Literatur Review : Metode Evaluasi Kualitas Usability Website

Upload

poland-today-business-reviewCategory

view

215download

0description

No. 014 / 9th December 2013 / www.poland-today.pl / magazine, conferences, portal, newsletter

1 year subscription: EUR 690 (PLN 2760)

Newsletter Editor: Lech Kaczanowski

tel. +48 607 079 547

Sales Contact: James Anderson-Hanney

tel. +48 881 650 600

MANUFACTURING & PROCESSING

Lotos and Azoty one step closer to PLN 12bn petrochemical project page 2 Economic recovery is gaining traction, PMI data show page 3

BANKING & FINANCE

PKO BP repeats bid on Nordea due to lack of regulatory verdict page 4

ENERGY & RESOURCES

Poland and Slovakia intensify work on gas interconnector page 5

Developer Mostostal Export shifts focus to minerals exploration and mulls London listing page 6

PROPERTY & CONSTRUCTION

Kulczyk Silverstein to turn Holland Park into Ethos, add more space page 6

Belgian OKRE gets permit for 2nd office project in Warsaw page 7

SERVICES & BPO

P&G to create 500 jobs at new supply chain planning centre in Warsaw page 8 Executive search firm Horton International finds partner in Poland page 9

TRANSPORT & LOGISTICS

PESA gets first of many lucrative orders from Deutsche Bahn page 9

Rail frright firm PKP Cargo gets PLN 200m EBI loan for fleet modernization page 10

CONSUMER GOODS & RETAIL

British firm McKinlay Development open their first Polish retail park page 11

POLITICS & ECONOMY

Sejm approves pension reform bill page 14

KEY FIGURES

Up-to-date macroeconomic figures, currency & stock market data and lots of other hard-to-find info pages 15-17

The transaction makes BNP Paribas Poland's 8th largest bank by assets. Photo: BNP Paribaa

BNP Paribas BNP Paribas BNP Paribas BNP Paribas acquiresacquiresacquiresacquires BGŻ for EUR 1bnBGŻ for EUR 1bnBGŻ for EUR 1bnBGŻ for EUR 1bn Dutch Rabobank has agreed to sell its Polish unit BGŻ to France's BNP Paribas for EUR 1bn. The transaction will give the French lender the critical mass it needs in order to challenge other European giants operating on the Polish market. page 3

Montagu sells Emitel to AlindaMontagu sells Emitel to AlindaMontagu sells Emitel to AlindaMontagu sells Emitel to Alinda European private equity giant Montagu has sold Poland's leading television and radio broadcast infrastructure operator Emitel to US-based Alinda Capital Partners in one of this year's largest M&A deals in the CEE region. page 12

weekly newsletter # 014 / 9th December 2013 / page 2

MANUFACTURING & PROCESSING

Lotos and Azoty one Lotos and Azoty one Lotos and Azoty one Lotos and Azoty one step closer to PLN 12bn step closer to PLN 12bn step closer to PLN 12bn step closer to PLN 12bn petrochemical projectpetrochemical projectpetrochemical projectpetrochemical project

Poland's number two oil refiner Grupa Lotos and chemicals conglomerate Grupa Azoty decided to go ahead with full feasibility study for their joint PLN 12bn petrochemical project, with possible participa-tion of Poland's investment vehicle Polskie Inwestycje Rozwojowe (PIR), the companies said in a press release. Following the completion of a pre-feasibility study, on 3rd December the two companies signed a deal on establishing an SPV. Upon completion of the feasibility study, an invest-ment decision is expected to be made in 2014. If the project is given the green light and the financing struc-ture agreed, construction of the complex will occur throughout 2016-2018, with operations commencing in 2019. Lotos and Azoty seek to develop a brand new petrochemical plant next to their existing installations. According to the companies, in terms of scale, the planned complex is on a level with the construction of a new refinery. The project's value is estimated at approximately PLN 12bn, making it the largest investment in the Polish in-dustrial sector in recent years. According to the two partners, the complex will help reduce Poland's chem-ical trade deficit, and will create between 5,000 and 7,000 jobs during the construction stage, and approx-imately 2,000 new jobs following commencement of its commercial operation. "Together with Grupa Azoty and PIR, we want to forge a link between the refining and chemical indus-

tries in Poland, creating a force that will drive the country's future economic growth," commented Paweł Olechnowicz, President of the Grupa Lotos Manage-ment Board.

Lotos and Azoty are seeking synergies in joint pro-duction of chemicals. Photo: Grupa Lotos Currently, Poland imports large volumes of chemical products, with the country's balance of trade at a nega-tive PLN -16.7bn in 2012 (organic chemicals and plas-tics in primary form). At the same time, Polish refiner-ies are holding a surplus of light fractions from crude oil processing, including raw gasoline and LPG, which are the perfect feedstock for petrochemical produc-tion. Lotos and Azoty argue that the integration of their raw materials bases will benefit the entire econ-omy, while the companies themselves will be able to diversify their production and revenue streams by in-troducing a range of new high-margin products. At the national level, the proposed project is to help improve Poland's trade balance, increase its export opportuni-

ties for high-margin chemical products, and provide the domestic industrial sector with access to state-of-the-art technologies from around the world. The two firms also inked a preliminary deal with Po-land's state investment vehicle PIR as a potential fi-nancial investor for the project. Created last year as part of the government's "Polish Investments" pro-gram to stimulate economic recovery by investing fu-ture privatization proceeds into projects of strategic importance, PIR has recently agreed to inject up to PLN 563m in Lotos Petrobaltic's B8 exploration pro-ject in the Baltic Sea (see PT Business Review+ No. 007 page 5). "If the undertaken feasibility study yields favorable re-sults in terms of profit and risk, PIR will engage in talks with Lotos and Grupa Azoty on the detailed terms of the planned transaction. PIR may then allo-cate up to PLN 750m to the project," said Mariusz Grendowicz, President of PIR's Management Board. "In parallel with the feasibility study, we will be con-ducting negotiations with other potential partners willing to join in this landmark venture, who could be particularly interested in specific products or process units. At that point, a preliminary analysis of the fi-nancing structure will also be conducted," added Jacek Socha, Vice-President of PwC Polska, the leader of the advisory consortium working on the preliminary fea-sibility study for the project. Although the entire undertaking is still at a very early stage, it fits with the action plan adopted by Poland's Treasury Ministry, which is a strong proponent of ex-ploring the potential synergies between the largest Polish companies and creating the so-called "national champions." Grupa Lotos has a solid track record in delivering large industrial projects, as exemplified in its 10+ Program, implemented over the 2007-11 period, which cost roughly a half of the estimated price tag on the new petrochemical complex.

weekly newsletter # 014 / 9th December 2013 / page 3

MANUFACTURING & PROCESSING

Economic recovery is Economic recovery is Economic recovery is Economic recovery is gaining traction, PMI gaining traction, PMI gaining traction, PMI gaining traction, PMI data showdata showdata showdata show

Poland's purchasing managers' index PMI moved up to 54.4 points in November, the highest level since April 2011, from 53.4 pts in October, supported by strong demand from both domestic and export mar-kets, a PMI report by HSBC and Markit showed. It was the fifth consecutive month when the indicator remained above the key 50-point threshold, which separates expansion from contraction, indicating im-proving business conditions in manufacturing. New orders increased at the fastest rate since the start of 2011, and output rose at the strongest pace in over two-and-a-half years as a result. Inflationary pressures remained historically weak, with input prices rising only moderately and output prices declining further.

Purchasing Managers' Index (PMI)

The 50 mark separates growth from contraction

45

50

55

Sep 12 Nov 12 Jan 13 Mar 13 May 13 Jul 13 Sep 13 Nov 13

Source: Markit & HSBC

"The improvement was broad- based while higher new orders and output contributed the strongest. Firms re-ported improving demand from both domestic and ex-port markets, and higher sales volumes on the back of price cuts. It has been the fifth month running in No-vember when rising input prices were accompanied by falling output prices," commented Agata Urbańska-Giner, Economist, Central & Eastern Europe at HSBC. "Improving activity has sustained a positive growth rate of employment for the fourth month running in November following eleven months of contraction earlier on. Growing new export orders have not been reflected in exports data to date this year with exports growth rates trending sideways. But growth of indus-trial production has been slowly picking up from -1.2% y/y in Q1, +1.1% in Q2, +3.5% in Q3 and 3.8% y/y in Oc-tober. The PMI survey as well as the economic senti-ment indicators by the Polish statistical office point to continuation of this gradual upward trend in the com-ing months," she added.

BANKING & FINANCE

BNP Paribas BNP Paribas BNP Paribas BNP Paribas acquires acquires acquires acquires BGŻ from Rabobank BGŻ from Rabobank BGŻ from Rabobank BGŻ from Rabobank for EUR 1bnfor EUR 1bnfor EUR 1bnfor EUR 1bn

Less than a month after we reported on plans by France's BNP Paribas to acquire its Dutch rival Rabobank's Polish subsidiary BGŻ (see PT Business Review+ No. 010 page 3), the two European giants have sealed the deal, in what is the latest example of consolidation in Poland's banking sector. If approved by Poland's regulator KNF, which has been increasing-ly critical of large bank mergers, the PLN 4.2bn trans-action will teleport BNP Paribas to No. 8 position in Poland.

