Pak Policy 1

19

July 2009 Document of the World Bank Report No. 50078-PK Pakistan Tax Policy Report T apping T ax Bases for Development (In T wo Volumes) V olume I: Summary Repor t The World Bank The Government of Pa kistan Federal Board of Revenue Georgia State University P u b l i c D i s c l o s u r e A u t h o r i z e d P u b l i c D i s c l o s u r e A u t h o r i z e d P u b l i c D i s c l o s u r e A u t h o r i z e d P u b l i c D i s c l o s u r e A u t h o r i z e d

-

Upload

sunnivoice -

Category

Documents

-

view

222 -

download

0

Transcript of Pak Policy 1

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 1/19

July 2009

Document of the World Bank

Report No. 50078-PK

PakistanTax Policy ReportTapping Tax Bases for Development(In Two Volumes) Volume I: Summary Report

The World Bank The Government of Pakistan Federal Board of Revenue Georgia State University

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 2/19

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 3/19

ACK OWLEDGEME TS

This report is a joint product of a team from the Federal Board of Revenue (FBR), Government of Pakistan, theAndrew Young School of Public Policy (AYSPS) at the Georgia State University, and the World Bank. The views,expressed in the report, are of the authors and not of the Government of Pakistan.

The FBR team was headed by Mr. Ahmad Waqar, Secretary Revenue Division and Chairman FBR, and Mr. M.Abdullah Yusuf, former Chairman FBR, and included Mr. Mumtaz Haider Rizvi, Member Fiscal Research andStatistics, Dr. Ather Maqsood Ahmed, former Member Fiscal Research and Statistics, Mrs. Robina Ather Ahmed,Chief Fiscal Research and Statistics, Mr. Umar Wahid, Secretary Fiscal Research and Statistics, Mr. Mir AhmedKhan, Second Secretary Fiscal Research and Statistics, and Mr. Naeem Ahmed, Second Secretary Fiscal Researchand Statistics.

The report was prepared by Kaspar Richter (World Bank), and Jorge Martinez-Vazquez (AYSPS). It is based onseven background studies (listed below), drafted by Robina Ather Ahmed, James Alm, Roy Bahl, Musharraf Cyan,Mir Ahmad Khan, Jorge Martinez-Vazquez, Geerten Michelse, Mark Rider, Wayne Thirsk, Umar Wahid and SallyWallace. The tax revenue simulation results in the report are based on micro-simulation models developed by Mark Rider and Sally Wallace with Harini Kannan. The GST chapter draws extensively on a review of Pakistan’s salestax by Rebecca Millar and Christophe Waerzeggers from June 2008. The report also benefited from the Pakistantax administration review by Carlos Silvani, Edmund Biber, William Crandall, Wyatt Grant, Orlando Reos andGeoff Seymour from September 2008. Peer reviewer comments from Kai-Alexander Kaiser, Senior Economist,World Bank; Michael Keen, Advisor, International Monetary Fund; Dr. Ahmad Khan, former Member FBR;Russell Krelove, Senior Economist, International Monetary Fund, and Eduardo Ley, Lead Economist, World Bank greatly enhanced the quality of the report. Dr. Ahmad Khan and Dr. A. R. Kemal reviewed the background studies,and Ehtisham Ahmad commented on the concept paper. Anjum Ahmad, Shamsuddin Admad, Mihaly Kopanyi,Hanid Mukhtar, and Saadia Refaqat from the World Bank provided useful feedback. Mirafe Marcos helped greatlyby providing the draft chapter of the provincial background study. The team would like to thank Satu Kahkonen,Lead Economist, Miria Pigato, Sector Manager, Ijaz Nabi, former Sector Manager, Yusupha Crookes, CountryDirector, and Ernesto May, Sector Director, for continued support and guidance throughout all stages of this report.Muhammad Shafiq, Nimanthi Attapattu, and Irum Touqeer handled with great ease all arrangements for themissions and for the processing of the report.

The team benefited enormously from the close collaboration of the Government of Pakistan ever since this work was launched in January 2007. The team is very grateful to Mr. M. Abdullah Yusuf, who conceived the idea forthis report, and to Dr. Ather Maqsood Ahmed, who developed the framework and coordinated the inputs of theFBR team. The team is greatly indebted for the outstanding support and assistance of FBR’s Fiscal Research andStatistics Wing. Its contribution is immense: it co-authored three background studies; provided comments,feedback, and guidance to the team throughout the analysis and report preparation; and facilitated the interactionwith other departments, including the Budget Wing, Debt Office, and the Economic Affairs Division of theMinistry of Finance.

Background Papers for the Pakistan Tax Policy Report

1. Ahmed, Robina Ather and Rider, Mark. Pakistan’s Tax Gap: Estimates by Tax Calculation and Methodology .2. Alm, James and Khan, Mir Ahmad. Assessing Enterprise Taxation and the Investment Climate in Pakistan .

3. Bahl, Roy, Wallace, Sally and Cyan, Musharraf. Pakistan: Provincial Government Taxation .

4. Martinez-Vazquez, Jorge. Pakistan – A Preliminary Assessment of the Federal Tax System.

5. Michelse, Geerten. Pakistan – a Globalized Tax World – An Analysis of its International Tax Practice.

6. Thirsk, Wayne. Tax Policy in Pakistan: An Assessment of Major Taxes and Options for Reform.

7. Wahid, Umar and Wallace, Sally. Incidence of Taxes in Pakistan: Primer and Estimates

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 4/19

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 5/19

i

EXECUTIVE SUMMARY

Preface

One of the toughest questions that the Pakistangovernment faces is what to do about taxes and howto raise tax revenues. There can be no real progress

on education, health care, infrastructure or any majoreconomic issue without dealing with rising budgetdeficits and mounting debt. To restore the health of the budget, let alone keep pledges for spending moremoney on social safety nets and development, thegovernment will have to raise tax revenues. AsPakistan’s economy recovers from its presenteconomic crisis, the overall tax effort has to bevisibly enhanced. The effort must be fair, efficientand supportive of sustained economic growth.

Tax revenue has continued to be a problem for thePakistan government. In the past, tax payers haveused anything from simple to sometimes complexschemes to keep businesses and households outsidethe tax authority’s reach. In response, the taxadministration has looked for short term solutionsand put together makeshift arrangements to save theday. There were new withholding taxes, tax rateincreases, revisions of targets and the like. Attemptsto remove special treatments and exemptions wentagainst powerful lobby groups and did not usuallysucceed. Whereas, all this improvisation may nothave resulted in buoyant tax revenue collection, itallowed the government to muddle through – untilthe arrival of the next crisis.

There is broad consensus that Pakistan’s tax systemunderperforms, as its tax base is very narrow. Thegovernment taxes only a limited number of sectors,businesses and people. The low level and largevolatility of these tax revenues has greatlyconstrained the government’s ability to make plansfor development and poverty reduction, and respondadequately to sudden economic crises. Theseweaknesses are so grave that they can undermine theconfidence in Pakistan’s economy as a whole.

The appropriate response to these challenges is toembrace a structural reform of the tax system. Thegoal is to put in place a system that is simple andpredictable, encourages investment and rewardspeople for their hard work. At the same time, itdelivers the funds for development spending. Such acomprehensive overhaul of the tax system is a crucialstep for securing Pakistan’s sustainable development.

The Pakistan government has now taken on board thechallenge of stepping up revenue mobilization. The2009 Poverty Reduction Strategy Paper (PRSP) laysout the objective of increasing the tax-to-GDP (GrossDomestic Product) ratio by 3.2 percentage points of GDP over the next five years, lifting the tax-to-GDPratio from 10.4 percent of GDP in 2007-08 to 13.9percent of GDP in 2012-13. This is encouraging, asin the past, similar targets were far more modest. Forexample, the 2003 PRSP envisioned an increase inthe tax-to-GDP ratio of only 1 percentage point of GDP in five years.

Yet, it is by no means certain that fundamental taxreform will succeed. Previous attempts at setting thesystem right over the last decades have deliveredlittle in terms of more revenues and a more rational

tax system. Comprehensive and fair tax reform willface stiff opposition, as it has done in the past. Whilethe tax system has been bad for the country, it hasbeen good for those who were able to receive highincomes largely shielded from the tax man. Theseinterest groups will not want wider tax nets and moreeffective enforcement because their narrowerinterests will supersede the broader ones of astabilized and growing economy.

This is why, it is feared that when the fiscal pressurewill start to ease, the tax reform pushback will be infull swing. Even modest reform proposals to curb taxexemptions and tax evasion will come under fire, andthe government will be subjected to pressure to back down and to return to business as usual. This wouldleave the government with far too little revenue tocover its desired expenses. The result would beunsustainable budget deficits or, alternatively, deepcuts in spending. which in turn would make itimpossible to maintain social and infrastructurespending at a level that is required for development.Yet, the special-treatment lobbyists have little to sayabout how the government should close the budgetgap their tax cuts would produce; the talk aboutfighting government waste and reformingprocurement procedures, however important, doesnot add up to the required sums.

This report highlights design ingredients for acomprehensive reform of tax policy in Pakistan. Inthe final analysis, the success of tax reform willdepend less on the mechanism of taxation and moreon the politics of taxation. Beyond adequateadministrative resources and an implementation

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 6/19

ii

strategy, this will require a clear political recognitionof the importance of the task and the willingness topersist with tax reform over the long haul.

