 11-storey office tower with retail and service space on the ground floor. We expect to receive the occupancy permit for this building by the end of 2014," Bartosz Kalinowski, regional director at Skanska Property Poland tells Poland Today. Located along Chorzowska street, Silesia Business Park will include four 11-storey office towers and 600 parking spaces. Similar to Skanska's other recent pro-jects, the Park will hold LEED Gold and EU GreenBuilding certificates to emphasize the wide range of energy-saving solutions implemented by the investor. Skanska argues that besides being environ-mentally-friendly, its "green" buildings offer substan-tial cost savings to tenants. "We are in talks with a number of companies interest-ed in renting offices in Silesia Business Park. There is a robust demand for well-located, modern offices in Ka-towice at the moment and we believe this is the right

weekly newsletter # 013 / 2nd December 2013 / page 7

moment to speed up construction. The first building of our class A complex will reach completion by the end of 2014, when we expect a peak demand for office space on the local market," adds Mr. Kalinowski.

Silesia Business Park will comprise four offices buildings with a combined GLA of 46,000 sq.m. Image: Skanska Property Poland

A few weeks ago (see PT Business Review+ No. 006 page 8), US IT Services giant IBM secured 9,000 sq.m at Katowice's A4 Business Park, developed by Polish Echo Investment, in what was one of the largest ev-er office lease deals in Poland's regional cities, The project is to create 2,000 jobs in two years. Other lead-ing global companies that have invested in Katowice in recent years include Capgemini, Unilever, Ericsson, Oracle and PwC. Located in one of Poland's most in-dustrialized regions, at the intersection of two trans-European transport corridors, Katowice is becoming an attractive destination for business services projects. "Katowice is a business centre with enormous poten-tial. Its well-developed industry and talent pool keep attracting new investors. Conveniently located be-tween Wrocław and Kraków, both of which are ma-ture outsourcing markets, it has direct air, road, an rail

links to key cities in Poland and Europe. We strongly believe in Katowice's prospects, especially since the city allocates more than 30% of its budget to invest-ments. We have been observing that market for a while now, waiting for the right moment to break ground on a modern office project there," says Bartosz Kalinowski, regional director at Skanska Property Po-land. Skanska Property Poland is very active in Poland's re-gional cities, with investments in Poznań, Łódź, Kraków (see PT Business Review+ No. 010 page 9,) as well as in Wrocław, where it has just launched its 4th project, the Dominikański (see PT Business Review+ No. 006 page 6). In Warsaw, the developer is currently finalizing work on Atrium 1, its flagship office project in the city centre, which the Swedes have recently sold to the German open-ended property fund Deka Immobilien-Global for EUR 94m (see PT Business Review+ No. 011 page 5). Scheduled to reach comple-tion in early 2014, Atrium 1 will offer 18,000 sq.m of leasable office and retail space. Currently the building is 75% leased, with Santander Group subsidiary BZ WBK as the key tenant. The 12-year contract for 12,200 sq.m signed in September 2013 was the largest lease agreement in War-saw's Central Business Dis-trict in recent years. Atrium 1 will house the new headquarters of BZ WBK along with the bank's flag-ship branch. The remaining space will be occupied by the property consultancy CBRE as well as the devel-oper, Skanska Property Poland itself. Skanska Property Poland has been operating in Poland since 1997 and is part of the Skanska Group, one of the world’s leading project development and construction groups. The group currently has 57,000 employees in selected home markets in Europe, the U.S. and Latin America. Skanska's revenue in 2012 totaled EUR 15.2bn.

DATA BOX: KATOWICE OFFICE MARKET IN 1H 2013 Leasing volume in Katowice’s office market reached

27,500 sq.m in H1 2013, with pre-lets accounting for

51% of the total. The largest deals involved owner oc-

cupation of space. Polski Koks took up over 6,150 sq.m

in the office building in Paderewskiego Street, while

the companies from group Getin Bank and LC Corp

signed a lease for 6,000 sq.m in phase one of the LC

Corp Tower project.

At the end of Q2 2013, Katowice’s office stock ex-

ceeded 300,000 sq.m, largely following the comple-

tions of Nowe Katowickie Centrum Biznesu (13,000

sq.m) and Polski Koks’ head office (6,150 sq.m). Under

construction are the passive office building (6,000

sq.m) developed within the Euro-Centrum Science and

Technology Park and the first two phases of Skanska’s

Silesia Business Park totaling more than 20,000 sq.m.

The vacancy rate in Katowice was up by over 1.5 pps

to 8.3% from the rate at the end of 2012. Asking rents

stood at EUR 13–14/sq.m/month in Q2 2013, with ef-

fective rents at EUR 11–12/sq.m/month.

Source: Cushman & Wakefield

SERVICES & BPO

Finnish Barona brings Finnish Barona brings Finnish Barona brings Finnish Barona brings Nordic staff to Polish Nordic staff to Polish Nordic staff to Polish Nordic staff to Polish outsourcing centersoutsourcing centersoutsourcing centersoutsourcing centers

The rapid growth of the country's business service outsourcing sector, which has so far created more than 115,000 jobs in Poland, increasingly often attracts em-ployees from other European countries, resulting in

weekly newsletter # 013 / 2nd December 2013 / page 8

new cross-border opportunities for staffing compa-nies. A good example is Finland's leading recruitment services provider Barona, which over the past year has established a solid foothold in Poland. Their most recent achievement is a cooperation agreement with Finnish water chemicals company Kemira, which is currently in the process of setting up a business service center in Gdańsk (see PT Business Review+ No. 008 page 10). With a planned staff of 200, the latter will serve all of Kemira's businesses in Eu-rope, Middle-east and Africa with certain business support functions such as finance, customer service, IT and procurement. Once fully operational, the pro-ject is to translate into EUR 10m in annual savings for the company. Kemira, which provides expertise and chemicals to water-intensive industries, such as pulp & paper, oil & gas, mining and water treatment, turned over EUR 2.2bn last year with a staff of approximately 4,900 employees. "We are delighted to have been chosen as Kemira´s re-cruitment partner for their shared service center, al-ready at this early stage. We are looking forward to deepen our cooperation and enable Kemira´s team to focus on project management and supervision of de-velopment and growth of Gdańsk center. Kemira is looking for talented people with difficult to find pro-files and we are very happy to be able to provide such candidates for them, especially from the Nordic coun-tries. This is a great opportunity for many job seekers to gain valuable international work experience and take part in building something new. Gdańsk and the whole vibrant Tricity area are also providing very comfortable living environment for both foreign and Polish candidates," says Ilkka-Cristian Niemi, Business Development Manager, at Barona HR Services in Po-land. Kemira is looking for experienced and motivated peo-ple with such language skills as Finnish, Swedish,

Dutch and German, and due to their limited supply, the company has turned to Barona, which specializes in multilingual and cross-border recruitments. Ac-cording to Ilkka-Cristian Niemi, this year alone his company has relocated 40 Finns to work in Polish BPO centers, and they are soon to be joined by 20 Swedes. This is an unexpected turn of events for Barona, which arrived in Poland last year to source Polish talents for customers in Finland and Sweden. The company fo-cuses on multilingual recruitment in BPO/SSC/ITO, manufacturing and engineering as well as IT sectors. Founded in 1999, with offices in Scandinavia, Russia, Poland and the Baltics, Barona is the largest company in Finland's human resources sector, recruiting some 10,000 professionals in Finland and accommodating nearly 40,000 people every year. Besides staffing & re-cruitment, Barona provides outsourcing services. A year ago the company opened a service center in Ka-towice, Poland. Joining similar centers in Finland's Joensuu, Kuusamo, and Lappeenranta, the Katowice unit provides mainly multilingual first and second line support and application support to customers from the ICT industry.