"The acquisition of Bank BGŻ constitutes a major step towards attaining a critical size in Poland. The trans-action will establish the BNP Paribas Group as a refer-ence player in Poland's banking sector," commented Jean-Laurent Bonnafé, CEO of BNP Paribas Group. "We are convinced that the combination of Bank BGŻ expertise, notably in the agri & food business and in e-banking, with the existing operations of BNP Paribas Bank Polska will create a unique player among Polish banks with significant growth prospects," added Stef-an Decraene, Head of BNP Paribas International Re-tail Banking and a Member of the BNP Paribas Execu-tive Committee. The deal offers a 14% premium to the market value of BGŻ, a rural-based Polish lender which ranks No. 11 by assets. BNP, which will buy 98.5% of BGŻ, has said it is looking to expand into faster-growing markets and buying BGŻ could yield benefits from integrating it with the group's existing Polish business BNP. Bank BGŻ is a universal commercial bank, serving retail and institutional clients. With a network of nearly 400 branches, it specializes in financing agriculture, the food economy and regional infrastructure. In the first three quarters of the year BGŻ boosted its net earnings by 73% y/y, reaching PLN 134m. Net lending remained unchanged from the end of 2012 at PLN 26.3bn, whereas deposits dropped 4% and totaled PLN 25.8bn. The bank's solvency ratio stood at 13.1% as of end of September 2013. Last year Rabobank increased its ownership in the Polish lender by 40%, reaching the current 98.5% and later boosted the bank's equity by PLN 0.5bn. At the end of October the Dutch bank confirmed plans to merge its Polish unit Rabobank Polska that serves primarily large corporate clients, with BGŻ. Rabobank Polska were to become a separate division of BGŻ fo-cusing on corporations. Rabobank, the biggest Dutch retail bank was recently fined USD 1bn over its in-volvement in the Libor rigging scandal and did not of-

weekly newsletter # 014 / 9th December 2013 / page 4

ficially put BGŻ up for sale, saying instead that it was reviewing its options for the Polish bank. Besides BNP, Italy's UniCredit and Spain's Banco Santander have expressed interest in the unit in recent months. In most of the markets where it operates, Rabobank is among the top three-top five players, but in Poland the only way to achieve such a position would be through acquisitions.

BNP Paribas will be one of Poland's Top Ten banks. Photo: BNP Paribas

Foreign banks control about 70% of the Polish banking sector, but several have looked for an exit to boost cap-ital positions hit by the global economic crisis, with others being keen to strengthen their foothold in an economy which has outperformed much of the euro zone in recent years. Major recent exits from Poland's banking market included Belgium's KBC and Ireland's AIB which sold their Polish units to Spain's Santander, Greek Eurobank EFG (their Polbank EFG merged with Raiffeisen Polska), and Swedish Nordea (their Polish arm is to be acquired by Poland's largest lender PKO BP for PLN 2.83m – see the next story). The Polish unit of BNP Paribas posted net earnings of PLN 78.2m in Q1-Q3 2013, up from PLN 19m in the

corresponding period of 2012. With 222 retail units and nine business centers, the bank serves 363,000 re-tail customers and 33,000 small and medium-sized companies. Globally, BNP Paribas has a presence in nearly 80 countries with 190,000 employees, including 145,000 in Europe, focusing on retail banking, invest-ment solutions as well as corporate & investment banking. With combined assets of more than PLN 56bn, the new BNP Paribas-BGŻ will remain far behind the top four lenders (PKO BP: PLN 200bn+Nordea's PLN 30bn; Pekao SA: PLN 150bn, mBank and BZ WBK (each with PLN 100bn in assets), but it will become a worthy rival for the likes of Raiffeisen Bank, Getin Noble, Millennium Bank and even ING BSK. The top ten of Poland's banking sector is therefore looking increasingly well-defined.

BANKING & FINANCE

PKO BP repeats bid on PKO BP repeats bid on PKO BP repeats bid on PKO BP repeats bid on Nordea Nordea Nordea Nordea due to lack of due to lack of due to lack of due to lack of regulatory verdictregulatory verdictregulatory verdictregulatory verdict

Although exactly half a year has passed since Poland's top lender PKO BP agreed to acquire 100% in Nordea Bank Polska from the Swedish banking group Nordea, the PLN 2.83bn transaction is yet to be concluded due to the lack of green light from the Polish regulator KNF. As the original tender offer placed by PKO BP had since expired, the Polish bank announced a new one on 3rd December, maintaining the price unchanged at PLN 47.99 per share. Subscrip-tions in the new offer will be accepted from 23rd De-cember 2013 through 25th February 2014. According to Bloomberg, the Nordea deal were to be Poland's

biggest M&A transaction this year, but now it seems like it will be booked in 2014. It is hardly a surprise that Polish regulatory bodies are taking their time to review the transaction. Shortly af-ter the Nordea deal had been announced KNF said the current level of concentration in Poland's banking sec-tor was "close to optimal" and therefore it would care-fully scrutinize any takeover transaction on that mar-ket. "From the point of view of systemic risks and of the safety of the financial system it is important that there are no too large banks in Poland, i.e. such whose potential problems could not be resolved based on domestic instruments of crisis management," the regu-lator added.

Nordea's exit from Poland is taking longer than ex-pected. Photo: Nordea On June 12 PKO BP agreed to buy 99.21% in Nordea Bank Polska for PLN 2.642bn, 100% in life insurer Nordea TUnŻ for PLN 180m and 100% in leasing and factoring firm Nordea Finance Polska for PLN 8m from Nordea AB, which decided to pull out of the Polish market. PKO BP said that it would take steps to acquire the remaining shares from minority share-holders and delist the Nordea unit from the Warsaw

weekly newsletter # 014 / 9th December 2013 / page 5

Stock Exchange. The Nordea Operations Centre in Łódź and its Polish pension fund company will not be affected by the transaction. "The Polish banking market is consolidating. The competitive landscape will change in favor of large banks with scale in the market. Nordea Bank Polska is currently the 12th largest bank in the country, and we would have to make large investments in the coming years to be competitive. At the same time the new re-quirements from the Polish authorities make it in-creasingly challenging for us to pursue our uniform operating model, and eventually meet our financial targets in the Polish business," Christian Clausen Nordea Group CEO explained the logic behind their exit. Only a few years ago Nordea had very ambitious plans for the Polish market. It had a goal of operating 400 branches by 2010 and of doubling its market share to 8%. After poor results in 2012, with operating profit falling to EUR 78m from EUR 95m in 2011 and with net loan losses up from EUR 14m to EUR 37m, the Scandinavian lender had to substantially revise its former targets. In recent years, stricter governance and operational practices have been imposed on Polish banks, including a requirement to list at least 25% of their shares on the Warsaw Stock Exchange. Nordea Bank Polska today has a free float of 0.8%. According to estimates PKO BP published in June, the acquisition were to help the Polish bank increase its assets by 16%. Its profit per share is expected to rise by 10% and the return on investment should be 13%. PKO BP's network in Poland's largest cities will expand by 25% and its portfolio of wealthy customers will ex-pand by 8%, the Polish bank said. In short, the deal seals PKO's position as Poland's number one lender, boosting its share in the banking sector's totals assets from 15% to 18%. The number two player, Italian-

owned Pekao SA has 11%. PKO's share in retail loans will increase from 17.5% to 20.7%.

ENERGY & RESOURCES

Poland and Slovakia Poland and Slovakia Poland and Slovakia Poland and Slovakia sssspeed uppeed uppeed uppeed up work on work on work on work on key key key key gas interconnectorgas interconnectorgas interconnectorgas interconnector

At the end of November the governments of Poland and Slovakia inked a cooperation agreement on the connection of the two countries' natural gas transmis-sion systems. With a estimated price tag of PLN 1.3bn, the planned interconnector will contribute a an im-portant element to the region's gas distribution net-work, which is being currently being expanded under the umbrella of the European North-South infrastruc-ture corridor. The interconnection is stimulate compe-tition in the region's gas market, among other by providing both countries with more diversified gas sources and transmission routes as well as security of gas supplies, Polish operator Gaz-System said in a statement. The new cross-border pipeline between Poland and Slovakia may provide the Polish market with access to gas supplies from the so-called Southern Corridor, which is to carry natural gas from the Caspian Sea through the Baumgarten gas hub or the recently built Slovakia-Hungary interconnection, therefore further reinforcing the stability of natural gas supplies to Po-land. Moreover, it will give Slovak entities access to gas offered in the Polish market, including LNG from the terminal that is to open next year in Świnoujście currently constructed, as well as Poland's gas storage caverns. The project will also potentially enable Po-land to export supply gas from unconventional sources, such as shale, to other European countries.

Gaz-System and its Slovakian counterpart Eustream have been working on the project since early 2009, and according to the two partners, a new two-way cross-border pipeline with auxiliary infrastructure, could be operational by the end of 2018, at the earliest. The pipeline leading to Poland will have a capacity of 5.7bn cb.m per annum in phase one to be increased to 9.5bn cb.m in phase two, whereas the one pumping gas in the opposite direction (to Slovakia) will be capable of transmitting up to 4.7bn cb.m.

Gaz-System seeks to improve Poland's energy secu-rity by developing cross-border interconnectors. Photo: Gaz-System

The feasibility studies and other analytical work on the project have already been completed and the two operators are hoping to start building the new inter-connector next year. In a list of 248 key energy sector projects, published by the European Commission in mid-October, the Poland-Slovakia gas interconnection was assigned a PCI (Project of Common Interest) sta-tus under the priority corridor: North-South gas inter-connections in Central Eastern and South Eastern Eu-rope, making it potentially eligible for partial EU fund-ing.

weekly newsletter # 014 / 9th December 2013 / page 6

Under its ambitious investment program, Gaz-System seeks to build more than 1,000 km of new gas pipelines by 2014, mainly in north-western and central Poland. Thanks to the ongoing development of Poland's gas transmission network and other recent investments, the country now has technical capabilities to obtain up to 43% of its gas import from suppliers other than Russia, compared to merely 9% back in 2011. So far Po-land has built interconnectors to Germany (1.5bn cb.m/year) and Czech Republic (0.5bn cb.m/year; to be increased tenfold in 2017/18) and it is taking ad-vantage of virtual reverse flow services on the Yamal pipeline (to be turned into an actual two-way link with a capacity of 5.5bn cb.m/year). Next year the country is hoping to launch the LNG terminal in Świnoujście (5bn cb.m).