Tapping Tax Bases for Development

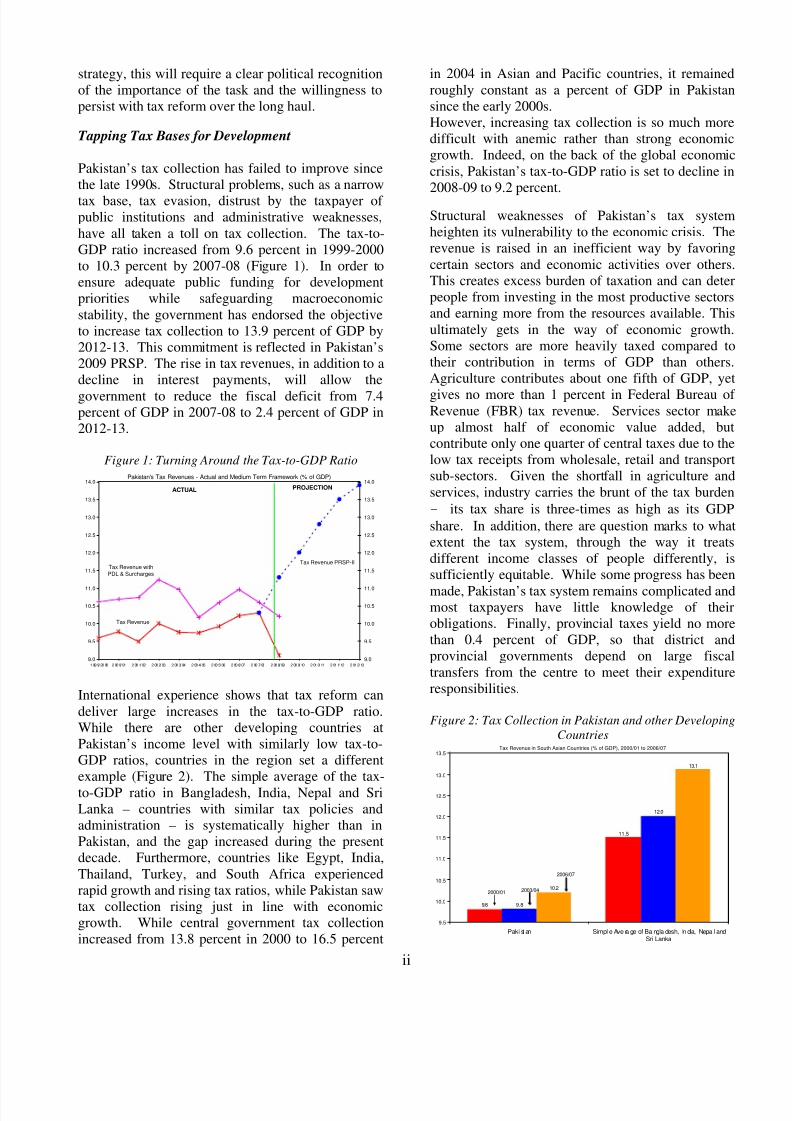

Pakistan’s tax collection has failed to improve sincethe late 1990s. Structural problems, such as a narrowtax base, tax evasion, distrust by the taxpayer of public institutions and administrative weaknesses,have all taken a toll on tax collection. The tax-to-GDP ratio increased from 9.6 percent in 1999-2000to 10.3 percent by 2007-08 (Figure 1). In order toensure adequate public funding for developmentpriorities while safeguarding macroeconomicstability, the government has endorsed the objectiveto increase tax collection to 13.9 percent of GDP by2012-13. This commitment is reflected in Pakistan’s2009 PRSP. The rise in tax revenues, in addition to adecline in interest payments, will allow thegovernment to reduce the fiscal deficit from 7.4percent of GDP in 2007-08 to 2.4 percent of GDP in2012-13.

Figure 1: Turning Around the Tax-to-GDP Ratio Pakistan's Tax Revenues - Actual and Medium Term Framework (% of GDP)

Tax Revenue withPDL & Surcharges

Tax Revenue

Tax Revenue PRSP-II

9.0

9.5

10.0

10.5

11.0

11.5

12.0

12.5

13.0

13.5

14.0

1 99 9/ 20 00 2 00 0/ 01 2 00 1/ 02 2 00 2/ 03 2 00 3/ 04 2 00 4/ 05 2 00 5/ 06 2 00 6/ 07 2 00 7/ 08 2 00 8/ 09 2 00 9/ 10 2 01 0/ 11 2 01 1/ 12 2 01 2/ 139.0

9.5

10.0

10.5

11.0

11.5

12.0

12.5

13.0

13.5

14.0PROJECTIONACTUAL

International experience shows that tax reform candeliver large increases in the tax-to-GDP ratio.While there are other developing countries atPakistan’s income level with similarly low tax-to-GDP ratios, countries in the region set a differentexample (Figure 2). The simple average of the tax-to-GDP ratio in Bangladesh, India, Nepal and SriLanka – countries with similar tax policies andadministration – is systematically higher than inPakistan, and the gap increased during the presentdecade. Furthermore, countries like Egypt, India,Thailand, Turkey, and South Africa experiencedrapid growth and rising tax ratios, while Pakistan sawtax collection rising just in line with economicgrowth. While central government tax collectionincreased from 13.8 percent in 2000 to 16.5 percent

in 2004 in Asian and Pacific countries, it remainedroughly constant as a percent of GDP in Pakistansince the early 2000s.However, increasing tax collection is so much moredifficult with anemic rather than strong economicgrowth. Indeed, on the back of the global economiccrisis, Pakistan’s tax-to-GDP ratio is set to decline in2008-09 to 9.2 percent.

Structural weaknesses of Pakistan’s tax systemheighten its vulnerability to the economic crisis. Therevenue is raised in an inefficient way by favoringcertain sectors and economic activities over others.This creates excess burden of taxation and can deterpeople from investing in the most productive sectorsand earning more from the resources available. Thisultimately gets in the way of economic growth.Some sectors are more heavily taxed compared totheir contribution in terms of GDP than others.Agriculture contributes about one fifth of GDP, yetgives no more than 1 percent in Federal Bureau of Revenue (FBR) tax revenue. Services sector makeup almost half of economic value added, butcontribute only one quarter of central taxes due to thelow tax receipts from wholesale, retail and transportsub-sectors. Given the shortfall in agriculture andservices, industry carries the brunt of the tax burden– its tax share is three-times as high as its GDPshare. In addition, there are question marks to whatextent the tax system, through the way it treatsdifferent income classes of people differently, issufficiently equitable. While some progress has beenmade, Pakistan’s tax system remains complicated andmost taxpayers have little knowledge of theirobligations. Finally, provincial taxes yield no morethan 0.4 percent of GDP, so that district andprovincial governments depend on large fiscaltransfers from the centre to meet their expenditureresponsibilities.

Figure 2: Tax Collection in Pakistan and other DevelopingCountries

Tax Revenue in South Asian Countries (% of GDP), 2000/01 to 2006/07

9.8

11.5

9.8

12.0

10.2

13.1

9.5

10.0

10.5

11.0

11.5

12.0

12.5

13.0

13.5

Paki st an Simpl e Ave ra ge of Ba ngla desh, In dia, Nepa l andSri Lanka

2000/01 2003/04

2006/07

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 7/19

iii

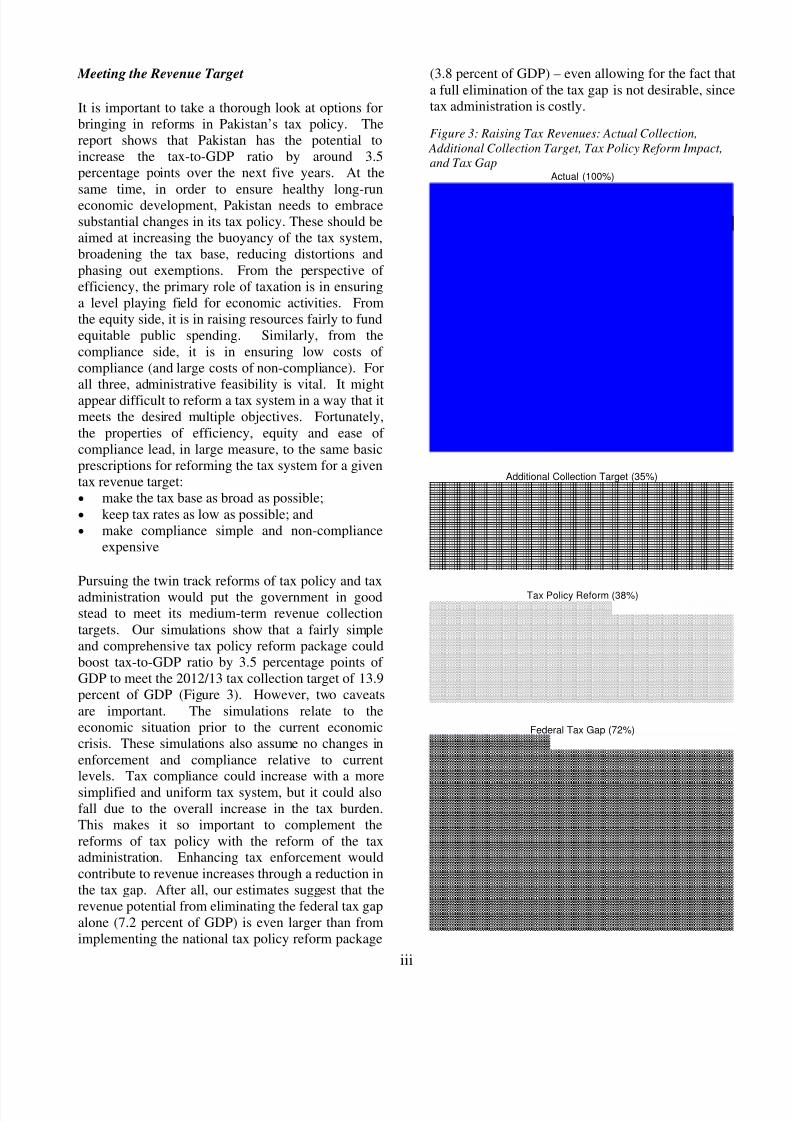

Meeting the Revenue Target

It is important to take a thorough look at options forbringing in reforms in Pakistan’s tax policy. Thereport shows that Pakistan has the potential toincrease the tax-to-GDP ratio by around 3.5percentage points over the next five years. At the