Poland Today talks to: Ilkka-Cristian Niemi, Business Development Manager at Barona HR Services Sp. Z o.o.

• PT: The 40 Finns & 20 Swedes you've relocated to Poland: what positions are those typically? Regular BPO staff or executives??

Ilkka-Cristian Niemi: They're regular BPO/SSC/ITO staff, usually with customer service experience and fluent/native knowledge of the language. But there are also some managers and team leaders for outsourcing centers. • PT: Do you think many more will be coming? ICN: By the end of 2014 we expect to recruit about 40-50 Scandinavians/Finns and a few from the Baltics to our own center in Katowice alone plus a further 30-50 for our external clients in BPO/SSC sector, resulting total about 100 people from Nordics in 2014. Probably there will also be a few from the Netherlands and oth-er European countries. • PT: What's the key attraction for Nordic employees in Poland? Surely, the money can’t be that good... ICN: For one, Poland is relatively close to the Nordics and finding a proper job in Finland or Sweden is not easy due to economic situation as well as outsourcing of back office jobs to lower cost countries. Poland of-fers much lower living costs, which means that most Finns net more money in Poland than in Finland, even though gross salary is higher in Finland. Gaining in-ternational experience is also a major attraction and for many this is a journey of a lifetime: new and inter-national job, new country, new friends etc… • PT: Kemira seeks to employ 200 staff in Gdańsk. What % of them will be non-Poles, in your opinion?

ICN: They are aiming at 20% and with certain lan-guages natives are the only way to cover their needs. I believe the 20% will be the minimum ratio. It´s great to be able to help them to build such an organization which differs a bit from others.

weekly newsletter # 013 / 2nd December 2013 / page 9

• PT: It's been over a year since Barona came to Po-land to source talents for Nordic clients. Have you achieved your key objectives so far? Have there been any surprises?

ICN: Especially in Finland the economic slowdown has had influence on the market, but it has also created opportunities for specialization in certain businesses which need labor all the time (e.g. industrial mainte-nance). In Sweden we have positive feedback and ex-periences from our client projects and we have strengthened our own team which should result in significant growth in 2014 regarding Polish labor. A positive surprise has been that the Nordic countries are becoming an increasingly attractive destination for Poles. They have always been, but now they are get-ting even more popular. Candidates prefer the Nordics to Germany, Netherlands, France or UK. But we can also see that Norway is overtaking the other Nordic countries due to much higher income, though the liv-ing costs are also much higher. • PT: What is Barona's key focus in Poland at the moment?

ICN: We have three major business areas: recruitment and staffing in the Polish market, ICT Services Center in Katowice and cross-border staffing to the Nordics. In recruitment we are concentrating in BPO/SSC sec-tor and gaining share rapidly with our “niche” service being able to relocate native speakers from Nordics. Also Manufacturing & Engineering and IT are areas where we want to grow. Beside these business lines our focus is of course all Nordic companies that are al-ready here, or are planning to establish business in Po-land. • PT: How many staff have you got at the ICT cus-tomer support centre in Katowice and what are your plans?

ICN: By the end of 2014 we will have close to 100 em-ployees in Katowice. There are no plans or strategy as

of yet for other projects, but within few years the cen-tre will grow to reach some 200 employees. • PT: How about the remainder of Barona's Polish organization?? ICN: Our employee numbers are growing relatively fast. In the recruitment business Barona HR Services we seek to achieve significant growth during next years to double our size and turnover. By the end of 2014 we should have two new offices in Poland, be-sides Kraków and Katowice.

TRANSPORT & LOGISTICS

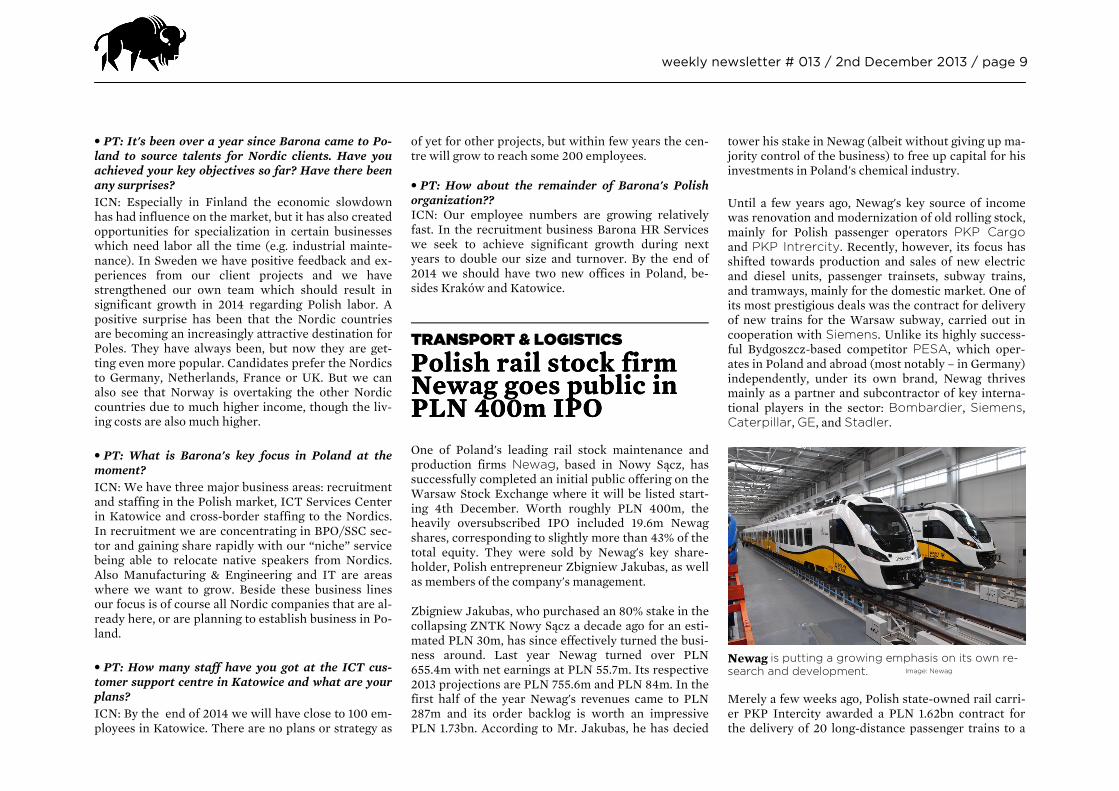

Polish rail stock firm Polish rail stock firm Polish rail stock firm Polish rail stock firm Newag Newag Newag Newag goesgoesgoesgoes public in public in public in public in PLN 400m IPOPLN 400m IPOPLN 400m IPOPLN 400m IPO