ENERGY & RESOURCES

Developer Mostostal Developer Mostostal Developer Mostostal Developer Mostostal Export Export Export Export sssshifts focushifts focushifts focushifts focus to to to to minerals exploration minerals exploration minerals exploration minerals exploration and mullsand mullsand mullsand mulls LSELSELSELSE listing listing listing listing

Warsaw-listed construction and property develop-ment company Mostostal Export has picked a new strategic investor – a mysterious Luxembourg-based fund Tarantoga Capital, which specializes in explo-ration and development projects in the mineral re-sources sector and owns a balanced portfolio of cop-per, coal, gold and other conventional assets across Central Asia and West Africa.

Under the new owner, Mostostal Export will shift its focus from construction to mineral prospecting and exploration. According to Mostostal's board, the com-

pany will take up first projects in the new business ar-ea in early 2014. "Our intention is to acquire an exploration company in Mongolia that operates on an area of 14,000 sq.km, which corresponds to roughly 5% of the total area of Poland. This is an exploration potential that no other Warsaw-listed company can match at the moment," commented Wielkosław Staniszewski, member of Mostostal Export's board. Mostostal is eyeing the Mongolia's Bayankhongor province, which is particularly rich in copper as well as gold and coal. The planned acquisition of a Mongo-lian license holder is to be completed by the end of January 2014, Mostostal said. As the world's top exploration and extraction compa-nies are listed either in London, Toronto, or Sydney, Mostostal Export is determined to carry out a listing on the London Stock Exchange in 2014. "Advisors for the process will be chosen in early 2014. Due to the scale of the undertaking we will cooperate with international consultancies and investment banks. If all goes as planned, Mostostal's shares will be listed on the London market in Q3 2014," declared Staniszewski. Established in early 1980s, Mostostal Export has been listed on the Warsaw Stock Exchange since 1992. To-date its key focus was on construction and develop-ment, including projects in the Commonwealth of In-dependent States. The once profitable company was badly affected by the crisis as well as shareholder con-flicts. Last year it nearly went bankrupt, following a net loss of PLN 47m on PLN 33m worth of revenues it saw in 2011. The help came from Calatrava Capital, a listed Polish fund which purchased more than PLN 90m worth of Mostostal bonds. Investor reaction to Mostostal plans has been rather lukewarm.

PROPERTY & CONSTRUCTION

Kulczyk Silverstein to Kulczyk Silverstein to Kulczyk Silverstein to Kulczyk Silverstein to turn Holland Park into turn Holland Park into turn Holland Park into turn Holland Park into Ethos, add more space Ethos, add more space Ethos, add more space Ethos, add more space

Real-estate investment firm Kulczyk Silverstein Properties (KSP), a joint project of Polish billionaire Jan Kulczyk and New York property mogul Larry Sil-verstein is gearing up to begin a major makeover of the Holland Park office complex on Warsaw's Plac Trzech Krzyży Square, across the street from the stock ex-change building. Built in late 1990s, Holland Park has long housed the Polish offices of Dutch financial group ING, but the latter has moved to the newly-built Plac Unii complex. KSP, which acquired the project in ear-ly 2013, has decided to take the opportunity to mod-ernize the property. Holland Park consists of two buildings - a six story tall main building, and a lower one, known as Piano. Total office space of the building amounts to 10,416 sq.m. The building comprises 1,418 sq.m of retail space as well as 106 underground and surface parking spaces. KSP intends to refurbish, extend and reposition Hol-land Park, which will be known under a new name - Ethos. The main repositioning feature of the building will be the reconfiguration of the ground floor retail which will almost double its current size and will amount to approximately 2,500 sq,m. The Plac Trzech Krzyży area has recently evolved into Warsaw's luxury shopping district and KSP is hoping the new, expand-ed retail section of Ethos to attract some top brands. The works will include BREEAM certification for the existing building and the new build extension that will increase the building's total office GLA to 13,100 sq.m, creating larger floors (up to 3,000 sq.m). Although the investor is yet to apply for all the necessary permits, it

weekly newsletter # 014 / 9th December 2013 / page 7

is hoping to begin the redevelopment in early 2014 and complete the project by the end of 2015.

The Holland Park complex, built in late 1990s, is to be given a major makeover. Image: KSP Holland Park, which KSP acquired from a fund man-aged by CBRE Global Investors in March 2013 for an undisclosed amount, is KSP's fourth acquisition in Warsaw. Last year the company purchased two office buildings located in a prestigious part of Warsaw from Germany's Hochtief Development Poland. Follow-ing the planned renova-tions and expansion, which is to reach completion by mid-2014, the Malachowskiego Square building will offer 7,600 sq.m of offices and 1,500 sq.m of retail and storage space, as well as 100 underground parking spaces. As for the other property (on Mazowiecka St.), it is also undergoing comprehen-sive modernization in the coming months with 2,250 sq.m of office and 750 sq.m of class-A retail or service space. KSP's first acquisition in Warsaw was the 10,700-sq.m Stratos Office Center the company bought back in August 2011. KSP is also managing three other office properties in Warsaw: Ufficio Primo, Krucza House, and Warta Tower. Despite some progress on the development front, Kulczyk and Silverstein's other project, the institu-

tional real estate investment management platform KSP Real Estate Investment Management (KSP REIM) they set up jointly last year has been put on a back burner. The two former Heitman executives Otis Spencer and Dennis Dart, who were supposed to drive KSP REIM's expansion, have since jumped ship and fundraising has been suspended, officially due to "un-favorable market conditions." According to original plans, KSP REIM were to be-come the preeminent real estate fiduciary in Central and Eastern Europe by launching Luxembourg regu-lated closed-end funds intended for institutional in-vestors seeking exposure to the dynamic and increas-ingly liquid CEE real estate market. The first closing of the KSP REIM’s initial fund was planned for mid-2013 and the company was hoping its assets under man-agement to reach more than EUR 1.5bn. As for the former KSP REIM executives, Otis Spencer became the managing director of Peakside Group and CEO of Peakside Polonia Management whereas Dennis Dart joined the Olczak-Klimek van der Kroft Węgiełek law firm.

PROPERTY & CONSTRUCTION

Belgian OKRE gets Belgian OKRE gets Belgian OKRE gets Belgian OKRE gets permit for 2nd office permit for 2nd office permit for 2nd office permit for 2nd office project in Warsawproject in Warsawproject in Warsawproject in Warsaw

Belgian-owned property company OKRE Develop-ment has obtained a valid building permit for Grójecka Offices, its new class-A office project in War-saw's Ochota district. Designed by the renowned War-saw's studio Kuryłowicz & Associates, the project will provide 7,400 sq.m of GLA, including eight office stories, ground floor retail space, underground parking

lot with 134 spaces, bicycle storage, as well as a num-ber of energy saving and environmentally solutions that have earned Grójecka Offices an "Excellent" grade under the BREEAM certification system.

"In our office buildings nobody is billed for media in relation to rented space, but only for actually used me-dia, precisely measured. This generates savings for every tenant and this is what today's market expects. This type of property development is in the best tradi-tion of our firm and I am happy that it is well appreci-ated in Poland," commented Ronnie Richardson, CEO of OKRE Development.

OKRE's new Grójecka Offices project will hold a BREEAM "Excellent" certificate. Image: OKRE

Grójecka Offices is OKRE's second office project in Warsaw, after the class-A office building GreenWings, which is currently nearing completion on 17 Stycznia Street, merely a stone’s throw from the Chopin air-port, close to the LOT Polish Airlines headquarters. The seven-story wing-shaped building will include close to 11,000 sq.m of offices, 270 parking places at an underground lot, and 80 bicycle racks together with dressing rooms and showers for all those brave enough to dodge the Warsaw traffic on two wheels. With a "very good" BREEAM assessment, GreenWings is to welcome its first tenants in May 2014.

weekly newsletter # 014 / 9th December 2013 / page 8

With offices in Warsaw and Poznań, OKRE Develop-ment has been operating on the Polish market since 1997. Besides the office projects in Warsaw, its recent developments included the Na Skraju Lasu housing es-tate in Poznań (139 flats). OKRE Development belongs to a Belgian development and project management company OKRE, which has completed a number of in-vestments in Poland, including Jerozolimskie Business Park in Warsaw (16,500 sq.m of office space), Jutrzenki Business Park in Warsaw (2,738 sq.m), Winogrady Business Center in Poznan (7,330 sq.m), Galeria Indomo in Lubin (9,577 sq.m of commercial space) and Park Residence in Warsaw.

Warsaw office market Key indicators as of end of 1H 2013

Office zones Stock

sq.m

Vacan-

cy

Central locations 1,287,000 9.9%

CBD-Central Business District 501,000 11.4%

CCF-City Centre Fringe 786,000 8.9%

Non-central locations 2,724,000 10.8%

E-East (Praga) 172,000 9.8%

LS-Lower South (Puławska) 176,000 13.0%

N-North (Żoliborz) 135,000 9.0%

SE-South East (Wilanów & Sadyba) 188,000 2.2%

SW-South West (Jerozolimskie & Okęcie) 660,000 15.6%

US-Upper South (Mokotów) 1,105,000 10.5%

W-West (Wola) 288,000 6.4%

Total 4,011,000 10.5%

Source: CBRE H1 2013 Warsaw Office MarketView

OKRE is a joint venture of Otreco NV, a Belgian company with over 30-year experience in the devel-opment market, and Koramic Real Estate NV, part of Belgium’s Koramic Investment Group. Otreco has offices in Belgium, France, Poland and Bulgaria with a staff of more than 40 people. The company specializes in turnkey projects, especially in residential and office buildings, shopping centers, warehouses and holiday

properties. Koramic was established in 1883 as roof tiles factory and nearly a century later a property in-vestment and management unit Koramic Real Estate was spun off from the group.