same time, in order to ensure healthy long-runeconomic development, Pakistan needs to embracesubstantial changes in its tax policy. These should beaimed at increasing the buoyancy of the tax system,broadening the tax base, reducing distortions andphasing out exemptions. From the perspective of efficiency, the primary role of taxation is in ensuringa level playing field for economic activities. Fromthe equity side, it is in raising resources fairly to fundequitable public spending. Similarly, from thecompliance side, it is in ensuring low costs of compliance (and large costs of non-compliance). Forall three, administrative feasibility is vital. It mightappear difficult to reform a tax system in a way that itmeets the desired multiple objectives. Fortunately,the properties of efficiency, equity and ease of compliance lead, in large measure, to the same basicprescriptions for reforming the tax system for a giventax revenue target:• make the tax base as broad as possible;• keep tax rates as low as possible; and• make compliance simple and non-compliance

expensive

Pursuing the twin track reforms of tax policy and taxadministration would put the government in goodstead to meet its medium-term revenue collectiontargets. Our simulations show that a fairly simpleand comprehensive tax policy reform package couldboost tax-to-GDP ratio by 3.5 percentage points of GDP to meet the 2012/13 tax collection target of 13.9percent of GDP (Figure 3). However, two caveatsare important. The simulations relate to theeconomic situation prior to the current economiccrisis. These simulations also assume no changes inenforcement and compliance relative to currentlevels. Tax compliance could increase with a moresimplified and uniform tax system, but it could alsofall due to the overall increase in the tax burden.This makes it so important to complement thereforms of tax policy with the reform of the taxadministration. Enhancing tax enforcement wouldcontribute to revenue increases through a reduction inthe tax gap. After all, our estimates suggest that therevenue potential from eliminating the federal tax gapalone (7.2 percent of GDP) is even larger than fromimplementing the national tax policy reform package

(3.8 percent of GDP) – even allowing for the fact thata full elimination of the tax gap is not desirable, sincetax administration is costly.

Figure 3: Raising Tax Revenues: Actual Collection, Additional Collection Target, Tax Policy Reform Impact,and Tax Gap

Actual (100%)

Additional Collection Target (35%)

Tax Policy Reform (38%)

Federal Tax Gap (72%)

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 8/19

iv

Closing the Tax Gap

The tax gap provides a useful measure of the extentof tax evasion in a country. People and firms fail tocomply with tax laws for many reasons, such asillness, distractions, ignorance, sloth and greed.There is a difference between tax avoidance and taxevasion. Tax avoidance refers to the use of the taxlaw to minimize tax liabilities, which is perfectlylegal. Tax evasion, or non-compliance with the taxlaw, refers to the non-payment of lawful tax liabilitiesand is illegal. The tax gap does not arise from taxavoidance, but rather from evasion, whatever theunderlying motivation. Given this definition, the taxgap becomes zero when everyone fully complies witha country’s tax system. As tax evasion increases, thecountry’s tax gap increases. Thus, the size of acountry’s tax gap is directly related to the extent of tax evasion in the country. A large tax gap suggeststhat a tax system is likely to underperform in terms of

revenues, efficiency, equity and tax administration.As mentioned earlier, the estimated federal tax gap inPakistan for 2007-08 is about 79 percent of actual taxreceipts. This sum amounts to over Rs. 796 billion,or some Rs. 4,800 worth of tax evasion by everyman, woman and child in Pakistan.

What measures can the government take to reducethe tax gap? International evidence suggests that taxevasion depends crucially on enforcement strategies.It is a fair guess that the FBR is disliked by manyPakistani businessmen, professionals and workers.

But many people who dislike the FBR probably do sofor the wrong reasons. They may think it is a harshand cruel agency, but in fact it is not nearly asvigilant as it should be. At least, this is an importantlesson from the US Internal Revenue Service’s (IRS)National Research Program. In its three-year study,some 46,000 randomly selected tax returns from2001 were intensively reviewed, and a tax gap of nearly one-fifth of all taxes (collected by the IRS)was identified. While this tax gap is sizable, mostpeople are compliant, and some people evade farmore than others. In the “wages, salaries and tips”

category, taxpayers underreport no more than only 1percent of the actual income. Yet, in the “nonfarmproprietor income” category, 57 percent of theincome goes unreported. The reason for such a largedifference between the wage earner and the self-employed is that the only person reporting the self-employed’s income to IRS is the self-employedhimself, whereas, for the wage earner, his employeris filling in a form to let the IRS know exactly howmuch he has been paid. The wage earner’s taxes areautomatically withheld from his every check, while

the self-employed have all year to decide if, and howmuch, he will pay. It is not that the average self-employed worker is less honest than the averagewage earner. Instead, the self-employed knows thatthe only chance the IRS has of learning his trueincome and expenditures is to audit him. But sincethe IRS audit rate is so low — the agency conductsface-to-face audits with no more than 0.20 percent of all individual taxpayers — he can be pretty confidentto go ahead and not disclose his actual income. Thestark differences in compliance rates across taxableitems that line up closely with detection rates suggeststrongly that many people pay their taxes not somuch because it is the right thing to do, but becausethey fear getting caught if they do not. Acombination of good technology (employer reportingand withholding) and poor logic (most tax-payersoverestimate their chances of being audited) makesthe system work. So the compliant taxpayer shoulddislike FBR not because it is too vigilant, but becauseit is not nearly vigilant enough. FBR requires, amongothers, a comprehensive risk-based compliancestrategy, including reliable data, field audits, andpenalties to enforce timely and accurate filing of returns..

Apart from better enforcement of laws, boosting taxmorale might be another way to increase taxcompliance. In some countries, people appear to befar more compliant than the low audit rates wouldsuggest. One explanation is that tax compliance isvoluntary due the intrinsic motivation of citizens to

pay taxes. Such tax morale depends on their attitudestoward the state. If the general population feels thatthe tax system treats them fairly and that they aregetting good value for their taxes, their willingness topay tax increases, and vice versa. Given this view,,increasing tax morale should increase voluntary taxcompliance. However, increasing the transparencyand accountability of the government is likely towork only over the long-term. In the meantime, thereis little alternative to an efficient, even-handed andstringent tax administration.

One important issue is how many resources to devoteto enforcing the tax laws. Just as it is not optimal tostation a police officer at each street corner toeliminate robbery, it is not optimal to completelyeliminate tax evasion. The tax gap estimates are notmeasures of the potential for additional enforcementyields because some would not be cost-effective tocollect. Nevertheless, the size of the tax gap suggeststhat Pakistan’s enforcement measures to date arevastly inadequate.

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 9/19

v

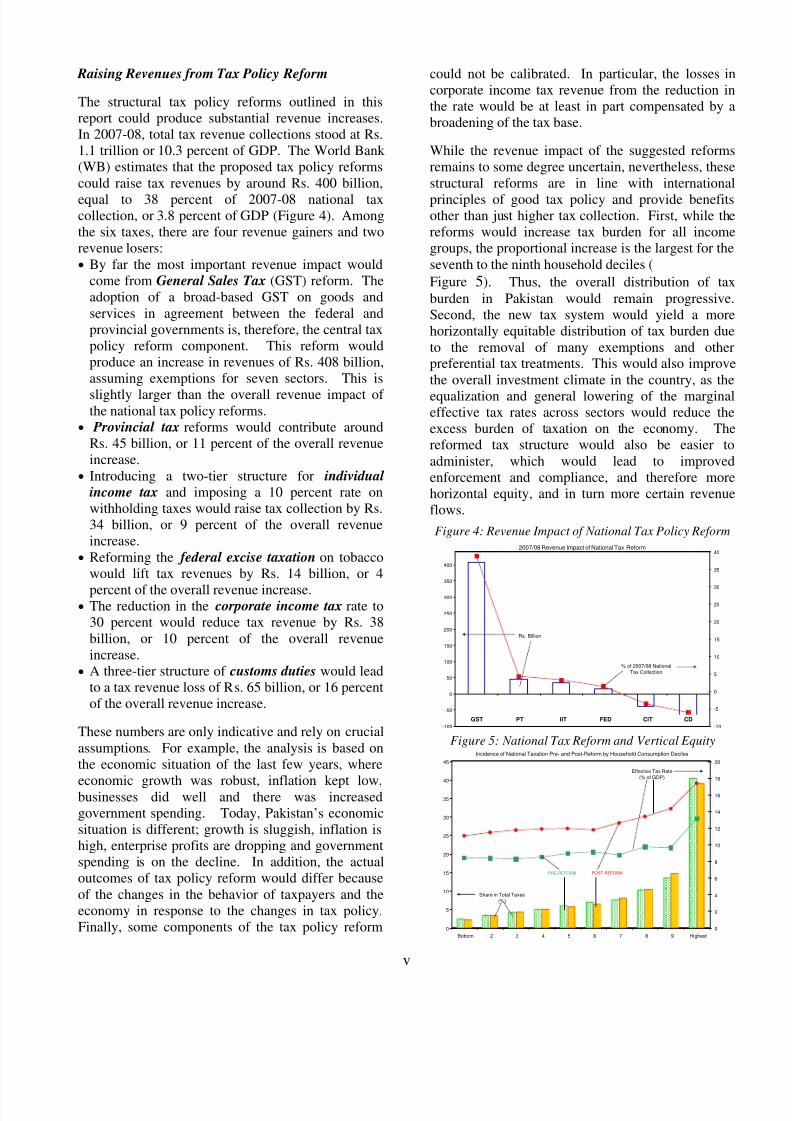

Raising Revenues from Tax Policy Reform

The structural tax policy reforms outlined in thisreport could produce substantial revenue increases.In 2007-08, total tax revenue collections stood at Rs.1.1 trillion or 10.3 percent of GDP. The World Bank (WB) estimates that the proposed tax policy reformscould raise tax revenues by around Rs. 400 billion,equal to 38 percent of 2007-08 national taxcollection, or 3.8 percent of GDP (Figure 4). Amongthe six taxes, there are four revenue gainers and tworevenue losers:• By far the most important revenue impact would

come from General Sales Tax (GST) reform. Theadoption of a broad-based GST on goods andservices in agreement between the federal andprovincial governments is, therefore, the central taxpolicy reform component. This reform wouldproduce an increase in revenues of Rs. 408 billion,assuming exemptions for seven sectors. This isslightly larger than the overall revenue impact of the national tax policy reforms.