One of Poland's leading rail stock maintenance and production firms Newag, based in Nowy Sącz, has successfully completed an initial public offering on the Warsaw Stock Exchange where it will be listed start-ing 4th December. Worth roughly PLN 400m, the heavily oversubscribed IPO included 19.6m Newag shares, corresponding to slightly more than 43% of the total equity. They were sold by Newag's key share-holder, Polish entrepreneur Zbigniew Jakubas, as well as members of the company's management. Zbigniew Jakubas, who purchased an 80% stake in the collapsing ZNTK Nowy Sącz a decade ago for an esti-mated PLN 30m, has since effectively turned the busi-ness around. Last year Newag turned over PLN 655.4m with net earnings at PLN 55.7m. Its respective 2013 projections are PLN 755.6m and PLN 84m. In the first half of the year Newag's revenues came to PLN 287m and its order backlog is worth an impressive PLN 1.73bn. According to Mr. Jakubas, he has decied

tower his stake in Newag (albeit without giving up ma-jority control of the business) to free up capital for his investments in Poland's chemical industry. Until a few years ago, Newag's key source of income was renovation and modernization of old rolling stock, mainly for Polish passenger operators PKP Cargo and PKP Intrercity. Recently, however, its focus has shifted towards production and sales of new electric and diesel units, passenger trainsets, subway trains, and tramways, mainly for the domestic market. One of its most prestigious deals was the contract for delivery of new trains for the Warsaw subway, carried out in cooperation with Siemens. Unlike its highly success-ful Bydgoszcz-based competitor PESA, which oper-ates in Poland and abroad (most notably – in Germany) independently, under its own brand, Newag thrives mainly as a partner and subcontractor of key interna-tional players in the sector: Bombardier, Siemens, Caterpillar, GE, and Stadler.

Newag is putting a growing emphasis on its own re-search and development. Image: Newag

Merely a few weeks ago, Polish state-owned rail carri-er PKP Intercity awarded a PLN 1.62bn contract for the delivery of 20 long-distance passenger trains to a

weekly newsletter # 013 / 2nd December 2013 / page 10

consortium of Swiss Stadler Rail and Newag. The new trains will be an advanced version of Stadler's flagship eight-carriage FLIRT model, which can al-ready be found on a number of routes in Poland. As far as the division of responsibilities within the consortium is concerned, Stadler is to deliver the two end vehicles along with the entire drive system as well as supply the bogies and the aluminum bodies for all cars. Newag, on its part, has been put in charge of planning the interior fittings as well as the final as-sembly of all intermediate cars. Newag will also con-nect the two end vehicles with the intermediate cars and handle the entire commissioning process. Newag employs some 1,300 workers across two factories, in Nowy Sącz and Gliwice. Stadler owns an assembly plant in Siedlce (90km east of Warsaw), where some 700 staff are employed. Although the trains themselves are to be made in Po-land by Stadler and Newag, certain parts, such as the bogies and the drive components, will be produced in Stadler's Swiss factories. All EMUs (electric multiple units) are to be delivered by the end of 2015. In addi-tion, Stadler will ensure the technical maintenance of the trains for 15 years.

TRANSPORT & LOGISTICS

Szymany airport Szymany airport Szymany airport Szymany airport projecprojecprojecproject one step closer t one step closer t one step closer t one step closer to becoming realityto becoming realityto becoming realityto becoming reality

Although merely a year has passed since the opening of Poland's latest passenger airport in Lublin, local au-thorities in the northeastern Mazury lake district are putting together technical documentation for another regional airport, in Szymany near Szczytno (approx.

50km southeast of Olsztyn). Polish engineering com-pany Polconsult has just won a PLN 1.3m contract to prepare the said paperwork and building works are to begin shortly after. The regional authorities plan to spend PLN 200m on the whole project, hoping for the EU to pay for up to 75% of the investment. The former military airport in Szymany had been in operation un-til 2004 and it is to be back in business, this time with civilian airplanes, in 2015, with a renovated runway and new terminal.

The authorities are hoping the new Szymany airport will stimulate tourism and investment in the north east of Poland. Image: Port Lotniczy Szymany

According to earlier estimates, the Szymany airport is to initially receive some 57,00 passengers per annum, which is less than enough to ensure its economic via-bility. The authorities believe that over two decades the figure is to reach 731,000 but many observers con-sider such estimates as a textbook case of wishful thinking. Although the project is unlikely to turn prof-itable in any foreseeable future, municipalities from the Szczytno area are hoping the new airport brings an influx of foreign tourists and investors to the Warmia

and Mazury region, which despite its natural beauty suffers from high unemployment. In the case of Szymany, the airport will also suffer di-rect competition with the Warsaw-Modlin airport, lo-cated merely 120km to the south. Modlin reopened this autumn (see PT Business Review No 003 page 11 and No 009 page 7) after being closed for repairs for more than half a year. Modlin is the Warsaw base for Ryanair, from where the Irish low-cost flies to over 30 European destinations. "We expect our traffic to grow to 1.5m passengers to/from Modlin in 2014," Ryanair’s CEO Michael O’Leary said back in October. "We have no doubt that Warsaw Modlin’s location allied to its low cost base, cheap car parking and easy bus transfers, will make it the airport of choice for passengers flying on Ryanair’s first two Polish domestic routes from Gdańsk and Wrocław to Warsaw. These first two domestic routes will deliver significantly lower air fares for Polish con-sumers, and finally free them from LOT’s high fares on domestic routes." Despite the impressive growth of Poland's air travel industry in recent years, many industry insiders be-lieve that only the country's three largest airports (Warsaw, Kraków, Gdańsk) attract enough passengers to stay profitable, with the rest having to partially rely on municipal or regional subsidies. The Lublin airport, opened shortly before Christmas last year at the cost of PLN 400m, were to welcome 300,000 passengers in 2013, but in the first half of the year the figure came to merely 83,700. The construction of Port Lotniczy Lu-blin took two years and it was completed in October last year. Spread over some 300ha, the airport includes a 2.5km long runway, and a 11,000 sq.m terminal, ca-pable of handling up to 1m passengers. Travelers can get to Lublin in 15 minutes by railbus, thanks to a brand new railway line. The Lublin airport belongs to the Lublin and Świdnik municipalities and the Lublin

weekly newsletter # 013 / 2nd December 2013 / page 11

regional authority. Close to a third of the financing for the project was provided by the EU under one of the latter's cohesion instruments.