SERVICES & BPO

P&G to create 500 jobs P&G to create 500 jobs P&G to create 500 jobs P&G to create 500 jobs at Warsaw supply at Warsaw supply at Warsaw supply at Warsaw supply chain planning centrechain planning centrechain planning centrechain planning centre

Global consumer products giant P&G has officially launched its Warsaw Planning Service Center (PSC) a completely new unit that will be in charge of devel-opment and implementation of innovative solutions across the company's supply chain in 100 countries worldwide. The Warsaw project will create 500 jobs, P&G representatives announced on 5th December at a press conference co-hosted by Poland's investment promotion agency PAIiIZ, which supported the pro-ject. "We chose Warsaw and Poland due to P&G's earlier investments in the country, its proximity to other markets, business-friendly climate, and availability of qualified staff," Yannis Skoufalos, Global Product Sup-ply Officer P&G. "Our new planning and supply chain centre in Warsaw is a milestone project, but certainly not our last," added Werner Geissler, Vice Chairman, Global Operations. Recruitment for the centre is currently underway, with open positions for university graduates with technical & science degrees as well as leadership, problem-solving and language skills. P&G currently employs an estimated 3,500 full-time staff in Poland, where it has four factories, exporting

to 100 global markets, as well as a head office with a shares services centre. Its key manufacturing opera-tions in Poland include the Warsaw baby care plants, making Pampers diapers and baby wipes, the Olay body & face care unit in Aleksandrów Łódzki, just out-side Łódź, as well as the razor & blade factory in Łódź: the largest producer of Gillette and Venus-branded shaving products worldwide. The US corporation, which employs more than 126,000 people worldwide, has invested more than PLN 4bn in Poland to-date.

Yannis Skoufalos, Global Product Supply Officer, P&G, Werner Geissler, Vice Chairman, Global Opera-tions P&G, and Monika Piątkowska, Deputy Hdead of PAIiIZ at the opening of P&G's Warsaw Planning Ser-vice Center. Photo: PAIiIZ One of the world's largest consumer firms, P&G turned over a massive USD 84.2bn and earned USD 11.31bn in net-profits in financial year 2013. Each of its 25 top brands that include Always, Ambi Pur, Ariel, Bounty, Duracell, Fairy, Gillette, Head & Shoulders, Lenor, Olay, Oral-B, Pampers, Pantene, Tide, Vicks, and Wella, generates more than USD 1bn in annual sales. Its advertising expenditure came to USD 9.7bn last year.

weekly newsletter # 014 / 9th December 2013 / page 9

SERVICES & BPO

Executive search firm Executive search firm Executive search firm Executive search firm Horton International Horton International Horton International Horton International finds partner in Polandfinds partner in Polandfinds partner in Polandfinds partner in Poland

Global executive search network Horton Interna-tional has entered the Polish market by teaming up with a local company Executive People, which re-cruits managerial staff and senior management. Exec-utive People will from now on operate under the brand Horton International Poland as Horton's exclu-sive partner on the Polish market. "Both sides were seeking a partner. Executive People wanted to become part of a global executive search in-tegrated firm and we were looking for a long-term partner in the Polish market. We see huge potential in Poland for both the domestic market and for cross border opportunities with our international clients," Ross Eades, CEO of Horton Group International Lim-ited (HGIL), tells Poland Today. Horton International was founded in 1978 in Avon, Connecticut, USA, by Robert Horton. It is an executive search network specializing in the recruitment of sen-ior talent. In the 1980s, the firm began its international expansion into Europe, the Asia-Pacific region and the Americas. HGIL was formed in 1995 by the founding Horton International partners in the US, UK, France, Germany, Italy, Australia and Spain. HGIL continues to serve as the governing body for the firm, establish-ing global policies, procedures and guidelines for all international partner firms. "We have partners, not subsidiaries, operating in 50 office locations across 27 countries, including Poland.

Horton operates on a long-term basis in all markets based on license agreements," Mr. Eades explains. Clients of the Horton International network include some of the largest companies in the world from the Forbes Global 2000 as well as start-ups. The firm’s consultants specialize in such industries as automo-tive, aviation and defense, maritime, logistics, manu-facturing, FMCG, energy and natural resources, fi-nance, technology, healthcare and pharmaceuticals, media and entertainment, retail, fashion and luxury goods, and life science. Executive People (now Horton International Poland) launched operations over 16 years ago as a division of the HR consultancy People, from which it was spun off earlier this year. From an office in Warsaw, its con-sultants specialize in search and consulting projects for industries that include pharmaceuticals, FMCG and retail, manufacturing, TSL, construction, tele-communications, banking and finance, and IT/technology. Apart from recruitment of executives and managerial staff, the firm's services also include close cooperation at the phase of interviews, negotia-tions, post-hiring consultations and on-boarding. Its clients include such companies as Sanofi Aventis, Co-ca-Cola HBC, Perfetti Van Melle, Citi Handlowy, Sodexo Motivation Solutions, Netia, Borg Automotive and Budimex. Horton International Poland will be headed by Paulina Baranowska, Managing Partner, previously managing partner of Executive People. "The executive market in Poland is competitive but not saturated. It is an immature market where we see a gap. We link local knowledge with the global market. Our knowledge and experience and the network of contacts we have built on international markets over the years can contribute significant added value for clients of Horton International in Poland. We are de-lighted to now have, in Poland, a large established team, larger than the teams of competitors specialized

in recruiting C-suite and senior management," con-cludes Horton's CEO.

TRANSPORT & LOGISTICS

PESA PESA PESA PESA receivereceivereceivereceives first of s first of s first of s first of many lucratimany lucratimany lucratimany lucrative orders ve orders ve orders ve orders from Deutsche Bahnfrom Deutsche Bahnfrom Deutsche Bahnfrom Deutsche Bahn

Deutsche Bahn subsidiary DB Regio has ordered 36 new diesel-multiple units (DMUs) from Polish PESA in the first tranche of a EUR 1.2bn framework contract with the Bydgoszcz-based rolling stock manufacturer. The EUR 120m order includes 20 two-car and 16 three-car LINK model regional trains that will operate on Germany’s Sauerland network and will range in ca-pacity from 100 to 160 seats. DB Regio was selected by Westfalen-Lippe Local Transport, Rhine-Ruhr Transport Association, and North Hessen Transport Association to operate the so-called Sauerland Net-work from December 2016. In 2012, DB signed a framework contract with PESA for a potential 470 new DMUs. The diesel-powered trains, which will meet the latest crashworthiness re-quirements and Stage IIIB exhaust emissions stand-ards, are expected to be delivered by the end of 2018. PESA is to build 120 DMUs with 50 to 100 seats each, capable of travelling at maximum speeds of 120km/h as well as 350 DMUs with 50 to 220 seats and top speeds of 140km/h. The PESA deal Deutsche Bahn's first ever order to a non-German manufacturer. Deutsche Bahn's reputation as operator of the lucra-tive regional railway lines, has been somewhat tar-nished in recent years by technical flaws in trains sup-plied by German units of Siemens and Bombardier, resulting in intensified efforts among public admin-

weekly newsletter # 014 / 9th December 2013 / page 10

istrations to look for private-sector operators to run railway lines. Facing increased competition under new government legislation, DB will have to bid for operat-ing rights contracts on multiple short-distance routes, which are set to expire and be re-tendered in the com-ing years by Germany's federal states. Until recently, the state-owned rail operator boasted a market share of 80% in German regional rail transport, 75% in freight and remains a virtual monopoly on long-distance travel.

PESA's LINK trains were an instant hit with German clients. Image: PESA PESA will be working closely with the German railway industry as many components will be sourced from German suppliers. German engine manufacturer MTU will provide the engines, while the braking systems will be offered by Knorr-Bremse, a Germany-based manufacturer of braking systems for rail and commer-cial vehicles. Deutsche Bahn said the contracts had been drawn up in such a way as to afford the maxi-mum possible flexibility with regard to the size and power of the trains ordered. A couple of weeks ago, PESA secure another order in Germany on the delivery of nine new LINK-type DMUs to NEB (Niederbarniemer Eisenbahn). The Polish firm will supply seven two-car vehicles and two three-car vehicles that will be used to service Berlin-

Templin and Berlin-Kostrzyn Wielkopolski lines, PESA also said. The vehicles house 140 and 200 pas-sengers, respectively and their maximum speed is 140 km/h. Besides DB and NEB, PESA's German custom-ers include private carrier Netinera. PESA supplies locomotives for the Italian, Ukrainian and Lithuanian railways as well as trams for munici-palities in Poland, Hungary, and Romania. The com-pany employs a workforce of 3,500 at factories in Byd-goszcz and Mińsk Mazowiecki, just east of Warsaw. Last year PESA turned over PLN 1.55bn and net-earned PLN 137m. The company belongs to a number of Polish investors, including its top management.

TRANSPORT & LOGISTICS

PKP Cargo PKP Cargo PKP Cargo PKP Cargo obtainsobtainsobtainsobtains PLN 200m EBI loan PLN 200m EBI loan PLN 200m EBI loan PLN 200m EBI loan fofofofor r r r fleet modernizationfleet modernizationfleet modernizationfleet modernization

Shortly after the successful listing of Poland's top rail freight operator PKP Cargo on the Warsaw Stock Exchange, the European Investment Bank (EIB) has agreed to lend the company PLN 200m (EUR 47m) to help the company pay for a large-scale fleet upgrade. Thanks to the EIB loan PKP Cargo will be able to purchase and modernize locomotives and rail cars, as part of its ambitious three-year investment program. "It's worth noting that this is the first loan in the histo-ry of Polish railways to be granted without Treasury collateral, which shows that we are reliable business partner and confirms our excellent financial situa-tion," says Adam Purwin, PKP board member for fi-nance.

According to EIB, which has been supporting rail in-vestments in Poland for more than two decades, by providing new and modernized rolling stock, the pro-ject will increase the quality of freight rail services in Poland, enabling more efficient operation, reducing maintenance costs and energy consumption. In EIB's view, this should help railways compete with other modes of transportation, particularly road, so as to maintain or improve its modal share. Shifting freight flows from other modes to rail will result in reduced vehicle operation costs as well as safety and environ-mental benefits, EIB said. New vehicles will replace the ageing fleet and modernized diesel locomotives will consume less fuel and oil as well as operating with less noise and vibration.