• Provincial tax reforms would contribute aroundRs. 45 billion, or 11 percent of the overall revenueincrease.

• Introducing a two-tier structure for individual income tax and imposing a 10 percent rate onwithholding taxes would raise tax collection by Rs.34 billion, or 9 percent of the overall revenueincrease.

• Reforming the federal excise taxation on tobaccowould lift tax revenues by Rs. 14 billion, or 4

percent of the overall revenue increase.• The reduction in the corporate income tax rate to

30 percent would reduce tax revenue by Rs. 38billion, or 10 percent of the overall revenueincrease.

• A three-tier structure of customs duties would leadto a tax revenue loss of Rs. 65 billion, or 16 percentof the overall revenue increase.

These numbers are only indicative and rely on crucialassumptions. For example, the analysis is based onthe economic situation of the last few years, where

economic growth was robust, inflation kept low,businesses did well and there was increasedgovernment spending. Today, Pakistan’s economicsituation is different; growth is sluggish, inflation ishigh, enterprise profits are dropping and governmentspending is on the decline. In addition, the actualoutcomes of tax policy reform would differ becauseof the changes in the behavior of taxpayers and theeconomy in response to the changes in tax policy.Finally, some components of the tax policy reform

could not be calibrated. In particular, the losses incorporate income tax revenue from the reduction inthe rate would be at least in part compensated by abroadening of the tax base.

While the revenue impact of the suggested reformsremains to some degree uncertain, nevertheless, thesestructural reforms are in line with internationalprinciples of good tax policy and provide benefitsother than just higher tax collection. First, while thereforms would increase tax burden for all incomegroups, the proportional increase is the largest for theseventh to the ninth household deciles (Figure 5). Thus, the overall distribution of taxburden in Pakistan would remain progressive.Second, the new tax system would yield a morehorizontally equitable distribution of tax burden dueto the removal of many exemptions and otherpreferential tax treatments. This would also improvethe overall investment climate in the country, as theequalization and general lowering of the marginaleffective tax rates across sectors would reduce theexcess burden of taxation on the economy. Thereformed tax structure would also be easier toadminister, which would lead to improvedenforcement and compliance, and therefore morehorizontal equity, and in turn more certain revenueflows.

Figure 4: Revenue Impact of ational Tax Policy Reform2007/08 Revenue Impact of National Tax Reform

Rs. Billion

% of 2007/08 NationalTax Collection

-100

-50

0

50

100

150

200

250

300

350

400

-10

-5

0

5

10

15

20

25

30

35

40

GST PT IIT FED CIT CD

Figure 5: ational Tax Reform and Vertical Equity

Incidence of National Taxation Pre- and Post-Reform by Household Consumption Deciles

Share in Total Taxes(%)

Effective Tax Rate(% of GDP)

0

5

10

15

20

25

30

35

40

45

Bottom 2 3 4 5 6 7 8 9 Highest0

2

4

6

8

10

12

14

16

18

20

PRE-REFORM POST-REFORM

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 10/19

vi

Sequencing Tax Policy Reform

Any successful reform has to take along three corestakeholders: the tax administration (FBR), thetaxpayer and the policy maker. First, meeting thisgoal will not only be about bringing changes in taxpolicy but also about changes in tax administration.In the past, reform initiatives failed because there wasinadequate focus on ensuring that tax policy reformscould be well administered. Federal taxadministrators have made good progress in a numberof areas, but more efforts are needed to completeFBR’s modernization program over the next fewyears. Similar efforts are needed to strengthen taxadministration at the provincial level, such. Second,although overall tax burdens in Pakistan are low, thedistribution of those tax burdens among householdsand among economic sectors is highly unbalanced.The taxpaying members of society who are tocompete in an increasingly globalized world arelikely to oppose reforms if they see them as furtherincreasing their tax burden while doing little to taxother individuals and businesses that pay little or notaxes. Third, the fiscal position of the government isweak and could deteriorate further in view of theeconomic slowdown. This will make policy makersreluctant to provide leadership on tax reforms thatmay be considered uncertain in their revenue impact,especially if they face opposition from interestgroups.

Because some of the ills afflicting Pakistan’s taxsystem have been the outcome of past policymeasures, it will be important to spend time andeffort to generate broad consensus for the proposedreform package. Many tax incentives andpreferential treatments that have been prevalent sincelong, will be difficult to remove. The politicaleconomy of tax reforms in other countries suggeststhe importance of having a broad package that asksfor the sacrifices of many but also offers generaladvantages including simpler taxes and reduced taxrates. In the case of a gradual implementation of thereforms (Table 2), there is a risk that the reforms

which are easier to implement will be picked first andthe more controversial reforms requiring a strongerdetermination, will be delayed, and ultimatelyderailed. One way to guard against this is to separatethe approval of the tax reform package, which couldbe done upfront for the whole agenda, and the timingof its implementation, which could be donesequentially. This approach could also help inovercoming resistance from particular groups, suchas sectors affected by the removal of tax preferences.The overall gains from this whole reform effortshould be properly highlighted to increasestakeholder involvement.

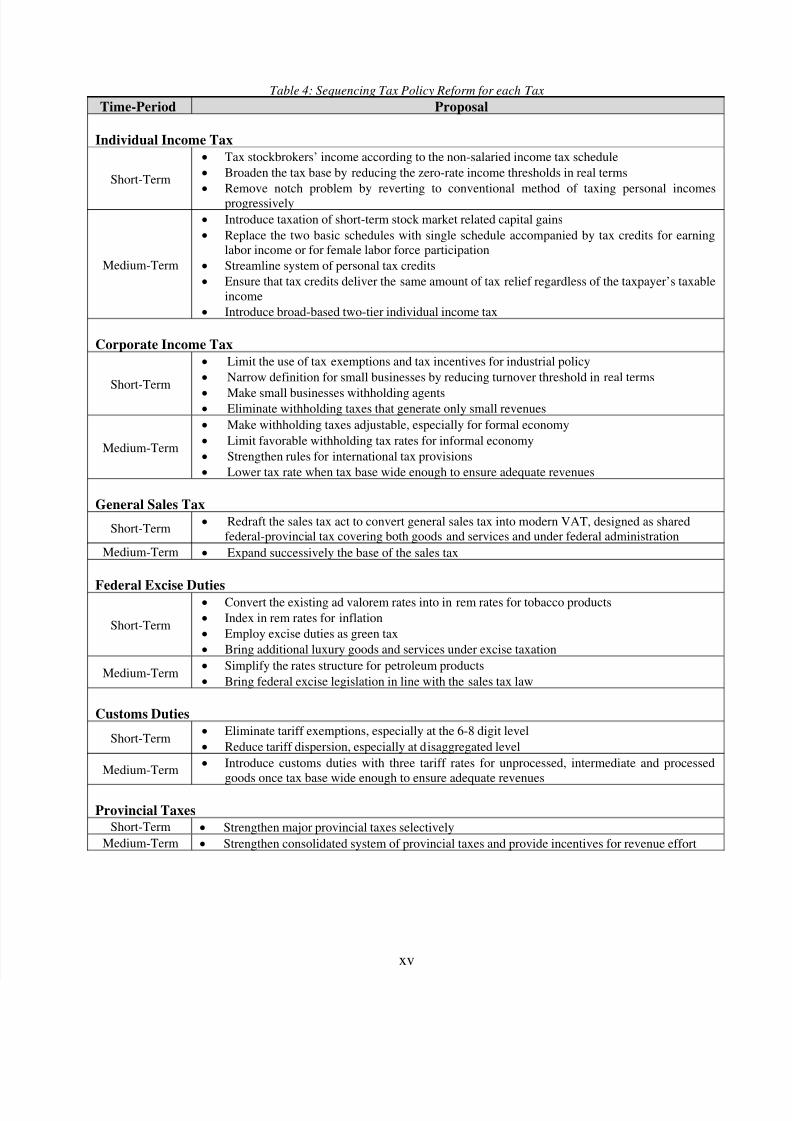

The right sequencing of tax policy measures will beimportant to sustain the reform program. If some of the expected outcomes of the reforms do not fullymaterialize, a backlash against change could stall itsimplementation. This highlights the importance of acomprehensive analytical preparation (Table 3) and aroad-map for the successful reform of each major taxcomponent (Table 4).