More difficult year for regional airports Poland's largest airports, millions of passengers

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

Rzeszów

Poznań

Wrocław

Katowice

Gdańsk

Kraków

Warsaw*

1H 2013

1H 2012

Source: ULC *) Chopin Airport

Another regional airport is emerging in the central Polish town of Radom, located merely 100km south of Warsaw, is expecting to launch passenger flights in July next year. The former military airport is being currently upgraded at the cost of PLN 25m. The air-port has acquired a former passenger terminal from Łódź, which had been dismantled and reassembled in Radom. The terminal will be able to handle 380 pas-sengers (two Boeing 737-80) at a time, maximum 1.5m a year. Local authorities say budget carriers are inter-ested in the new destination, perhaps as a second low-cost alternative to Warsaw's Chopin airport. In early November the new airport secured its first client: tour operator Alfa Star, which seeks to launch charter flights to Egypt from Radom in July 2014. In the first half of the year Polish airports handled 11.28m passengers, 0.4% fewer than in the correspond-ing period of 2012 but 16% more than in January-June

2011. Warsaw's Chopin airport welcome more than 5m passengers, followed by Kraków-Balice (1.65m), Gdańsk Lech Wałęsa airport (1.28m), and Katowice Pyrzowice (1.08m), and Wrocław-Strachowice (0.84m). Next year the top five list will almost certain-ly include Modlin, which was not in operation in 1H 2013.

CONSUMER GOODS & RETAIL

Balmain & Balmain & Balmain & Balmain & NBGI NBGI NBGI NBGI bubububuilding EUR 25m ilding EUR 25m ilding EUR 25m ilding EUR 25m retail project in retail project in retail project in retail project in StarachowiceStarachowiceStarachowiceStarachowice

Investors NBGI Private Equity and Balmain Asset Management have held a corner-stone laying cere-mony at the construction site of their Centrum Galardia shopping centre project in Starachowice in south-eastern Poland. The project is to reach comple-tion in autumn next year, becoming the area's most modern shopping destination. "It is the first project that we have been handling from the very beginning, as a ground up developer," Tim Rylance, Asset Management Director at Balmain Asset Management, tells Poland Today. "We hope to finalize more projects in this capacity but full-scale develop-ment is not going to be our core business. We are ob-serving the situation on the market and looking at oth-er opportunities, however we have nothing clearly de-fined as of yet. We used to consider a next develop-ment project, but in the end we decided not to carry it out." The Starachowice scheme is being built by Skanska with ARCADIS/ EC Harris as project managers. With an estimated capex of around EUR 25m, the

scheme will deliver 18,000 sq.m of leasable space di-vided into 38 retail units. So far, nearly two thirds (65%) of the available GLA at Centrum Galardia has been pre-leased. Its key tenants include a 6,200-sq.m Tesco Extra as the hypermarket anchor, as well as a 1,330-sq.m Helios movie theater, Media Expert elec-trical outlet, Rossmann drugstore and Polish LPP Group with its popular fashion brands Reserved, Mohito, Sinsay, Cropp, and House.

Anchored by Tesco and Helios, Centrum Galardia will open next year with a GLA of 18,000 sq.m. Image: Centrum Galardia

"Within a 10-minute drive from Centrum Galardia live 51,600 residents and the catchment, area of the Centre covers a population of 78,000. Our goal is to create a unique destination shopping and entertainment centre which will serve local inhabitants in the best possible way offering a wide choice of local and international brands not yet present in Starachowice," commented James Huckle of NBGI Private Equity. NBGI Private Equity is a private equity and capital in-vestment firm which currently manages around EUR 900m across a number of funds. With offices in Lon-don, Paris, Athens, Warsaw, Sofia, and Bucharest, it invests in a range of different private equity sectors in-

weekly newsletter # 013 / 2nd December 2013 / page 12

cluding mid-market buy-outs, growth capital for small and medium-sized companies, venture capital for technology businesses and real estate. Established in 2003, Balmain Asset Management spe-cializes in the development and leasing of shopping centers and other commercial facilities. The company is majority owned by its principals with niche property fund manager/venture capital investor, REVCAP LLP, holding a stake as well. Balmain has established rela-tionships with a number of funding and joint venture partners including three existing investment vehicles in partnership with REVCAP, Investec and HBoS/Lloyds via their Balmain European Property Investments limited liability partnerships. Additional-ly Balmain has a number of third party and co-investment mandates with investors including Resolu-tion Property Advisors, Rockspring Property Invest-ment Management, Charter Hall and NBGI. The company has been operating in Poland, its core market, since 2004 with an experienced Warsaw-based team. Balmain has over EUR 500m or retail property assets under management containing in ex-cess of 1,000 tenancy units & 255,320 sq.m of GLA in 25 properties welcoming over 40m customers annual-ly. Its key business areas include acquisition, manage-ment and redevelopment of existing shopping centers in Poland. One of Balmain's largest projects at the moment is the ongoing extension of Galeria Pomorska in Bydgoszcz, which will see the centre's GLA grow by 10,000 sg.m, adding 37 new shops to reach a total of 140 retail units. "The project will be carried out in stages. A new cus-tomer car park providing some 160 additional parking spaces is almost completed. By spring next year we expect to build a new multi storey car park with 900 spaces, and it will be followed by the construction of single level gallery extension, to be completed a year later. The extension of Galeria Pomorska represents

an investment of approximately PLN 110m," says Agata Radlak-Piechowicz, spokesperson for Balmain's Polish shopping centers. The company is also close to completing a PLN 20m extension of Ferio SC in Stare Miasto near Konin, which adds 2,500 sq.m of retail space to the existing property and introduces a number of retailers includ-ing: C&A, Smyk, Stradivarius, Sinsay, Home&You and Martes Sport to this central Polish town. Earlier this year. Balmain modernized and extended its Aura Cen-trum Olsztyna property, formerly known as Alfa Ol-sztyn, also at the cost of PLN 20m.

DATA BOX: RETAIL SALES Polish retail sales rose at an annual rate of 3.2% in Oc-

tober, on a 3.6% monthly increase, the Central Statisti-

cal Office GUS said. The PAP Polish news agency ana-

lyst survey had shown consensus expectations for a

4.3% y/y increase and a 4.7% m/m growth. In Septem-

ber, Polish retail sales increased at an annual rate of

3.9%, on a 0.9% monthly decline.