PKP Cargo and its subsidiaries operate a fleet of 2459 locomotives and 63,488 wagons. Photo: PKP Cargo The EIB is the long-term lending institution of the Eu-ropean Union owned by its Member States. It makes long-term finance available at attractive rates for in-vestments that contribute towards EU policy goals. PKP Cargo is the European Union's second largest railway freight company after Deutsche Bahn AG and the first listed one, following its recent PLN

weekly newsletter # 014 / 9th December 2013 / page 11

1.42bn IPO on the Warsaw Stock Exchange, which saw the state-owned Polish railway operator PKP sell 20.9m shares in the business. Foreigners bought 20% of the freight operator with the European Bank for Reconstruction and Development having acquired a 5.27% stake and thus becoming the second-biggest shareholder in PKP Cargo. PKP Cargo saw its revenues drop 9.2% to 2.29bn, in 1H 2013, due to economic slowdown, while its net income slumped 44% to PLN 76.8m. Last year the company carried around 116m tons of freight (mainly hard coal and building materials) and generated net profits of PLN 267m on PLN 5.2bn worth of revenues, down from its record net result of PLN 400m in 2011. War-saw-based PKP Cargo had a 60.3% share in the Polish market in 2012 and controlled 8.5% of total rail freight in the EU. That compares with DB Schenker's 28% and 5.4% shares in the EU and Poland, respectively.

CONSUMER GOODS & RETAIL

British British British British firm McKinlay firm McKinlay firm McKinlay firm McKinlay Development openDevelopment openDevelopment openDevelopment openssss itsitsitsits first Polish retail parkfirst Polish retail parkfirst Polish retail parkfirst Polish retail park in Sochaczewin Sochaczewin Sochaczewin Sochaczew

British-owned company McKinlay Development has completed the final extension of first Polish project, the 20,000 sq.m Multishop retail park in Sochaczew, some 60km west of Warsaw. Anchored by a Tesco hy-permarket and OBI home improvement store, the pro-ject has been expanded by 4,500 sq.m to include 11 new outlets. Located near the Warsaw-Poznań road Multishop is a typical retail park, enabling customers to enter stores

directly from the parking lot, which offers 600 spaces. The construction of the scheme started at the end of 2011. Upon the completion of the third, final phase, 11 new tenants have joined the scheme, including Jysk, RTV Euro AGD, Pepco, Deichmann, CCC, Takko, Martes Sport, Hebe and Olewnik as well as Kolporter newsagent’s store, a laundry and a butcher shop.

Multishop in Sochaczew is home to Tesco hyper-market, OBI DIY store and 11 other tenants. Image: C&W

"Multishop in Sochaczew boasts an excellent location and convenient transport links. New tenants will strengthen the park’s offer and enhance its attractive-ness. The last few years have witnessed a growing de-velopers interest in the development of retail parks, which are an interesting alternative to small shopping galleries in cities such as Sochaczew. We are pleased to have such a retail concept in our portfolio," says Aneta Rogowicz-Gała, head of Property & Asset Man-agement department of Cushman & Wakefield, who have been appointed Multishop's. property manager. C&W currently manages commercial properties total-ing 500,000 sq.m, comprising modern office, retail and industrial properties. Back in 2011 McKinlay Development's key shareholder and CEO Craig Thomas McKinlay said his company were to build 10 Multshop retail parks in Poland with

a combined GLA of more than 200,000 sq.m in five years. His target were regional towns such as Żywiec, Jelenia Góra, Bochnia, Iława, Sieradz and Ciechanów, offering an average catchment of 150,000-200,000.

DATA BOX: RETAIL WAREHOUSES & RETAIL PARKS IN 1H 2013 Total retail park and retail warehouse stock in Poland

stands at 2.4m sq.m, with parks accounting for around

26% of the total. In H1 2013, more than 60,000 sq.m

came onto the market. Another 60,000 sq.m is cur-

rently under construction and scheduled for comple-

tion in 2013–2014, largely in small retail parks. The es-

timated development pipeline provides for a further

100,000 sq.m of retail park and retail warehouse

space by the end of 2015.

Poland’s retail park sector is currently experiencing

rapid growth with a dozen or so developers strongly

active on the market. Retail parks are planned and de-

veloped primarily in small and medium-sized cities,

frequently as small schemes with convenience retail-

ing. The vacancy rate in retail parks stands at around

5%. Large-scale, non-food stores are also expanding

as standalone schemes.

Rents in retail parks are stable at EUR 6-8/

sq.m/month for large units and EUR 9-13/sq.m /month

for medium-sized space. Rents for freestanding retail

warehouses average EUR 6–8/sq m/month.

Source: Cushman & Wakefield

"Our goal at the time was development of regular shopping centers in cities of up to 100,000 inhabitants, albeit with a smaller GLA than in big city malls. Our Sochaczew project is a model example as it combines DIY and grocery retailers with a retail park, petrol sta-tion, and a McDonalds," Zbigniew Dymarkowski, board member at Retail Park Sochaczew, the SPV in

weekly newsletter # 014 / 9th December 2013 / page 12

charge of Multishop, tells Poland Today. "Over the past three years we have witnessed a fast paced expan-sion of discount supermarkets coupled with a slower growth of home improvement retailers in smaller towns, which has affected our plans." The Multishop concept is pretty straightforward: good location near a major intersection, offering good local and regional accessibility, low maintenance costs, plenty of parking and strong grocery/DIY anchors. "The idea is to create a convenient shopping location for local residents, where they are able to quickly ac-cess stores straight from the parking lot. We remain interested in building further retail parks in smaller towns, but since the retail property market is becom-ing saturated relatively quickly, we are now contem-plating entry into residential developments as well," adds Mr. Dymarkowski.

CONSUMER GOODS & RETAIL

DIY chain NOMI DIY chain NOMI DIY chain NOMI DIY chain NOMI files files files files for bankruptcyfor bankruptcyfor bankruptcyfor bankruptcy

Poland's oldest DIY retailer, NOMI has filed for bank-ruptcy protection, hoping to settle with its creditors and find new investors in the coming months. The company, which until recently had been the sector's fifth largest player, was badly hit by the decline in de-mand for home improvement goods at the end of 2012 and in early 2013. Despite cost-cutting efforts, recently NOMI has not been able to pay its bills in a timely fashion, which prompted its board to apply for bankruptcy protection. The management hopes NOMI will pay back all its debts over the next six years, with a portion of its dues to be converted into shares. The company is to under-

go a large-scale reorganization that will see the num-ber of NOMI outlets reduced, among other measures. Parallel to its negotiations with creditors, NOMI will continue to seek investors interested in keeping the business alive. NOMI's management is also contem-plating an IPO on the Warsaw Stock Exchange to pro-vide its creditors with a convenient way of exiting the investment in the future.

Poland's key DIY chains Number of outlets as of end of 2012

0 10 20 30 40 50 60 70 80 90

Bricoman

Praktiker

NOMI

OBI

Leroy Merlin

Castorama*

Bricomarche

*) including Brico Depot Source: Cushman & Wakefield

Established in 1993, NOMI used to be part of the UK retail giant Kingfisher (owners of the Castorama chain), which sold the chain to private equity company Enterprise Investors in 2003 for PLN 45m. At the time, NOMI had 39 stores across the country and an-nual revenues of PLN 0.5bn. Over the 2007-2011 peri-od the business was profitable. In 2012 the company turned over PLN 497m and employed 1,367 staff. NOMI, which has stores in 28 medium-sized towns, belongs to a Polish investment fund i4ventures.

IT & TELECOM

Alinda buys broadcast Alinda buys broadcast Alinda buys broadcast Alinda buys broadcast infrastructure firm infrastructure firm infrastructure firm infrastructure firm Emitel from Montagu Emitel from Montagu Emitel from Montagu Emitel from Montagu

Two and a half years after it acquired Poland's leading television and radio broadcast infrastructure provider Emitel for EUR 425m, European private equity giant Montagu has sold the business for an undisclosed amount to Alinda Capital Partners, the American-based infrastructure investment firm. "Following the 2011 acquisition of Emitel together with the management we devised a five-year invest-ment plan focused on expansion and modernization of its broadcast infrastructure, better signal quality, digit-ization of terrestrial television and operational optimi-zation. However, we managed to achieve our invest-ment objectives in less than three years," says Michał Chałaczkiewicz, Director at Montagu Private Equity tells Poland Today. "The several hundred million PLN investment program that we implemented gave Emitel solid foundations for further growth." Emitel broadcasts television and radio signals nation-wide under long-term contracts with television and radio channels, including the government-owned TV and radio channels. The company is the sole broad-caster of digital terrestrial television signal in Poland, and is leading the introduction of digital radio. Poland completed the switchover to digital TV in mid-2013. With a proprietary network of 377 towers in Poland, Emitel is also actively developing its telecom infra-structure business, utilizing its tower locations for mobile network operators’ equipment.

weekly newsletter # 014 / 9th December 2013 / page 13

"The result of our investment program is a top quality transmission network covering the entire country, which has enabled Emitel to compete for digital ter-restrial television broadcasting contracts. Earlier this year Emitel also acquired two complementary busi-nesses extending its portfolio of broadcast and telecom towers. The company currently operates four digital multiplexes and successfully leads the migration from analogue television to a high quality digital terrestrial platform, which is the primary source of television for more than 30% of households in Poland," says Michał Chałaczkiewicz. Back in 2011, when Montagu bought Emitel from the French-owned telecoms group TPSA for a massive PLN 1.7bn (EUR 425m), the transaction raised many an eyebrow among market observers. Some of Monta-gu's competitors, which reportedly included France's TdF, as well as private equity funds EQT, Macquarie, Advent International, and Doughty Hanson, criticized the buyer for what they called an "irrationally high valuation" it put on Emitel. Everyone seemed to be in agreement, however, that Montagu paid extra for the potential it saw in the company. The deal was Monta-gu’s first direct investment in Poland, and its second investment in Central and Eastern Europe. Interna-tional financial institutions, focused on the CEE re-gion: Innova Capital, Value4Capital and the European Bank for Reconstruction and Development, co-invested alongside Montagu. "Our sale of Emitel marks the completion of another successful investment for Montagu. Today, Emitel is the market leader of television as well as radio trans-mission services in Poland. Following the digitaliza-tion process, the terrestrial television platform has be-come a viable and growing content distribution chan-nel. Moreover, the company is the only operator serv-ing all nationwide radio stations and is also Poland's largest operator of telecoms towers independent from mobile operators," says Michał Chałaczkiewicz.