Ensuring early gains should be part of theimplementation strategy. The broadening of the taxbase should have priority compared to rationalizationof taxes, and especially compared to tax ratereduction. Across taxes, GST reform should be thefirst priority, followed by reforms of provincial taxes,individual income tax and federal excise tax, whilethe reforms of custom duties and corporate incometax should have the lowest priority (Table 1). For example, trade reform with a reductionand unification of the customs tariffs is desirable, butit should be put on hold until it is certain that therevenue losses from trade liberalization would beoffset by larger collections from domestic taxes,especially the GST. When we combine tax by tax therevenue potential from tax policy reform with thepotential from tax gap elimination, corporate incometax and GST are the most important areas requiringreforms.

Table 1: Sequencing Tax Policy Reform Across Taxes and Issues

Broadening of Tax Bases Rationalization of Taxes Reduction in Tax Rates

FIRST PRIORITY THIRD PRIORITY

GST PT, IIT, FED CD, CIT

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 11/19

vii

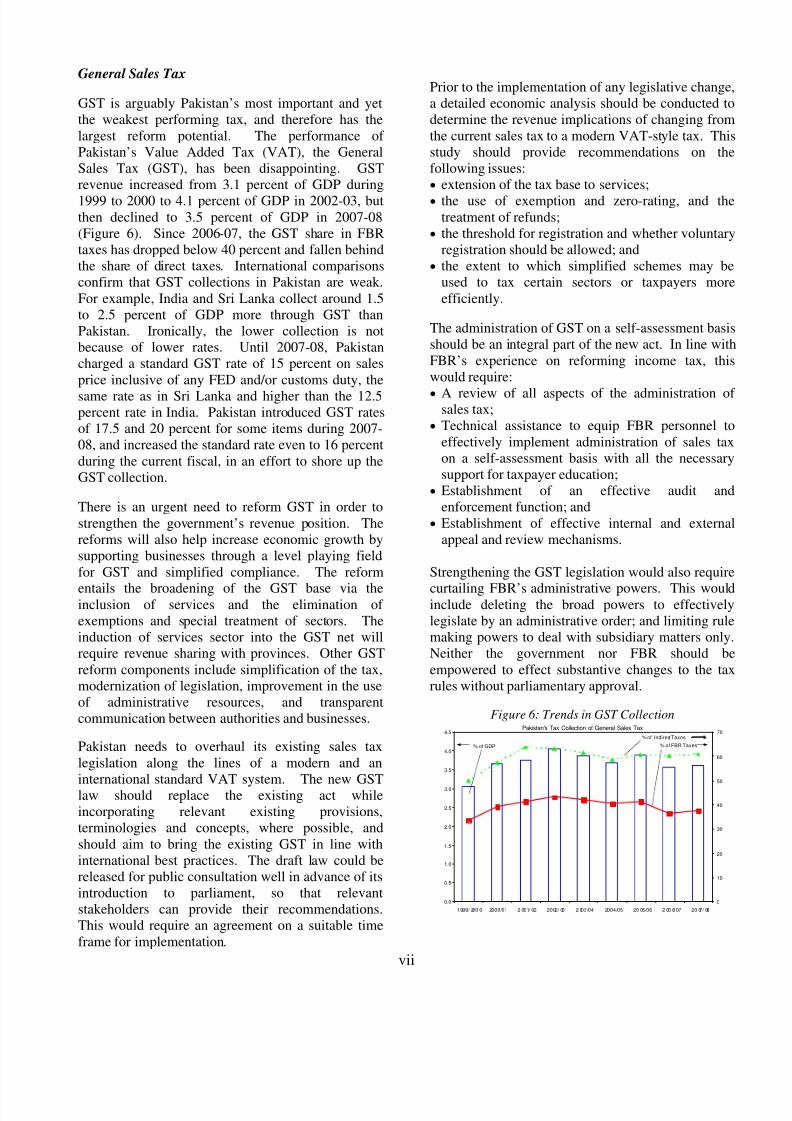

General Sales Tax

GST is arguably Pakistan’s most important and yetthe weakest performing tax, and therefore has thelargest reform potential. The performance of Pakistan’s Value Added Tax (VAT), the GeneralSales Tax (GST), has been disappointing. GSTrevenue increased from 3.1 percent of GDP during1999 to 2000 to 4.1 percent of GDP in 2002-03, butthen declined to 3.5 percent of GDP in 2007-08(Figure 6). Since 2006-07, the GST share in FBRtaxes has dropped below 40 percent and fallen behindthe share of direct taxes. International comparisonsconfirm that GST collections in Pakistan are weak.For example, India and Sri Lanka collect around 1.5to 2.5 percent of GDP more through GST thanPakistan. Ironically, the lower collection is notbecause of lower rates. Until 2007-08, Pakistancharged a standard GST rate of 15 percent on salesprice inclusive of any FED and/or customs duty, thesame rate as in Sri Lanka and higher than the 12.5percent rate in India. Pakistan introduced GST ratesof 17.5 and 20 percent for some items during 2007-08, and increased the standard rate even to 16 percentduring the current fiscal, in an effort to shore up theGST collection.

There is an urgent need to reform GST in order tostrengthen the government’s revenue position. Thereforms will also help increase economic growth bysupporting businesses through a level playing fieldfor GST and simplified compliance. The reform

entails the broadening of the GST base via theinclusion of services and the elimination of exemptions and special treatment of sectors. Theinduction of services sector into the GST net willrequire revenue sharing with provinces. Other GSTreform components include simplification of the tax,modernization of legislation, improvement in the useof administrative resources, and transparentcommunication between authorities and businesses.

Pakistan needs to overhaul its existing sales taxlegislation along the lines of a modern and an

international standard VAT system. The new GSTlaw should replace the existing act whileincorporating relevant existing provisions,terminologies and concepts, where possible, andshould aim to bring the existing GST in line withinternational best practices. The draft law could bereleased for public consultation well in advance of itsintroduction to parliament, so that relevantstakeholders can provide their recommendations.This would require an agreement on a suitable timeframe for implementation.

Prior to the implementation of any legislative change,a detailed economic analysis should be conducted todetermine the revenue implications of changing fromthe current sales tax to a modern VAT-style tax. Thisstudy should provide recommendations on thefollowing issues:• extension of the tax base to services;• the use of exemption and zero-rating, and the

treatment of refunds;• the threshold for registration and whether voluntary

registration should be allowed; and• the extent to which simplified schemes may be

used to tax certain sectors or taxpayers moreefficiently.

The administration of GST on a self-assessment basisshould be an integral part of the new act. In line withFBR’s experience on reforming income tax, thiswould require:• A review of all aspects of the administration of

sales tax;• Technical assistance to equip FBR personnel to

effectively implement administration of sales taxon a self-assessment basis with all the necessarysupport for taxpayer education;

• Establishment of an effective audit andenforcement function; and

• Establishment of effective internal and externalappeal and review mechanisms.

Strengthening the GST legislation would also require

curtailing FBR’s administrative powers. This wouldinclude deleting the broad powers to effectivelylegislate by an administrative order; and limiting rulemaking powers to deal with subsidiary matters only.Neither the government nor FBR should beempowered to effect substantive changes to the taxrules without parliamentary approval.

Figure 6: Trends in GST Collection Pakistan's Tax Collection of General Sales Tax

% of GDP % of FBR Taxes

% of Indirect Taxes

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1999/ 200 0 2000/01 2 001/ 02 2002/ 03 2 003/04 2004/05 20 05/06 2 00 6/ 07 20 07/ 08

0

10

20

30

40

50

60

70

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 12/19

viii

Corporate Income Tax

Following international trends, Pakistan’s corporateincome tax rates have come down markedly. In theearly 1990s, banking, public and private companieswere taxed at the rate of 66 percent, 44 percent and55 percent, respectively. By 2007, Pakistan adopteda uniform corporate tax rate of 35 percent on taxableprofits for both public and private sector companies.In spite of the rate reductions, collections from thecorporate income tax improved during this decade onthe back of the economic upturn. It increased from1.2 percent of GDP in 2000-01 to 2.5 percent in2007-08 (Figure 7). The share of the corporateincome tax jumped from one-half to two-thirds ingross direct taxes, and from one-seventh to one-quarter in gross FBR taxes. Revenue collectionimproved sharply during 2006-07, primarily due tothe doubling of nominal tax collection from thefinancial sector, in addition to a significantperformance from public and foreign ownedcompanies from the oil and gas sector. However, theongoing slowdown in the economy poses a risk forcorporate income tax collection during the currentfiscal (2008-09).

The corporate income tax system requires change inpolicy and administration, as well as thestrengthening of international tax provisions. Theinternational trend is towards lower income tax ratesas a means of increasing economic competitiveness.Pakistan needs to respond to this challenge. Onlywith a broader tax base is there room to cut incometax rates and to enhance the attractiveness forinternational capital. Hence, the main priority shouldbe to broaden tax base and lower tax rates.Specifically, the statutory tax rate of the corporateincome tax could be reduced. This would bringPakistan more in line with peer countries and willhelp to significantly reduce the distorting effects of the corporate tax. At the same time, expanding thebase of the corporate income tax, mainly by reducingor rationalizing the use of tax incentives andexemptions, could ensure that the reduction in the

statutory rates does not lead to revenue loss, andinstead bolsters efficiency and equity. In this regard,it would be important to undertake a completeexamination of the costs and benefits of taxincentives and exemptions. In addition, thethresholds for small businesses could be reexaminedin order to ensure that only truly small businessesqualify.