Retail sales in Poland (y/y)

-5%

0%

5%

10%

15%

20%

Apr 11 Oct 11 Apr 12 Oct 12 Apr 13 Oct 13

Source: GUS

CONSUMER GOODS & RETAIL

Textile discounter KiK Textile discounter KiK Textile discounter KiK Textile discounter KiK to speed up expansion to speed up expansion to speed up expansion to speed up expansion in Poland next yearin Poland next yearin Poland next yearin Poland next year

When we spoke to German discount clothing & non-food chain KiK following the opening of their 20th Polish store opened in March 2013, the company was hoping to add a further 50 stores to the chain by the end of the year. Although KiK's Polish retail network continues to expand, its growth has proven slower than expected, with merely 28 locations in operation to-date. KiK is seeking suitable units to lease in cities of at least 10,000 inhabitants, preferably in city centers or shop-ping malls. As ideal neighbors for its outlets the com-pany lists self-service department stores, food dis-counters, drugstores, specialty markets and local sup-ply centers. The retail units themselves should range from 500 to 2,000 sq.m, preferably on ground floor, with large windows and an outdoor sale area, with clearly visible entrances, and parking. An average KiK store measures between 500 and 800 sq.m, offers about 10,000 articles from ladies-, men's-, kids and ba-by wear to accessories, gifts, toys, beauty products and home textiles, and employs from 8 to 10 employees. In 2011 KiK (short for 'Kunde ist König' or 'Customer is King') turned over EUR 1.69bn and had close to 20,100 employees. The company operates more than 3,200 outlets in eight European countries: Germany (2,600 shops), Austria, Croatia, Slovakia, Slovenia, Czech Republic, Hungary, and Netherlands. Over the coming four years KiK seeks to launch another 1,000 stores throughout the region. Logistics for Poland is

weekly newsletter # 013 / 2nd December 2013 / page 13

being handled by the company's central depot in Bönen, Germany. Established in 1994, KiK is part of Germany's Tengelmann group, which operates 44 OBI DIY su-permarkets in Poland. Tengelmann's Polish business used to incorporate a food discount chain Plus, before the company sold it (210 outlets in Poland and 75 in Portugal) to Portuguese Jeronimo Martins (operator of the Biedronka chain) in 2008 for an estimated EUR 320m. KiK's main competitor in Poland is the South African chain PEPCO, which currently has close to 500 outlets in Poland, expanding at the rate of more than 100 locations per annum.

Poland Today talks to: Mariusz Kulik, Managing Director of KiK Textilien Polska

• PT: When we spoke earlier this year, your plan was to have 70 stores in Poland by the end of 2013? Are you on track to achieve that objective?

Mariusz Kulik: We have since reduced our target due to strategic changes in the company, including the in-troduction of a new KiK 17 concept in our European chain, which required new merchandising standards and staff training systems. These are growth-oriented changes that support our long-term expansion in Po-land. We have opened 28 stores in Poland to-date and plan to add a further 10 by New Year's. We have also

strengthened our expansion team, which should give us a solid basis for growth in 2014. • PT: What is your target for 2014 then? MK: We want to open at least 40 new stores and enter all regional markets, focusing on nationwide expan-sion of the chain and implementation of the new con-cept. Our existing stores keep improving their results, which is encouraging. • PT: Can you tell us more about the financials? MK: All I can says is that we have beaten our projec-tions both in terms of sales as well as profits. Consid-ering that we have been on the market for less than two years, we find this satisfactory. • PT: Is your search for suitable locations proving more challenging than initially expected? MK: We are inviting landlords across the country to long-term cooperation and a growing number of them see KiK as an attractive business partner. Retail centre managers increasingly often choose to balance out their tenant mix by inviting both upscale boutiques and textile discounters. Our stores are visually attrac-tive and they generate footfall. Last but not least, we adhere to strict cooperation standards that emphasize fairness in landlord-tenant relations. • PT: After two years on the market, have your loca-tion preferences changed in any way? MK: We remain interested mainly in shopping centers and retail parks, both in large and small cities. Of course we are also paying close attention to the bottom line, so the turnover-to-cost ratio for each location has to ensure profitability in the shortest possible time, in order to meet our standards.

HEALTHCARE & PHARMA

US medical equipment US medical equipment US medical equipment US medical equipment company enters company enters company enters company enters Warsaw bourse Warsaw bourse Warsaw bourse Warsaw bourse

Shares in New Jersey-based medical technology startup Milestone Medical, a subsidiary of Mile-stone Scientific, debuted on the New Connect mar-ket of the Warsaw Stock Exchange last week after the company raised USD 1.5m of common stock in a pri-vate placement to European institutional and other in-vestors. Milestone's stock opened at PLN 6.98 apiece, 50% above its IPO price. New shares represent slightly more than 9% of Milestone's increased equity. Milestone Medical Inc. was formed two years ago as a joint venture between Milestone Scientific Inc. and Beijing 3H Scientific Technology Co. Ltd. for the development, commercialization, manufacturing and marketing of Milestone's epidural and intra-articular injection instruments. Net proceeds from the financ-ing will be used for growth capital, including hiring personnel, signing additional international distribu-tors, and supporting regulatory requirements, the company said in a statement. "This timely financing provided by European investors will enable Milestone Medical Inc. to develop distribu-tion channels throughout the world. Based on our proprietary platform technology, we believe these first two medical applications represent a significant mar-ket opportunity for both Milestone Medical Inc. and Milestone Scientific Inc.," said Leonard Osser, Chief Executive Officer of Milestone Scientific. The company estimates its market segment at some USD 1bn, as in the US alone some 11.4m patients a year

weekly newsletter # 013 / 2nd December 2013 / page 14

receive epidural anesthesia, including 2.5m pregnant women. Despite the widespread popularity of the pro-cedure, it is not without risk, with as many as 3-4% of cases being mishandled. Milestone claims its system helps a clinician know the location of a hypodermic needle during an injection by measuring the density of body tissue and is therefore 100% foolproof. In appli-cations that have already received clearance, the sys-tem utilizes computer controlled technology to pro-vide real-time feedback to the medical practitioner, providing precision technology for administering a drug to a patient. The company expects to register its technology in the EU and US in mid-2014.

Milestone Medical says its patented injection device offers ensures full safety in epidural anesthesia. Image: Milestone Medical

Milestone representatives said their chose Warsaw as the size of their placement was too small for US stock exchanges. The offering agent and leading financial advisor behind their Warsaw IPO was WDM, a War-saw-listed small cap investment bank WDM, which over the past six years has taken over 50 companies public on the Warsaw Stock Exchange and raised over USD 150m in private equity, venture capital and public financing for its clients. WDM's investment manage-ment subsidiary, WDM Capital, manages a growing portfolio of some of the region's most promising micro

caps. WDM's United States subsidiary, WDM Capital USA, provides access to CEE financing and investment opportunities for North American clients and North American financing and market access for CEE clients.