Emitel's new owner, Alinda Capital Partners, is one of the world’s largest infrastructure investment firms. The company is wholly owned by its seven Partners and has USD 7.8bn in equity commitments to infra-structure investments. Alinda has invested in infra-structure businesses that operate in the United States as well as in Canada, the United Kingdom, Germany, the Netherlands, Austria, Belgium and Luxembourg. These businesses serve 100m customers annually in more than 400 cities globally, and employ more than 15,000 people. Alinda’s investors are predominantly pension funds for public sector and private sector workers. These institutions seek steady investments over the long term, matching their pension liabilities. They include some of the largest institutional inves-tors in the world.

As for Montagu, which has an estimated EUR 3.3bn worth of assets under management, it continues to seek new investment opportunities in Europe. The company invests in businesses that operate in stable markets across Europe with transaction values ranging from approximately EUR 100m to EUR 1bn.

"We are currently investing from our EUR 2.5bn Mon-tagu IV fund, focusing on sectors and companies with limited exposure to cyclical fluctuations, solid growth potential and an attractive operational profile. We do not specialize in any particular sectors. Our Warsaw team is working on a number of new investments but our policy is to refrain from commenting on ongoing projects. Following the sale of Emitel, our only in-vestment in the region is Euromedic International, Europe's largest provider of advanced diagnostic im-aging and cancer treatment services. The company op-erates in 15 countries, including 10 CEE markets. In Poland, one of Euromedic's key markets, we've recent-ly acquired Numedic, a chain of diagnostic centers," Michał Chałaczkiewicz tells Poland Today.

IT & TELECOM

Polish Asseco Group is Polish Asseco Group is Polish Asseco Group is Polish Asseco Group is Europe's 6th largest Europe's 6th largest Europe's 6th largest Europe's 6th largest software vendorsoftware vendorsoftware vendorsoftware vendor

After its revenues from proprietary software solutions had passed the EUR 1bn benchmark in 2012, Polish IT giant Asseco Group moved up in the ranking of Eu-rope's largest software producers, occupying the num-ber six position in the newly released 2013 edition of the prestigious Truffle 100 report. Asseco Group has remained one of Europe's top ten software vendors already for five consecutive years, during which time the company continued to boost sales of proprietary software, one of its key strategic goals. The upward trend is likely to continue also in 2013. In the first three quarters of the year, Asseco Group generated nearly PLN 4.2bn in sales revenues, achieving a 5% increase y/y. Operating profit reached PLN 483m, while net profit attributable to sharehold-ers of the parent company amounted to PLN 262 mil-lion. The backlog of orders totals PLN 5.5bnand is 5% higher than in the corresponding period of 2012. Rev-enues from Asseco's proprietary IT solutions also hit record-breaking levels. In the first nine months of 2013, they came to nearly PLN 3.3bn, an improvement of 7% y/y. During that period Asseco signed 3,326 new contracts, including large agreements with Orange Polska, social security institution ZUS and regional healthcare administration units. In Q3 2013, Asseco Poland acquired a 70% stake in Russian R-Style Softlab, which develops software for the banking and finance sector, specializing in online banking and customer service systems, data warehouses and business intelligence systems, as well

weekly newsletter # 014 / 9th December 2013 / page 14

as core banking systems. The acquisition expanded Asseco's customer pool by approximately 400 active clients. The Truffle 100 ranking discusses the marketplace of Europe’s one hundred major software producers, whose combined software revenues rose by 11% last year. Interestingly, 63% of that turnover was generat-ed by 10 largest market players, mainly Germany’s SAP with EUR 15.9 billion in software revenues, France’s Dassault Systèmes (EUR 1.8bn) and Britain’s Sage (EUR 1.6bn). The ranking is dominated by companies from the UK, France and Germany. Commenting on this year's ranking, Bernard Louis Roques, Partner & Co-Founder of Truffle Capital, emphasized that with 63,000 specialist jobs and high investments in devel-opment of new products, the software industry re-mains an unwavering catalyst for innovation and a key driver of European economic growth.

POLITICS & ECONOMY

Poland's lPoland's lPoland's lPoland's lower houseower houseower houseower house of parliament of parliament of parliament of parliament approvesapprovesapprovesapproves pension pension pension pension reform reform reform reform billbillbillbill

Polish lawmakers last week approved the takeover and cancellation of government bonds held by privately managed pension funds, allowing the cabinet to cut state debt and gain leeway for public spending. Law-makers in the 460-seat Sejm, the lower house of par-liament, voted 232-216 in favor of the changes, with one abstention. The draft law must still be approved by the Senate and signed by President Bronislaw Komorowski, who may direct it for legal review to Po-land's Constitutional Tribunal.

Under the new law, Poland's state-guaranteed private pension funds (OFE) are to transfer 51.5% of their as-sets to the state pension vehicle ZUS on 3rd February next year, after which they will be banned from invest-ing in treasury debt and state-guaranteed bonds start-ing 2016. The state pension institution will be also re-sponsible for distributing the pensions, and therefore the funds will also be required to gradually transfer employee assets to ZUS starting 10 years prior to re-tirement. According to the draft bill, the changes will lower Poland's public debt by 9.2 percentage points from its current level of 55% of GDP and reduce annu-al borrowing needs by PLN 20-25bnin the years 2014-2017. Pension funds in the mandatory system held PLN 303.4bn of assets, including PLN 131.1bn of stocks and PLN 125.8bn of bonds as of 31st October, data from Po-land’s financial markets regulator show. The owners of companies running the funds include Dutch Aegon and ING, German Allianz, US MetLife, British Aviva, French AXA, Italian Assicurazioni Generali, and Swedish Nordea Bank. What is more, participation in the OFE system has been made optional. While every OFE account re-mains in place with its rump equity assets, Poles will have four months to determine if the portion of their future social security premium - 2.9% - should contin-ue to go to the OFE funds. Should they fail to declare, their premiums go to a virtual individual account at the ZUS. They’ll be able to review their decision in 2016. For the past 14 years, Poland has had a hybrid pension system, with part of workers' contributions diverted from the state pay-as-you-go system to private pension funds, known collectively as the second pension pillar. Shortly after the new system was introduced, the gov-ernment found itself in a pickle, forced to finance pay-outs for pensioners covered by the old system at the

same time contributing to OFE accounts for would-be pensioners belonging to the new system. Poland ended up borrowing left and right and its debt skyrocketed as a result, from PLN 273bn in 1999 to PLN 888bn in mid-2013, with the pension system being responsible for roughly a half of the new liabilities. In the end, the government admitted the system was too costly for public finances and failed to deliver additional benefits for future pensioners.

The government-sponsored changes to the country’s three-tier pension system have sparked controversy, including concern that canceling bonds would amount to uncompensated expropriation. The overhaul is op-posed by 53% of Polish voters, according to a recent poll. The revamp may end up being vetted by the country’s constitutional court after president signs it into law. According to the President, the changes are "necessary for financial safety."

The government has already included the pension-fund changes in its 2014 budget, which will run a 4.6% of GDP surplus as a result of the asset transfer, accord-ing to a November forecast by the European Commis-sion.