The second priority of tax policy reform is torationalize the withholding tax system. Theextensive use of withholding taxes increases theeffective tax rate on companies; creates opportunitiesfor tax evasion schemes; masks serious complianceissues; and, through the many special stipulations,complicates the tax system. In many cases,withholding taxes become final liabilities. As aresult, many taxpayers are caught in the withholdingtax net, even though their incomes would put them inthe zero-rate bracket under the regular tax schedule.Some withholding taxes often resemble excise taxesmore than income taxes, as in the case of withholdingon imports, exports and sales of goods and services.As a general rule, whenever they are imposed on theformal economy, withholding taxes should beconsidered an advance payment of the final taxliability. Withholding taxes that generate trivialamounts of revenues could well be eliminated.Finally, clarifying FBR’s rules for classifyingwithholding taxes into the different income tax headswill improve the understanding of their impact of thesystem of direct taxation, and hence improve FBR’sability to identify and implement good performancepolicies.

With regard to international tax provisions, there arethree areas requiring reforms. First, there is a needfor policy level guidance on new sectors, coveringresidency, e-commerce, banking and financialactivities, turnkey projects, and the establishment of areliable transfer price, in the 2002 Income Tax Rules.Second, a number of steps could help to limit the useof transfer pricing provisions to exclusively anti-avoidance situations. Third, double taxationagreements should be provided with more detailedimplementation rules. For example, the currentagreements provide no guidance on the interpretationof terms like “center of vital interests” and “effectiveplace of management” or on the application of reduced withholding tax rates.

Figure 7: Trends in Corporate Income Tax Collection Pakistan's Gross Tax Collection of Corporate Income Tax

% of GDP

% of FBRGross Taxes

% of FBRGross Direct Taxes

0.0

0.3

0.6

0.9

1.2

1.5

1.8

2.1

2.4

2.7

3.0

2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/080

10

20

30

40

50

60

70

80

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 13/19

ix

Individual Income Tax

The individual income tax is typically not popularamong taxpayers, yet it needs to be part and parcel of the tax system. As a direct tax on individuals, ratherthan an indirect tax on transactions, it relies on thetax administration taking a slice of a hard-earnedmoney of workers and the business income of theself-employed. At the same time, the individualincome tax is central to a society’s notion of raisingrevenue in a fair and equitable way. By allowing theassessment of individual economic circumstances,the income tax is naturally better suited for making atax structure progressive rather than through indirecttaxes.

Pakistan’s tax yield from individual income tax isinadequately low and has declined since the early2000s. Partly due to a reduction in income tax rates,gross revenues from the individual income tax

declined from 1.5 percent of GDP in 2000-01 to 1.1percent during 2007-08 (Figure 8). The individualincome tax accounts for around 11 percent of overallFBR tax revenues and 29 percent of direct taxrevenues, which also include the corporate incometax, capital value tax and social security taxes. Thislevel of revenue mobilization would seem to putPakistan somewhere in the middle rank amongemerging market economies. However, Pakistan’sstanding might actually be worse than what thenumbers suggest for three reasons. First, Pakistan’sindividual income tax is measured in gross receipts,

which include refunds. Second, there are twocategories of taxpayers liable to individual incometax in Pakistan: workers and salaried individuals; andsmall unincorporated businesses and associations of persons, including firms with a profit sharingagreement. This may be in part due to a moreexpansive definition of individual income tax thanthe ones used in other developing countries. Indeed,FBR refers to the individual income tax as a non-corporate income tax. Finally and most importantly,the individual income tax collection includes a shareof the funds mobilized through withholding taxes.

Some of the withholding taxes are presumptive,imposing a fixed charge on certain transactions. Thisarrangement, in many cases, turns such withholdingtaxes effectively into indirect taxes. Since the heavyreliance on withholding taxes is unusual, this movesup Pakistan’s rank in country comparisons onindividual income tax collections.

There are two priorities in the reform of theindividual income tax. First, streamlining credits and

phasing out many exemptions would move it closerto a fully-fledged broad-based income tax. The taxcredits could be reshaped so that the amount of targeted allowances remains unchanged, irrespectiveof the income level of the beneficiary taxpayer.While most exemptions and credits are relativelyminor, there is one noticeable exception. Imposing amodest tax on short-term stock market related capitalgains would seem attractive from multipleperspectives: it benefits the national exchequer bygenerating revenues over the medium term; itimproves efficiency by making companies moreindifferent between retained earnings and paying outdividends; and it improves equity by making the taxsystem more progressive. Arguably, it would also begood politics, as it would be a symbol for agovernment ready to tackle powerful lobbies for thenational interest. Whatever is done with the capitalgains tax, there is every reason to tax the incomes of stockbrokers according to the regular schedule fornon-salaried taxpayers

Second, the tax design can be simplified. Theindividual income tax operates with two basicschedules for recipients of wage and non-wage orbusiness income. There are anywhere from fourteento twenty different tax brackets, each having large butdifferent zero rate brackets for men and women. Thehigh threshold level could be addressed over time bykeeping the zero-band constant in nominal terms inspite of inflation. The individual income tax applieshigher marginal tax rates to the total amount of a

non-salaried taxpayer’s income. This problem canresult in punitively high effective rates of marginaltaxation and create perverse incentives to accuratelyreport additional amounts of taxable income. Themarginal tax relief introduced in 2008-09, mitigatesthis problem to some extent, but it furthercomplicates the tax system and applies only forsalaried taxpayers.

Figure 8: Trends in Individual Income Tax Collection Pakistan's Gross Tax Collection of Individual Income Tax

% of GDP

As % of FB R GrossTaxes

As % of FBR GrossDirect Taxes

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

2000/01 2001/ 02 2002/03 2003/04 2004/05 2005/ 06 2006/07 2007/08

0

5

10

15

20

25

30

35

40

45

50

55

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 14/19

x

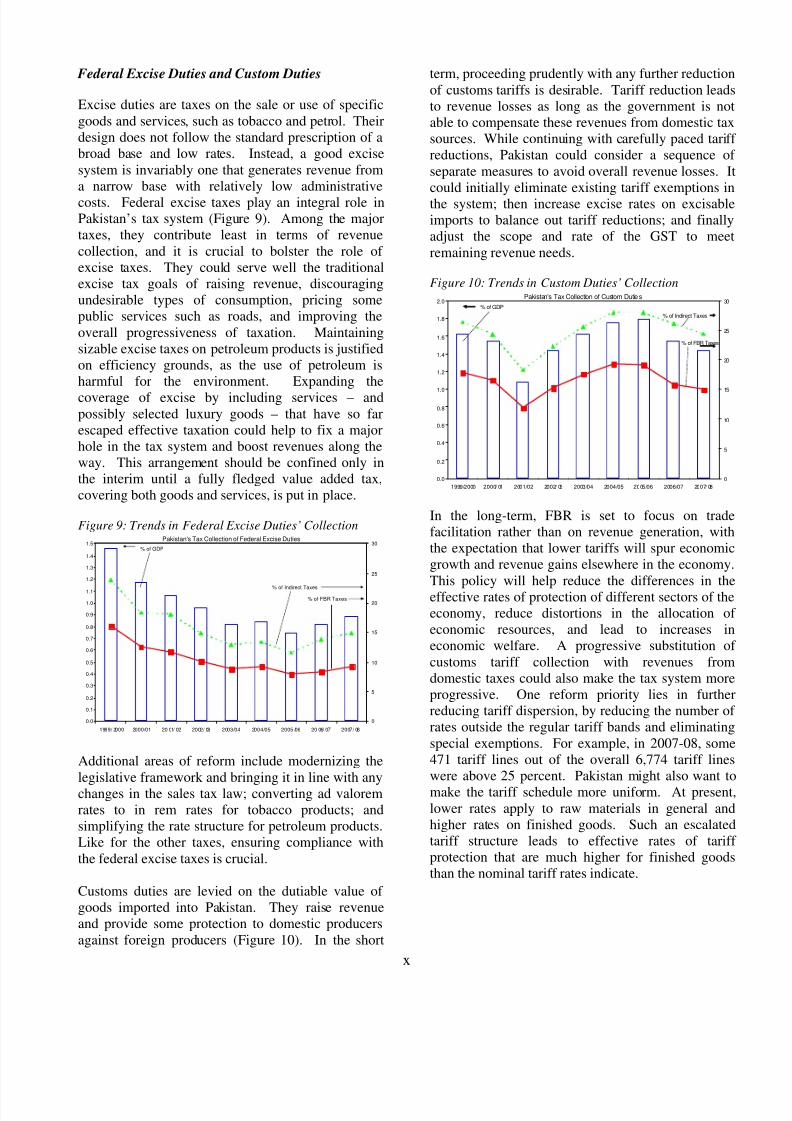

Federal Excise Duties and Custom Duties

Excise duties are taxes on the sale or use of specificgoods and services, such as tobacco and petrol. Theirdesign does not follow the standard prescription of abroad base and low rates. Instead, a good excisesystem is invariably one that generates revenue froma narrow base with relatively low administrativecosts. Federal excise taxes play an integral role inPakistan’s tax system (Figure 9). Among the majortaxes, they contribute least in terms of revenuecollection, and it is crucial to bolster the role of excise taxes. They could serve well the traditionalexcise tax goals of raising revenue, discouragingundesirable types of consumption, pricing somepublic services such as roads, and improving theoverall progressiveness of taxation. Maintainingsizable excise taxes on petroleum products is justifiedon efficiency grounds, as the use of petroleum isharmful for the environment. Expanding thecoverage of excise by including services – andpossibly selected luxury goods – that have so farescaped effective taxation could help to fix a majorhole in the tax system and boost revenues along theway. This arrangement should be confined only inthe interim until a fully fledged value added tax,covering both goods and services, is put in place.