POLITICS & ECONOMY

Official Q3 Official Q3 Official Q3 Official Q3 GDP GDP GDP GDP figures figures figures figures show modest recovery show modest recovery show modest recovery show modest recovery in consumption and in consumption and in consumption and in consumption and investments investments investments investments

Poland's central statistical office GUS has confirmed its flash estimate from mid-November, which saw the country's economic growth accelerate to its fastest pace in more than a year in Q3 2013. Gross domestic product, unadjusted for seasonal effects, rose 1.9% from a year earlier, compared with a 0.8% growth in Q2. Seasonally adjusted quarterly growth was con-firmed at 0.6% in the third quarter up from 0.4% in the second quarter. In the first nine months of 2013 real growth came to 1.1%, GUS said. What's important about the Friday announcement by GUS is that it offers a glimpse into the composition of the growth, where one can discern the first signals of a true economic recovery. Although exports remained the main driver of growth in Poland, with 6.4% annual growth, the GUS data showed also some positive trends in consumer spending and investments. Po-land's domestic demand rose 0.5% in the third quarter compared with a 1.7% decline in the second quarter, while fixed investments rose 0.6% during the period, compared with a 3.2% drop a quarter earlier. Private consumption rose 1.0% from July to September, com-pared with an increase of 0.2% in the previous quarter.

"Such composition of the GDP suggests that the Polish economy is waking up from its year-long slumber and in the coming quarters growth will rely on more than just exports. Moreover, the value of goods and services exported in the past quarter saw the highest increase in two years," commented Krzysztof Kolany, chief economist at the financial portal Bankier.pl.

Gross Domestic Product (y/y)

0%

1%

2%

3%

4%

5%

6%

Q3'09 Q1'10 Q3'10 Q1'11 Q3'11 Q1'12 Q3'12 Q1'13 Q3'13

Seasonally unadjusted Seasonally adjusted

Source: GUS

Although modest, the said increases point to an im-proving sentiment among businesses and households, which should lay foundations for a faster recovery in the coming months. Prime Minister Donald Tusk said he is banking on a growth of 2% or more in Q4 and a full-year growth of 1.4% this year and 3% in 2014. The central bank, which expects the country's GDP growth to reach 1.4% in 2013, has pledged to keep its main interest rate at a record low until mid-2014 or longer to aid a "moderate" recovery from the econo-my’s worst slowdown in at least a decade. In 2012 Po-land's economy grew at a pace of 1.9%, but it should be noted that since 2008, when the European economy

weekly newsletter # 013 / 2nd December 2013 / page 15

barely avoided a contraction, Poland has grown by an aggregate 19.8%. A number of institutions have recently raised their growth forecasts for Poland. The OECD is expecting the Polish economy to expand by 2.7% in 2014 and 3.3% in 2015. According to Moody's, Poland's GDP growth will accelerate to 2.5% in 2014 from 1.4% in 2013, while CPI will hit 1.7% in December 2014. The rating agency also said Poland will record public fi-nance sector surplus of 4.6% of GDP next year after some 4.8% deficit in 2013 as a result of changes in the private pension system OFE. Current account deficit will drop to 1.5% of GDP in 2014 from 1.9% in 2013, Moody's also said.

POLITICS & ECONOMY

E&Y says investors E&Y says investors E&Y says investors E&Y says investors need to hurry to make need to hurry to make need to hurry to make need to hurry to make the most of Polish the most of Polish the most of Polish the most of Polish special economic zones special economic zones special economic zones special economic zones

The global business advisory giant Ernst&Young has published a brand new report on Polish special eco-nomic zones (SEZ), in which it urges companies to speed up their investment decisions in order to take full advantage of the current incentive mix that will remain in place only until the end of June 2014. "Taking into account the recent and planned changes in SEZ regulations, it is recommended that all inves-tors considering new projects apply for a SEZ permit before July 1, 2014. This will provide them with addi-tional six years (giving in total about 13 years) for utili-zation of the CIT exemption on one hand, and, on the other hand, will enable them to take advantage of

higher aid intensity and less restrictive requirements than those effective from July 1, 2014," E&Y experts say in the report, referring to the planned changes to EU regional aid intensity levels that directly influence the maximum value of CIT exemptions companies op-erating in the SEZ can count on. The value of tax incentives available to investors in the SEZ depends on the one hand on the size of the pro-ject (capital expenditures or two-year employment costs), and on the other – on external administrative factors, namely the level of state aid intensity in a giv-en region and the remaining period of SEZs' existence. Earlier this year the government has extended the zones' lifetime by additional until 2026. This prolonga-tion gives investors entering the SEZs an additional 6 years to take advantage of the CIT exemption. Com-panies that entered the SEZs in the first half of 2013 could count on merely 6.5 years to utilize the SEZ credit, but following the extension they have twice as much time. However, as a result of changes to EU pol-icy, the average level of regional aid intensity in the EU and therefore also in Poland will decrease signifi-cantly in July 2014. "The value of available state aid is something many in-vestors take into consideration when choosing where to invest. Hence, the government's decision to extend the existence of the SEZ until 2026 is fantastic news for entrepreneurs. Taking into consideration the fact that there's still more than six months left until the new EU aid intensity levels enter into force and that the economic outlook for Poland is looking increasing-ly positive, one can expect many new investment deci-sions in the coming months," commented Paweł Tynel, Director at Ernst & Young, Head of Grants and Incen-tives Advisory Services, who co-authored the report. E&Y experts emphasize Poland's uninterrupted cumu-lative economic growth of 18.1% over the 2008-2012 period, during which the entire EU economy contract-

ed 0.8%. According to forecasts by E&Y and Oxford Economics, Poland's GDP growth will reach 3.5-3.6% in 2016. Five Polish SEZ were included in the fDi Magazine's recent list of the world's 50 best special economic zones, with Katowice ranking no 2 in Eu-rope and no 11 globally. Other Polish zones mentioned in the ranking are: Łodź, Wałbrzych, Pomeranian and Starachowice SEZ, all scoring high on quality of infra-structure and good transport connections. Until December 31, 2012, the SEZ had issued 1,545 in-vestment permits, attracted capital expenditures worth more than EUR 20.4bn, and created in excess of 186,000 new jobs. The leading zones, by both invest-ment volume and job creation, are the Katowice SEZ and Wałbrzych SEZ, with other strong performers be-ing Łódź, Mielec, Legnica and Tarnobrzeg. The overall area actually covered by all zones now exceeds 15,800 ha, out of which 40% (over 6,000 ha) is still available for new investors. Moreover, the SEZ area may be ex-tended by including new plots of land up to the limit of 20,000 ha.