weekly newsletter # 014 / 9th December 2013 / page 15

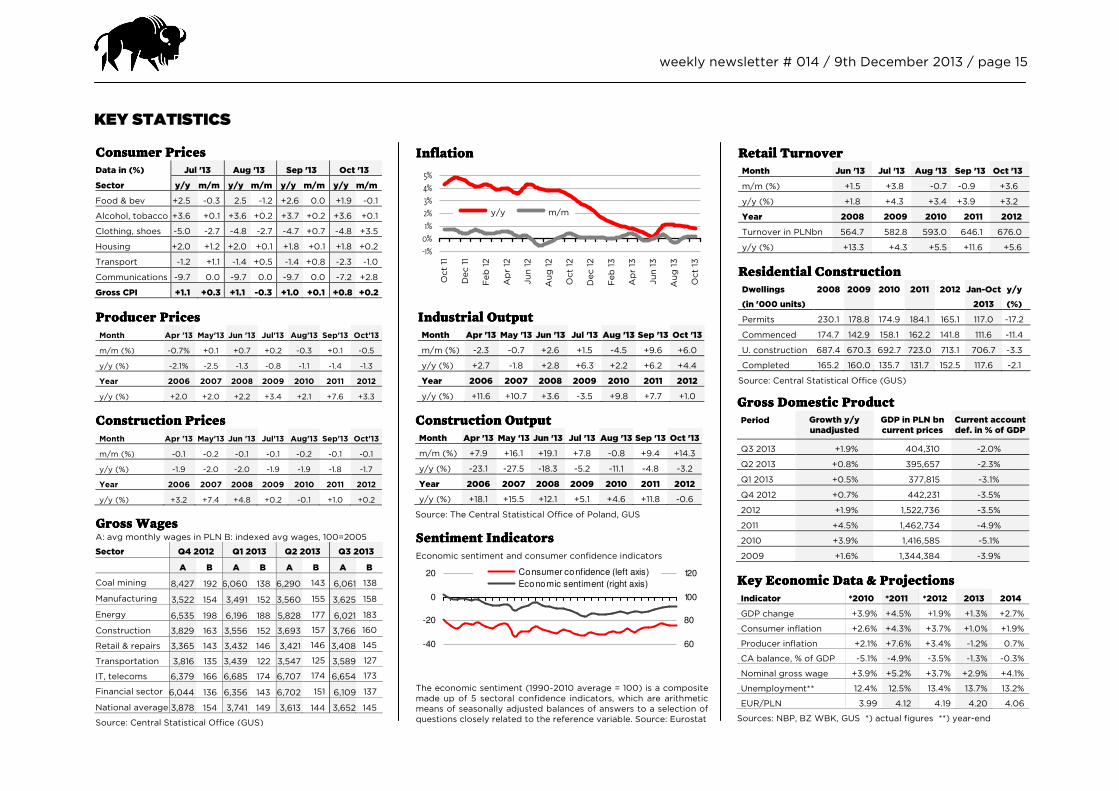

KEY STATISTICS

Consumer PriceConsumer PriceConsumer PriceConsumer Pricessss

Data in (%) Jul '13 Aug '13 Sep '13 Oct '13

Sector y/y m/m y/y m/m y/y m/m y/y m/m

Food & bev +2.5 -0.3 2.5 -1.2 +2.6 0.0 +1.9 -0.1

Alcohol, tobacco +3.6 +0.1 +3.6 +0.2 +3.7 +0.2 +3.6 +0.1

Clothing, shoes -5.0 -2.7 -4.8 -2.7 -4.7 +0.7 -4.8 +3.5

Housing +2.0 +1.2 +2.0 +0.1 +1.8 +0.1 +1.8 +0.2

Transport -1.2 +1.1 -1.4 +0.5 -1.4 +0.8 -2.3 -1.0

Communications -9.7 0.0 -9.7 0.0 -9.7 0.0 -7.2 +2.8

Gross CPI +1.1 +0.3 +1.1 -0.3 +1.0 +0.1 +0.8 +0.2

IIIInflationnflationnflationnflation

-1%

0%

1%

2%

3%

4%

5%

Oct 11

Dec 11

Feb 12

Apr 12

Jun 12

Aug 12

Oct 12

Dec 12

Feb 13

Apr 13

Jun 13

Aug 13

Oct 13

y/y m/m

Retail Retail Retail Retail TurnoverTurnoverTurnoverTurnover

Month Jun '13 Jul '13 Aug '13 Sep '13 Oct '13

m/m (%) +1.5 +3.8 -0.7 -0.9 +3.6

y/y (%) +1.8 +4.3 +3.4 +3.9 +3.2

Year 2008 2009 2010 2011 2012

Turnover in PLNbn 564.7 582.8 593.0 646.1 676.0

y/y (%) +13.3 +4.3 +5.5 +11.6 +5.6

Residential ConstructionResidential ConstructionResidential ConstructionResidential Construction

Dwellings

(in '000 units)

2008 2009 2010 2011 2012 Jan-Oct

2013

y/y

(%)

Permits 230.1 178.8 174.9 184.1 165.1 117.0 -17.2

Commenced 174.7 142.9 158.1 162.2 141.8 111.6 -11.4

U. construction 687.4 670.3 692.7 723.0 713.1 706.7 -3.3

Completed 165.2 160.0 135.7 131.7 152.5 117.6 -2.1

Source: Central Statistical Office (GUS)

GGGGross Domestic Productross Domestic Productross Domestic Productross Domestic Product

Period Growth y/y unadjusted

GDP in PLN bn current prices

Current account def. in % of GDP

Q3 2013 +1.9% 404,310 -2.0%

Q2 2013 +0.8% 395,657 -2.3%

Q1 2013 +0.5% 377,815 -3.1%

Q4 2012 +0.7% 442,231 -3.5%

2012 +1.9% 1,522,736 -3.5%

2011 +4.5% 1,462,734 -4.9%

2010 +3.9% 1,416,585 -5.1%

2009 +1.6% 1,344,384 -3.9%

Key Economic Data & ProjectionsKey Economic Data & ProjectionsKey Economic Data & ProjectionsKey Economic Data & Projections

Indicator *2010 *2011 *2012 2013 2014

GDP change +3.9% +4.5% +1.9% +1.3% +2.7%

Consumer inflation +2.6% +4.3% +3.7% +1.0% +1.9%

Producer inflation +2.1% +7.6% +3.4% -1.2% 0.7%

CA balance, % of GDP -5.1% -4.9% -3.5% -1.3% -0.3%

Nominal gross wage +3.9% +5.2% +3.7% +2.9% +4.1%

Unemployment** 12.4% 12.5% 13.4% 13.7% 13.2%

EUR/PLN 3.99 4.12 4.19 4.20 4.06

Sources: NBP, BZ WBK, GUS *) actual figures **) year-end

Gross WagesGross WagesGross WagesGross Wages A: avg monthly wages in PLN B: indexed avg wages, 100=2005

Sector Q4 2012 Q1 2013 Q2 2013 Q3 2013

A B A B A B A B

Coal mining 8,427 192 6,060 138 6,290 143 6,061 138

Manufacturing 3,522 154 3,491 152 3,560 155 3,625 158

Energy 6,535 198 6,196 188 5,828 177 6,021 183

Construction 3,829 163 3,556 152 3,693 157 3,766 160

Retail & repairs 3,365 143 3,432 146 3,421 146 3,408 145

Transportation 3,816 135 3,439 122 3,547 125 3,589 127

IT, telecoms 6,379 166 6,685 174 6,707 174 6,654 173

Financial sector 6,044 136 6,356 143 6,702 151 6,109 137

National average 3,878 154 3,741 149 3,613 144 3,652 145

Source: Central Statistical Office (GUS)

Construction OutputConstruction OutputConstruction OutputConstruction Output

Month Apr '13 May '13 Jun '13 Jul '13 Aug '13 Sep '13 Oct '13

m/m (%) +7.9 +16.1 +19.1 +7.8 -0.8 +9.4 +14.3

y/y (%) -23.1 -27.5 -18.3 -5.2 -11.1 -4.8 -3.2

Year 2006 2007 2008 2009 2010 2011 2012

y/y (%) +18.1 +15.5 +12.1 +5.1 +4.6 +11.8 -0.6

Source: The Central Statistical Office of Poland, GUS

Sentiment IndicatorsSentiment IndicatorsSentiment IndicatorsSentiment Indicators

Economic sentiment and consumer confidence indicators

-40

-20

0

20

60

80

100

120 Consumer confidence (left axis)

Economic sentiment (right axis)

The economic sentiment (1990-2010 average = 100) is a composite made up of 5 sectoral confidence indicators, which are arithmetic means of seasonally adjusted balances of answers to a selection of questions closely related to the reference variable. Source: Eurostat

Producer PriceProducer PriceProducer PriceProducer Pricessss

Month Apr '13 May'13 Jun '13 Jul'13 Aug'13 Sep'13 Oct'13

m/m (%) -0.7% +0.1 +0.7 +0.2 -0.3 +0.1 -0.5

y/y (%) -2.1% -2.5 -1.3 -0.8 -1.1 -1.4 -1.3

Year 2006 2007 2008 2009 2010 2011 2012

y/y (%) +2.0 +2.0 +2.2 +3.4 +2.1 +7.6 +3.3

Construction PriceConstruction PriceConstruction PriceConstruction Pricessss

Month Apr '13 May'13 Jun '13 Jul'13 Aug'13 Sep'13 Oct'13

m/m (%) -0.1 -0.2 -0.1 -0.1 -0.2 -0.1 -0.1

y/y (%) -1.9 -2.0 -2.0 -1.9 -1.9 -1.8 -1.7

Year 2006 2007 2008 2009 2010 2011 2012

y/y (%) +3.2 +7.4 +4.8 +0.2 -0.1 +1.0 +0.2

IIIIndustrial Outputndustrial Outputndustrial Outputndustrial Output

Month Apr '13 May '13 Jun '13 Jul '13 Aug '13 Sep '13 Oct '13

m/m (%) -2.3 -0.7 +2.6 +1.5 -4.5 +9.6 +6.0

y/y (%) +2.7 -1.8 +2.8 +6.3 +2.2 +6.2 +4.4

Year 2006 2007 2008 2009 2010 2011 2012

y/y (%) +11.6 +10.7 +3.6 -3.5 +9.8 +7.7 +1.0

weekly newsletter # 014 / 9th December 2013 / page 16

TTTTraderaderaderade

Poland exports and imports according to commodity groups, according to SITC classification

EXPORTS in PLN bn IMPORTS in PLN bn

Jan-Sep 2013

y/y (%)

share (%)

2012 share (%)

Jan-Sep 2013

y/y (%)

share (%)

2012 share (%)

Food and live animals 49,806 +9.4 10.6 61,694 10.3 34,538 +4.5 7.3 44,287 6.9

Beverages and tobacco 6,405 +6.7 1.4 7,967 1.3 2,995 +1.2 0.6 3,989 0.6

Crude materials except fuels 11,947 +9.9 2.5 14,024 2.4 15,917 -7.4 3.4 22,053 3.5

Fuels etc 22,200 +0.7 4.7 29,389 4.9 55,502 -11.7 11.6 85,280 13.4

Animal and vegetable oils 1,267 +46.7 0.3 1,342 0.2 1,955 -9.4 0.4 2,887 0.5

Chemical products 43,903 +7.0 9.3 54,295 9.1 69,490 +1.9 14.6 89,140 14.0

Manufactured goods by material 97,528 +1.0 20.7 126,161 21.1 82,985 -3.2 17.5 110,773 17.4

Machinery, transport equip. 176,544 +5.0 37.5 223,646 37.5 156,992 +2.4 33.1 203,718 31.9

Other manufactured articles 60,447 +6.0 12.8 75,925 12.7 42,337 -4.8 8.9 57,646 9.0