Figure 9: Trends in Federal Excise Duties’ CollectionPakistan's Tax Collection of Federal Excise Duties

% of GDP

% of FBR Taxes% of Indirect Taxes

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1999/ 2000 2000/01 20 01/ 02 2002/ 03 2003/04 2004/05 2005 /06 20 06/ 07 2007/ 08

0

5

10

15

20

25

30

Additional areas of reform include modernizing thelegislative framework and bringing it in line with anychanges in the sales tax law; converting ad valoremrates to in rem rates for tobacco products; andsimplifying the rate structure for petroleum products.Like for the other taxes, ensuring compliance withthe federal excise taxes is crucial.

Customs duties are levied on the dutiable value of goods imported into Pakistan. They raise revenueand provide some protection to domestic producersagainst foreign producers (Figure 10). In the short

term, proceeding prudently with any further reductionof customs tariffs is desirable. Tariff reduction leadsto revenue losses as long as the government is notable to compensate these revenues from domestic taxsources. While continuing with carefully paced tariff reductions, Pakistan could consider a sequence of separate measures to avoid overall revenue losses. Itcould initially eliminate existing tariff exemptions inthe system; then increase excise rates on excisableimports to balance out tariff reductions; and finallyadjust the scope and rate of the GST to meetremaining revenue needs.

Figure 10: Trends in Custom Duties’ CollectionPakistan's Tax Collection of Custom Dutie s

% of GDP

% of FBR Taxes

% of Indirect Taxes

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

1999/2000 2000/ 01 2001/02 2002/ 03 2003/04 2004/05 2005/06 2006/07 2007/ 080

5

10

15

20

25

30

In the long-term, FBR is set to focus on tradefacilitation rather than on revenue generation, withthe expectation that lower tariffs will spur economicgrowth and revenue gains elsewhere in the economy.This policy will help reduce the differences in theeffective rates of protection of different sectors of theeconomy, reduce distortions in the allocation of economic resources, and lead to increases ineconomic welfare. A progressive substitution of customs tariff collection with revenues fromdomestic taxes could also make the tax system moreprogressive. One reform priority lies in furtherreducing tariff dispersion, by reducing the number of rates outside the regular tariff bands and eliminatingspecial exemptions. For example, in 2007-08, some471 tariff lines out of the overall 6,774 tariff lineswere above 25 percent. Pakistan might also want tomake the tariff schedule more uniform. At present,lower rates apply to raw materials in general andhigher rates on finished goods. Such an escalatedtariff structure leads to effective rates of tariff protection that are much higher for finished goodsthan the nominal tariff rates indicate.

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 15/19

xi

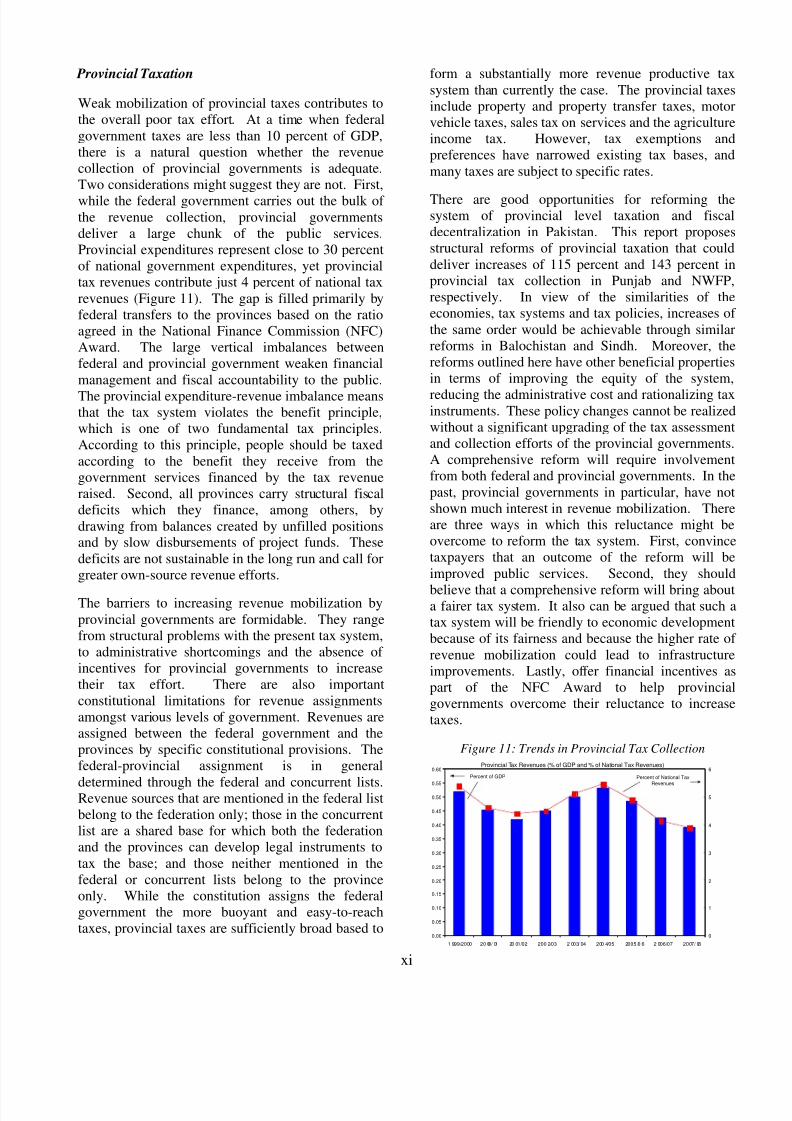

Provincial Taxation

Weak mobilization of provincial taxes contributes tothe overall poor tax effort. At a time when federalgovernment taxes are less than 10 percent of GDP,there is a natural question whether the revenuecollection of provincial governments is adequate.Two considerations might suggest they are not. First,while the federal government carries out the bulk of the revenue collection, provincial governmentsdeliver a large chunk of the public services.Provincial expenditures represent close to 30 percentof national government expenditures, yet provincialtax revenues contribute just 4 percent of national taxrevenues (Figure 11). The gap is filled primarily byfederal transfers to the provinces based on the ratioagreed in the National Finance Commission (NFC)Award. The large vertical imbalances betweenfederal and provincial government weaken financialmanagement and fiscal accountability to the public.The provincial expenditure-revenue imbalance meansthat the tax system violates the benefit principle,which is one of two fundamental tax principles.According to this principle, people should be taxedaccording to the benefit they receive from thegovernment services financed by the tax revenueraised. Second, all provinces carry structural fiscaldeficits which they finance, among others, bydrawing from balances created by unfilled positionsand by slow disbursements of project funds. Thesedeficits are not sustainable in the long run and call forgreater own-source revenue efforts.

The barriers to increasing revenue mobilization byprovincial governments are formidable. They rangefrom structural problems with the present tax system,to administrative shortcomings and the absence of incentives for provincial governments to increasetheir tax effort. There are also importantconstitutional limitations for revenue assignmentsamongst various levels of government. Revenues areassigned between the federal government and theprovinces by specific constitutional provisions. Thefederal-provincial assignment is in general

determined through the federal and concurrent lists.Revenue sources that are mentioned in the federal listbelong to the federation only; those in the concurrentlist are a shared base for which both the federationand the provinces can develop legal instruments totax the base; and those neither mentioned in thefederal or concurrent lists belong to the provinceonly. While the constitution assigns the federalgovernment the more buoyant and easy-to-reachtaxes, provincial taxes are sufficiently broad based to

form a substantially more revenue productive taxsystem than currently the case. The provincial taxesinclude property and property transfer taxes, motorvehicle taxes, sales tax on services and the agricultureincome tax. However, tax exemptions andpreferences have narrowed existing tax bases, andmany taxes are subject to specific rates.

There are good opportunities for reforming thesystem of provincial level taxation and fiscaldecentralization in Pakistan. This report proposesstructural reforms of provincial taxation that coulddeliver increases of 115 percent and 143 percent inprovincial tax collection in Punjab and NWFP,respectively. In view of the similarities of theeconomies, tax systems and tax policies, increases of the same order would be achievable through similarreforms in Balochistan and Sindh. Moreover, thereforms outlined here have other beneficial propertiesin terms of improving the equity of the system,reducing the administrative cost and rationalizing taxinstruments. These policy changes cannot be realizedwithout a significant upgrading of the tax assessmentand collection efforts of the provincial governments.A comprehensive reform will require involvementfrom both federal and provincial governments. In thepast, provincial governments in particular, have notshown much interest in revenue mobilization. Thereare three ways in which this reluctance might beovercome to reform the tax system. First, convincetaxpayers that an outcome of the reform will beimproved public services. Second, they should

believe that a comprehensive reform will bring abouta fairer tax system. It also can be argued that such atax system will be friendly to economic developmentbecause of its fairness and because the higher rate of revenue mobilization could lead to infrastructureimprovements. Lastly, offer financial incentives aspart of the NFC Award to help provincialgovernments overcome their reluctance to increasetaxes.