DATA BOX: UNEMPLOYMENT

Poland's registered unemployment rate held flat at the

prior-month level of 13.0%, still up from 12.5% one year

prior, according to Central Statistical Office (GUS)

figures released last week. The number of registered

jobless at end-October measured 2.075m, down 7,900

or 0.4% from the prior month. Against the prior year

period, the number of registered jobless is up 80,300

or 4.0%. Measured by the Labor Force Survey,

Poland's harmonized unemployment came to 9.8% in

Q3, down from 10.4% in Q2, GUS added.

weekly newsletter # 013 / 2nd December 2013 / page 16

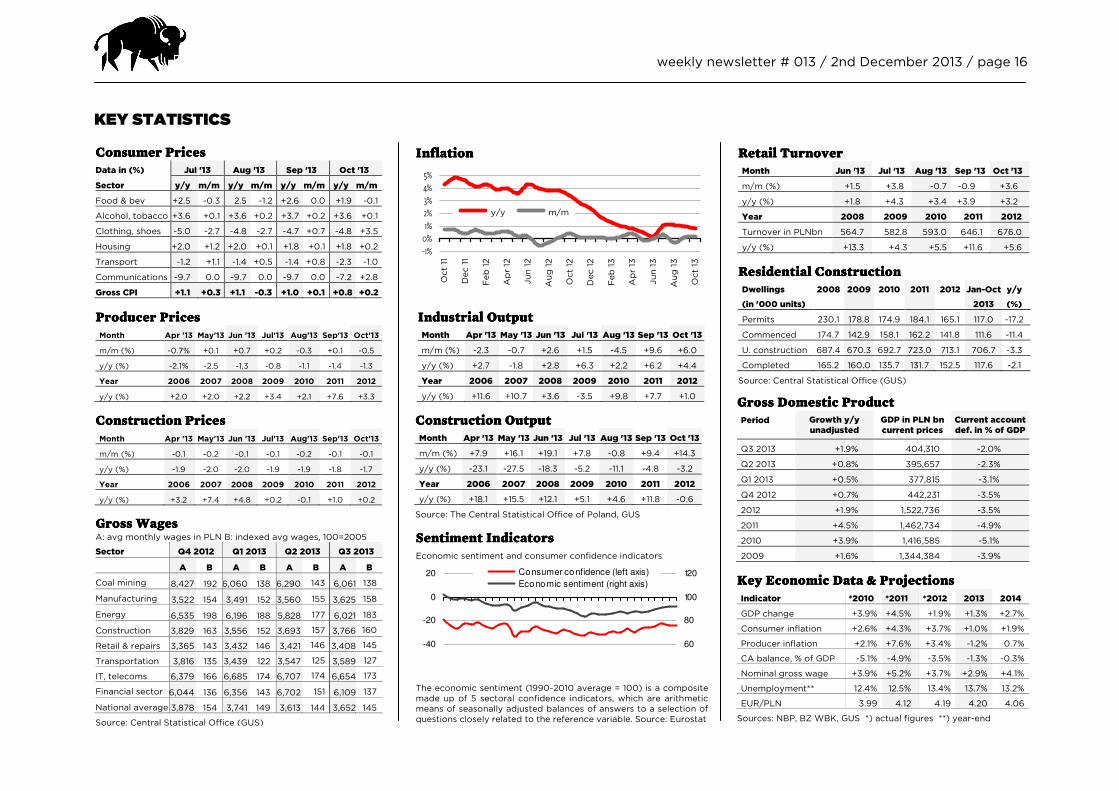

KEY STATISTICS

Consumer PriceConsumer PriceConsumer PriceConsumer Pricessss

Data in (%) Jul '13 Aug '13 Sep '13 Oct '13

Sector y/y m/m y/y m/m y/y m/m y/y m/m

Food & bev +2.5 -0.3 2.5 -1.2 +2.6 0.0 +1.9 -0.1

Alcohol, tobacco +3.6 +0.1 +3.6 +0.2 +3.7 +0.2 +3.6 +0.1

Clothing, shoes -5.0 -2.7 -4.8 -2.7 -4.7 +0.7 -4.8 +3.5

Housing +2.0 +1.2 +2.0 +0.1 +1.8 +0.1 +1.8 +0.2

Transport -1.2 +1.1 -1.4 +0.5 -1.4 +0.8 -2.3 -1.0

Communications -9.7 0.0 -9.7 0.0 -9.7 0.0 -7.2 +2.8

Gross CPI +1.1 +0.3 +1.1 -0.3 +1.0 +0.1 +0.8 +0.2

IIIInflationnflationnflationnflation

-1%

0%

1%

2%

3%

4%

5%

Oct 11

Dec 11

Feb 12

Apr 12

Jun 12

Aug 12

Oct 12

Dec 12

Feb 13

Apr 13

Jun 13

Aug 13

Oct 13

y/y m/m

Retail Retail Retail Retail TurnoverTurnoverTurnoverTurnover

Month Jun '13 Jul '13 Aug '13 Sep '13 Oct '13

m/m (%) +1.5 +3.8 -0.7 -0.9 +3.6

y/y (%) +1.8 +4.3 +3.4 +3.9 +3.2

Year 2008 2009 2010 2011 2012

Turnover in PLNbn 564.7 582.8 593.0 646.1 676.0

y/y (%) +13.3 +4.3 +5.5 +11.6 +5.6

Residential ConstructionResidential ConstructionResidential ConstructionResidential Construction

Dwellings

(in '000 units)

2008 2009 2010 2011 2012 Jan-Oct

2013

y/y

(%)

Permits 230.1 178.8 174.9 184.1 165.1 117.0 -17.2

Commenced 174.7 142.9 158.1 162.2 141.8 111.6 -11.4

U. construction 687.4 670.3 692.7 723.0 713.1 706.7 -3.3

Completed 165.2 160.0 135.7 131.7 152.5 117.6 -2.1

Source: Central Statistical Office (GUS)

GGGGross Domestic Productross Domestic Productross Domestic Productross Domestic Product

Period Growth y/y unadjusted

GDP in PLN bn current prices

Current account def. in % of GDP

Q3 2013 +1.9% 404,310 -2.0%

Q2 2013 +0.8% 395,657 -2.3%

Q1 2013 +0.5% 377,815 -3.1%

Q4 2012 +0.7% 442,231 -3.5%

2012 +1.9% 1,522,736 -3.5%

2011 +4.5% 1,462,734 -4.9%

2010 +3.9% 1,416,585 -5.1%

2009 +1.6% 1,344,384 -3.9%

Key Economic Data & ProjectionsKey Economic Data & ProjectionsKey Economic Data & ProjectionsKey Economic Data & Projections

Indicator *2010 *2011 *2012 2013 2014

GDP change +3.9% +4.5% +1.9% +1.3% +2.7%

Consumer inflation +2.6% +4.3% +3.7% +1.0% +1.9%

Producer inflation +2.1% +7.6% +3.4% -1.2% 0.7%

CA balance, % of GDP -5.1% -4.9% -3.5% -1.3% -0.3%

Nominal gross wage +3.9% +5.2% +3.7% +2.9% +4.1%

Unemployment** 12.4% 12.5% 13.4% 13.7% 13.2%

EUR/PLN 3.99 4.12 4.19 4.20 4.06

Sources: NBP, BZ WBK, GUS *) actual figures **) year-end

GrGrGrGross Wagesoss Wagesoss Wagesoss Wages A: avg monthly wages in PLN B: indexed avg wages, 100=2005