Not classified 1,257 n/a 0.2 2,653 0.5 12,229 n/a 2.6 18,515 2.8

TOTAL 471,304 +4.8 100 597,096 100 474,940 -1.8 100 638,288 100

Poland's ten largest trading partners, ranked according to 2012

EXPORTS in PLNbn IMPORTS in PLN bn

No Country Jan- Sep 2013

share *2012 Share No Country Jan- Sep 2013

share *2012 Share

1 Germany 118,119 25.1% 150,046 25.1% 1 Germany 101,785 21.4% 134,933 21.1%

2 UK 30,740 6.5% 40,184 6.7% 2 Russia 59,388 12.5% 91,033 14.3%

3 Czech Rep. 28,868 6.1% 37,475 6.3% 3 China 44,332 9.3% 57,235 9.0%

4 France 26,520 5.6% 34,862 5.8% 4 Italy 24,315 5.1% 32,782 5.1%

5 Russia 25,476 5.4% 32,290 5.4% 5 France 18,262 3.8% 25,303 4.0%

6 Italy 20,214 4.3% 29,067 4.9% 6 Netherlands 17,848 3.8% 24,543 3.8%

7 Netherlands 18,714 4.0% 26,678 4.5% 7 Czech Rep. 17,304 3.6% 23,327 3.7%

8 Ukraine 13,277 2.8% 17,213 2.9% 8 USA 13,299 2.8% 16,436 2.6%

9 Sweden 12,777 2.7% 15,811 2.6% 9 UK 12,704 2.7% 15,509 2.4%

10 Slovakia 12,273 2.6% 15,288 2.6% 10 South Korea n/a n/a 14,619 2.3%

Source: Central Statistical Office (GUS) *) preliminary estimates, full year

CurrencyCurrencyCurrencyCurrency

Central Bank average rates

as of 6 December 2013

100 USD 306.73 ↓

100 EUR 419.25 ↓

100 GBP 501.68 ↓

100 CHF 342.38 ↑

100 DKK 56.20 ↓

100 SEK 47.13 ↑

100 NOK 49.79 ↓

10,000 JPY 300.21 ↓

100 CZK 15.26 ↓

10,000 HUF 138.70 ↓

100 USD/EUR against PLN

300

350

400

450

21 Dec 12

4 M

ar 13

14 M

ay 13

22 Jul 13

27 Sep 13

6 D

ec 13

USD EUR

MMMMoney Supplyoney Supplyoney Supplyoney Supply

in PLN m Jul '13 Aug '13 Sep '13 Oct '13

Monetary base 155,767 153,867 166,620 154,967

M1 530,666 531,124 540,873 536,237

- Currency outside banks 112,565 114,083 113,223 113,174

M2 921,662 928,359 931,042 935,095

- Time deposits 405,900 412,407 405,703 414,941

M3 945,077 949,988 947,228 955,419

- Net foreign assets 159,749 154,035 147,978 150,517 Monetary base: Polish currency emitted by the central bank and money on accounts held with it. M1= currency outside banks + demand deposits M2= M1+ time deposits (inc in foreign currencies) M3= the broad measure of money supply Source: NBP

CCCCreditreditreditredit

The financial sector's net lending in PLN bn,

loan stock at the end of period

Type of loan Jul '13 Aug '13 Sep '13 Oct '13

Loans to customers 896,635 901,863 908,106 901,288

- to private companies 261,000 263,491 262,963 559,965

- to households 552,503 556,027 560,608 260,585

Total assets of banks 1,616,221 1,627,182 1,626,489 1,612,836

Source: Central Bank NBP

IIIInterest ratesnterest ratesnterest ratesnterest rates

Average weighted annual interest rates

on loans to non-financial corporations

Term / currency May '13 Jun '13 Jul '13 Aug '13 Sep '13 Oct '13

PLN (up to 1 year) 5.3% 5.0% 4.7% 4.6% 4.5% 4.5%

PLN (up to 5 y ) 5.7% 5.4% 5.1% 5.1% 4.9% 4.9%

PLN (over 5 y) 5.6% 5.3% 4.9% 4.9% 4.8% 4.8%

PLN (total) 5.6% 5.3% 5.0% 4.9% 4.8% 4.8%

EUR (up to 1m EUR) 2.3% 1.9% 2.3% 1.9% 1.8% 2.0%

EUR (over 1m EUR) 3.2% 2.9% 3.5% 3.5% 3.2% 2.5%

Warsaw Inter Bank Offered Rate (WIBOR) as of 6 Dec 2013

Overnight 1 week 1 month 3 months 6 months

2.58%% 2.58% 2.60% 2.65% 2.70%

Central Bank (NBP) Base Rates

Reference Lombard NBP deposit Rediscount

2.50% 4.00% 1.00% 2.75%

Stock ExchangeStock ExchangeStock ExchangeStock Exchange

Warsaw Stock Exchange, rates in PLN

WIG-20 stocks in alphabetical

order

Price 6 Dec '13

Change 29 Nov

'13

Change end of '12

↓ Asseco Pol. 49.67 -3% +10%

↓ Bogdanka 135.65 -2% 0%

↓ BZ WBK 391 -4% +62%

↓ Eurocash 46.95 -7% +7%

↓ Grupa Lotos 37.36 -6% -9%

↓ GTC 8.34 -1% -16%

↓ Handlowy 115.35 -4% +17%

↓ JSW 62.3 -6% -33%

↓ Kernel 40 -6% -40%

↓ KGHM 112.8 -5% -41%

↓ mBank 513.45 -8% +58%

↓ Pekao 183.15 -3% +9%

↓ PGE 17.37 -7% -5%

↓ PGNiG 5.65 -2% +8%

↓ PKN Orlen 45.42 -5% -8%

↓ PKO BP 39.7 -4% +8%

↓ PZU 453.85 -3% +4%

↓ Synthos 5.2 -4% -4%

↓ Tauron 4.84 -6% +2%

↓ TP SA 10.15 -2% -17%

Source: Warsaw Stock Exchange

Key indices

as of 6 December 2013

WIG Total index

55552222,,,,777727272727....52525252 Change 1 week -4% ↓

Change end of '12 +11% ↑

WIG-20 blue chip index

2,2,2,2,479479479479....16161616 Change 1 week -4% ↓

Change end of '12 -4% ↓

WIG Total closing index

last three months

45000

47500

50000

52500

55000

57500

5 Sep 13

27 Sep 13

21 Oct 13

14 N

ov 13

6 D

ec 13

weekly newsletter # 014 / 9th December 2013 / page 17

Poland Today Sp. z o. o.

ul. Złota 61 lok. 100,

00–819 Warsaw, Poland

tel/fax: +48 22 464 82 69

mobile: +48 694 922 898,

+48 602 214 603

www.poland-today.pl

Business Review+ Editor

Lech Kaczanowski

office: +48 22 412 41 69

mobile: +48 607 079 547

Business Review+ Subscription

1 year- EUR 690 (PLN 2760)

6 months- EUR 375 (PLN 1480)

3 months- EUR 245 (PLN 980)

Sales Director

James Anderson-Hanney

mobile: +48 881 650 600

james.anderson-hanney@poland-

today.pl

Publisher Richard Stephens

Financial Director Arkadiusz Jamski

Creative Director Bartosz Stefaniak

New Business Consultant

Tomasz Andryszczyk

RRRRegional Dataegional Dataegional Dataegional Data

Poland's regions

(main cities indicated

in brackets)

Industrial output

Jan-Oct 2013 *

Monthly wages (PLN)

Jan-Oct 2013 **

Unemploy-ment

Oct 2013

New dwellings Jan-Oct 2013

Indus-

try

Constru-

ction

Indus-

try

Constru-

ction

in '000 % Num-

ber

Index *

Dolnośląskie (Wrocław) 99.5 92.0 4,188 4,033 148.0 12.8 13,709 115.7

Kujawsko-Pomorskie (Bydgoszcz) 102.1 105.9 3,323 3,263 143.1 17.4 5,085 103.9

Lubelskie (Lublin) 102.1 98.7 3,637 3,054 126.1 13.7 5,243 90.8

Lubuskie (Zielona Góra) 96.4 88.3 3,367 2,980 57.0 15.1 2,715 104.7

Łódzkie (Łódź) 104.0 89.6 3,617 3,035 146.9 13.7 5,153 87.9

Małopolskie (Kraków) 96.8 98.7 3,749 3,339 158.6 11.2 12,239 106.2

Mazowieckie (Warszawa) 107.4 77.0 4,458 4,778 278.4 10.9 23,987 95.0

Opolskie (Opole) 97.3 98.3 3,478 3,178 49.7 13.8 1,455 106.3

Podkarpackie (Rzeszów) 108.4 97.8 3,248 3,047 145.7 15.6 4,904 97.1

Podlaskie (Białystok) 105.9 98.7 3,194 3,758 67.9 14.5 3,134 87.3

Pomorskie (Gdańsk-Gdynia) 102.1 92.7 3,881 3,488 110.6 12.9 9,893 91.7

Śląskie (Katowice) 97.6 89.4 4,480 3,535 203.9 11.0 8,809 111.6

Świętokrzyskie (Kielce) 101.3 88.3 3,360 3,185 85.7 15.8 2,180 93.3

Warmińsko-Mazurskie (Olsztyn) 98.8 83.1 3,172 3,084 108.9 20.6 3,324 81.0

Wielkopolskie (Poznań) 104.7 90.9 3,644 3,603 140.7 9.3 11,252 96.1

Zachodniopomorskie (Szczecin) 111.1 86.0 3,416 3,292 104.0 17.0 4,565 80.7

National average 101.7 87.6 3,885 3,697 2,075.2 13.0 117,647 97.9

Index 100 = same period of the previous year. ** without social taxes

Sources: Central Statistical Office GUS, NBP, C&W

Foreign Direct Investment (EUR m)Foreign Direct Investment (EUR m)Foreign Direct Investment (EUR m)Foreign Direct Investment (EUR m)

Quarter Q1'12 Q2 '12 Q3 '12 Q4 '12 Q1 '13 Q2 '13