Figure 11: Trends in Provincial Tax CollectionProvincial Tax Revenues (% of GDP and % of National Tax Revenues)

Percent of GDP Percent of National Tax

Revenues

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0.55

0.60

1 999/2000 20 00/ 01 20 01/02 200 2/03 2 003/ 04 200 4/05 2005 /0 6 2 006/07 2007/ 08

0

1

2

3

4

5

6

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 16/19

xii

Scope and Process

The Pakistan Tax Policy Report provides acomprehensive assessment of Pakistan’s tax policiesand lays out options for its reform. It is based onwork commissioned for this report and oncontributions of other researchers in Pakistan andelsewhere. The report has four parts (Figure 12).The first part, this chapter, argues from amacroeconomic perspective that there are no viablealternatives to mobilizing tax revenues for financinggovernment expenditures. The second part, Chapter2, pulls together the main findings to lay out aroadmap for tax reform. It presents a comprehensivemedium-term reform agenda for tapping tax basesaimed at Pakistan’s development. The third part,Chapter 3, subjects Pakistan’s tax system to a basichealth check and assesses with regard to the fourproperties of adequacy, efficiency, equity andcompliance. The final part, covered in Chapter 4 toChapter 9, takes each major tax and discusses how itsquares up with regard to the properties spelled out inChapter 3.

This report is the outcome of a partnership amongthree parties: the FBR; the Andrew Young School of Policy Studies (AYSPS) at Georgia State University,and the World Bank (WB). The Government of Pakistan (GoP) attaches high priority to broadeningthe tax base in an efficient and equitable manner, andis aware of the need for further improvements in theexisting tax system. Following the launch of a

project of FBR and the WB on tax administrationreform in 2005, the government wanted to start aparallel initiative on tax policy. In response to thegovernment’s request, a partnership among the threeparties was formed in January 2007. Additionalgovernment counterparts included the Ministry of Finance (MoF) and finance departments of Punjaband Balochistan. The services of AYSPS were

generously supported through the UK Department forInternational Development (DFID).

This collaboration extended beyond the delivery of areport. Pakistan’s capacity to undertake fiscal policyanalysis is limited, despite some positives at FBR andelsewhere. As part of a long-term remedy, initiativessuch as postgraduate training of FBR and MoFpersonnel in fiscal policy, similarly expanding thenumber of positions dedicated to tax policy analysisin those institutions, and offering more attractivesalary and working conditions to draw and retain theright people are much needed. Such measures werebeyond the scope of this project. Nevertheless, otherforms of capacity building took place by the jointwork of the AYSPS experts and government taxpolicy analysis experts, ensuring that the process of preparing the report served as a “teaching tool” forcapacity building and a “collaborative tool” to buildownership. Many of these mechanisms also servedas dissemination tools to stimulate dialogue. Thereport’s primary audience is the federal andprovincial governments. The report is also writtenfor policymakers and development practitioners inPakistan, as well as for governments andinternational donors that support tax policy reform inother South Asian countries. The report is expectedto generate debate and discussions among the civilsociety and research communities.

The background studies for this report werestructured as a series of seven tax policy papers. The

AYSPS teams visited Pakistan two times in thecourse of the preparation of each policy paper. Thefirst mission gathered the basic information, helddetailed discussions with government staff and otherstakeholders, and came to an agreement with thePakistan authorities on the coverage of each taxpolicy study. The second mission presented the draftpolicy paper and collected comments and feedback for the final report of the study.

Figure 12: avigational Aid for the Report

Adequacy Efficiency Equity Compliance

CHAPTER I V CHA PTER V C HAPTE R VI CHAPTER VI I CHAPTER VIII CHAPTER IX

CHAPTER II

ProvincialTaxes

FederalExcise Duties

National Tax Policy Reform

General SalesTax

CorporateIncome Tax

IndividualIncome Tax

CustomsDuties

OBJECTIVE

PROPERTIES

TAXES

STRATEGY

CHAPTER I

CHAPTER III

Tapping Tax Bases f or Development

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 17/19

xiii

Table 2: Piecemeal and Comprehensive Tax Policy MatrixReform Type Proposal

Individual Income Tax• Introduce taxation o f short-term stock market related capital ga ins• Tax stockbrokers’ income according to the non-salaried income tax schedule• Broaden the tax base by reducing the zero-rate income thresh olds in real terms• Replace the two basic schedules with single schedule accompanied by tax credits for earning labor

income or for female labor force participation• Remove notch problem by reverting to conventional method of taxing personal incomes

progressively• Reduce significantly the nu mber of tax brackets

Piecemeal

• Streamline sys tem of personal tax c redits (charity; pens ions; purchases of new shares; purchases of housing)

• Ensure that tax credits deliver the same amount of tax relief regardless of the taxpayer’s taxableincome

Comprehensive • Introduce broad-based two-tier indiv idual income tax

Corporate Income Tax•

Limit the use of tax exempt ions and tax incentives for indus trial policy• Make withholding taxes adjustab le for formal econo my• Limit favorable withholding tax rates for informal economy• Eliminate w ithholding taxes that generate only s mall revenues• Narrow def init ion for small bus inesses by reducing turnover threshold in real terms• Make small bus inesses withholding agents

Piecemeal

• Strengthen rules for international tax provisionsComprehensive • Introduce corporate income ta x with lower rate and wider ta x base

General Sales Tax• Redraft the sales ta x act to convert general sales tax into modern VAT, des igned as shared federal-

provincial tax covering both goods and services and und er federal administrationPiecemea l and

Comprehensive• Expand successively the base of the sales tax

Federal Excise Duties• Bring federal excise leg islation in line with the s ales tax law• Convert the existing ad valorem rates into in rem rates for tobacco products• Index in rem rates for inflation• Emp loy excise dut ies as g reen tax and s imp lify the rates structure for petroleum products

Piecemea l andComprehensive

• Bring additional luxu ry goods and services under excise taxat ion

Customs Duties• Combine tariff reductions with a sequence of separate measures to avoid overall revenue losses,

including elimination of existing tariff exemptions (especially at the 6-8 digit level), increases inexcisab le imports; and expansion of the y ield fro m general sales taxPiecemeal

•

Reduce tariff d ispersion, especially at disaggregated levelComprehensive • Introduce customs duties with three tariff rates for unprocessed, intermediate and processed goods. Provincial Taxes

Piecemeal • Strengthen major provincial ta xes selectivelyComprehensive • Strengthen consolidated system of provincia l taxes and provide incentives for revenue effort

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 18/19

xiv

Table 3: Analytical Preparation of Tax Policy ReformAll Taxes• Harmonize tax definitions and tax procedures for all domestic taxes and modernize the

delegation framework for the revenue laws• Conduct economic analysis of specific proposals for tax policy changes, including expansion of

the tax bases and adjustment in rates. This work includes the following:Individual Income Tax• Develop reformed system of tax credits• Develop transition plan from current system of multiple tax brackets to two-tier tax ratesCorporate Income Tax• Establish clear attribution of withholding tax collection to salaried taxpayers, non-salaried

taxpayers and corporations• Review each withholding tax with regard to its revenue impact, base, rate and adjustability • Evaluate treatment of debt and equity • Assess potential to widen corporate income tax base through the elimination of exemptions,

investment incentives and special treatmentsGeneral Sales Tax • Develop plan for widening successively the tax base• Develop revenue sharing formula between federal government and provincial governmentsFederal Excise Duties • Assess scope for increasing taxation of luxury goods and services• Develop reformed system of petroleum productsCustom Duties • Assess scope for expanding the base of dutiable imports• Develop transition plan from current multiple duties rates structure to three-tier duty rate

structureProvincial Taxes

• Conduct provincial tax policy analyses for Balochistan and Sindh• Develop reform proposals for revised National Finance Commission Award that include

incentives for provincial revenue effort

8/7/2019 Pak Policy 1

http://slidepdf.com/reader/full/pak-policy-1 19/19

xv

Table 4: Sequencing Tax Policy Reform for each TaxTime-Period Proposal

Individual Income Tax

Short-Term

• Tax stockbrokers’ income according to the non-salaried income tax schedule• Broaden the tax base by reducing the zero-rate income thresholds in real terms• Remove notch problem by reverting to conventional method of taxing personal incomes

progressively

Medium-Term

• Introduce taxation of short-term stock market related capital gains • Replace the two basic schedules with single schedule accompanied by tax credits for earning

labor income or for female labor force participation• Streamline system of personal tax credits • Ensure that tax credits deliver the same amount of tax relief regardless of the taxpayer’s taxable

income • Introduce broad-based two-tier individual income tax

Corporate Income Tax

Short-Term

• Limit the use of tax exemptions and tax incentives for industrial policy• Narrow definition for small businesses by reducing turnover threshold in real terms• Make small businesses withholding agents• Eliminate withholding taxes that generate only small revenues

Medium-Term

• Make withholding taxes adjustable, especially for formal economy• Limit favorable withholding tax rates for informal economy• Strengthen rules for international tax provisions• Lower tax rate when tax base wide enough to ensure adequate revenues

General Sales Tax

Short-Term• Redraft the sales tax act to convert general sales tax into modern VAT, designed as shared

federal-provincial tax covering both goods and services and under federal administrationMedium-Term • Expand successively the base of the sales tax

Federal Excise Duties

Short-Term

• Convert the existing ad valorem rates into in rem rates for tobacco products• Index in rem rates for inflation• Employ excise duties as green tax• Bring additional luxury goods and services under excise taxation

Medium-Term• Simplify the rates structure for petroleum products• Bring federal excise legislation in line with the sales tax law

Customs Duties

Short-Term• Eliminate tariff exemptions, especially at the 6-8 digit level• Reduce tariff dispersion, especially at disaggregated level

Medium-Term• Introduce customs duties with three tariff rates for unprocessed, intermediate and processed

goods once tax base wide enough to ensure adequate revenues

Provincial TaxesShort-Term • Strengthen major provincial taxes selectively

Medium-Term • Strengthen consolidated system of provincial taxes and provide incentives for revenue effort