Sector Q4 2012 Q1 2013 Q2 2013 Q3 2013

A B A B A B A B

Coal mining 8,427 192 6,060 138 6,290 143 6,061 138

Manufacturing 3,522 154 3,491 152 3,560 155 3,625 158

Energy 6,535 198 6,196 188 5,828 177 6,021 183

Construction 3,829 163 3,556 152 3,693 157 3,766 160

Retail & repairs 3,365 143 3,432 146 3,421 146 3,408 145

Transportation 3,816 135 3,439 122 3,547 125 3,589 127

IT, telecoms 6,379 166 6,685 174 6,707 174 6,654 173

Financial sector 6,044 136 6,356 143 6,702 151 6,109 137

National average 3,878 154 3,741 149 3,613 144 3,652 145

Source: Central Statistical Office (GUS)

Construction OutputConstruction OutputConstruction OutputConstruction Output

Month Apr '13 May '13 Jun '13 Jul '13 Aug '13 Sep '13 Oct '13

m/m (%) +7.9 +16.1 +19.1 +7.8 -0.8 +9.4 +14.3

y/y (%) -23.1 -27.5 -18.3 -5.2 -11.1 -4.8 -3.2

Year 2006 2007 2008 2009 2010 2011 2012

y/y (%) +18.1 +15.5 +12.1 +5.1 +4.6 +11.8 -0.6

Source: The Central Statistical Office of Poland, GUS

Sentiment IndicatorsSentiment IndicatorsSentiment IndicatorsSentiment Indicators

Economic sentiment and consumer confidence indicators

-40

-20

0

20

60

80

100

120 Consumer confidence (left axis)

Economic sentiment (right axis)

The economic sentiment (1990-2010 average = 100) is a composite made up of 5 sectoral confidence indicators, which are arithmetic means of seasonally adjusted balances of answers to a selection of questions closely related to the reference variable. Source: Eurostat

Producer PriceProducer PriceProducer PriceProducer Pricessss

Month Apr '13 May'13 Jun '13 Jul'13 Aug'13 Sep'13 Oct'13

m/m (%) -0.7% +0.1 +0.7 +0.2 -0.3 +0.1 -0.5

y/y (%) -2.1% -2.5 -1.3 -0.8 -1.1 -1.4 -1.3

Year 2006 2007 2008 2009 2010 2011 2012

y/y (%) +2.0 +2.0 +2.2 +3.4 +2.1 +7.6 +3.3

Construction PriceConstruction PriceConstruction PriceConstruction Pricessss

Month Apr '13 May'13 Jun '13 Jul'13 Aug'13 Sep'13 Oct'13

m/m (%) -0.1 -0.2 -0.1 -0.1 -0.2 -0.1 -0.1

y/y (%) -1.9 -2.0 -2.0 -1.9 -1.9 -1.8 -1.7

Year 2006 2007 2008 2009 2010 2011 2012

y/y (%) +3.2 +7.4 +4.8 +0.2 -0.1 +1.0 +0.2

IndustriaIndustriaIndustriaIndustrial Outputl Outputl Outputl Output

Month Apr '13 May '13 Jun '13 Jul '13 Aug '13 Sep '13 Oct '13

m/m (%) -2.3 -0.7 +2.6 +1.5 -4.5 +9.6 +6.0

y/y (%) +2.7 -1.8 +2.8 +6.3 +2.2 +6.2 +4.4

Year 2006 2007 2008 2009 2010 2011 2012

y/y (%) +11.6 +10.7 +3.6 -3.5 +9.8 +7.7 +1.0

weekly newsletter # 013 / 2nd December 2013 / page 17

TTTTraderaderaderade

Poland exports and imports according to commodity groups, according to SITC classification

EXPORTS in PLN bn IMPORTS in PLN bn

Jan-Sep 2013

y/y (%)

share (%)

2012 share (%)

Jan-Sep 2013

y/y (%)

share (%)

2012 share (%)

Food and live animals 49,806 +9.4 10.6 61,694 10.3 34,538 +4.5 7.3 44,287 6.9

Beverages and tobacco 6,405 +6.7 1.4 7,967 1.3 2,995 +1.2 0.6 3,989 0.6

Crude materials except fuels 11,947 +9.9 2.5 14,024 2.4 15,917 -7.4 3.4 22,053 3.5

Fuels etc 22,200 +0.7 4.7 29,389 4.9 55,502 -11.7 11.6 85,280 13.4

Animal and vegetable oils 1,267 +46.7 0.3 1,342 0.2 1,955 -9.4 0.4 2,887 0.5

Chemical products 43,903 +7.0 9.3 54,295 9.1 69,490 +1.9 14.6 89,140 14.0

Manufactured goods by material 97,528 +1.0 20.7 126,161 21.1 82,985 -3.2 17.5 110,773 17.4

Machinery, transport equip. 176,544 +5.0 37.5 223,646 37.5 156,992 +2.4 33.1 203,718 31.9

Other manufactured articles 60,447 +6.0 12.8 75,925 12.7 42,337 -4.8 8.9 57,646 9.0

Not classified 1,257 n/a 0.2 2,653 0.5 12,229 n/a 2.6 18,515 2.8

TOTAL 471,304 +4.8 100 597,096 100 474,940 -1.8 100 638,288 100

Poland's ten largest trading partners, ranked according to 2012

EXPORTS in PLNbn IMPORTS in PLN bn

No Country Jan- Sep 2013

share *2012 Share No Country Jan- Sep 2013

share *2012 Share

1 Germany 118,119 25.1% 150,046 25.1% 1 Germany 101,785 21.4% 134,933 21.1%

2 UK 30,740 6.5% 40,184 6.7% 2 Russia 59,388 12.5% 91,033 14.3%

3 Czech Rep. 28,868 6.1% 37,475 6.3% 3 China 44,332 9.3% 57,235 9.0%

4 France 26,520 5.6% 34,862 5.8% 4 Italy 24,315 5.1% 32,782 5.1%

5 Russia 25,476 5.4% 32,290 5.4% 5 France 18,262 3.8% 25,303 4.0%

6 Italy 20,214 4.3% 29,067 4.9% 6 Netherlands 17,848 3.8% 24,543 3.8%

7 Netherlands 18,714 4.0% 26,678 4.5% 7 Czech Rep. 17,304 3.6% 23,327 3.7%

8 Ukraine 13,277 2.8% 17,213 2.9% 8 USA 13,299 2.8% 16,436 2.6%

9 Sweden 12,777 2.7% 15,811 2.6% 9 UK 12,704 2.7% 15,509 2.4%

10 Slovakia 12,273 2.6% 15,288 2.6% 10 South Korea n/a n/a 14,619 2.3%

Source: Central Statistical Office (GUS) *) preliminary estimates, full year

CurrencyCurrencyCurrencyCurrency

Central Bank average rates

as of 29 November 2013

100 USD 308.46 ↓

100 EUR 419.98 ↑

100 GBP 503.48 ↓

100 CHF 340.84 ↓

100 DKK 56.31 ↑

100 SEK 47.07 ↓

100 NOK 50.33 ↑

10,000 JPY 301.63 ↓

100 CZK 15.34 ↓

10,000 HUF 139.56 ↓

100 USD/EUR against PLN

300