SA 43127 Restructuring aid to PR opening decision en...

47

Jego Ekscelencja Pan Jacek CZAPUTOWICZ Minister Spraw Zagranicznych Al. J. Ch. Szucha 23 00-580 Warszawa POLSKA Commission européenne/Europese Commissie, 1049 Bruxelles/Brussel, BELGIQUE/BELGIË - Tel. +32 22991111 EUROPEAN COMMISSION Brussels, 23.1.2018 C(2018) 205 final In the published version of this decision, some information has been omitted, pursuant to articles 30 and 31 of Council Regulation (EU) 2015/1589 of 13 July 2015 laying down detailed rules for the application of Article 108 of the Treaty on the Functioning of the European Union, concerning non-disclosure of information covered by professional secrecy. The omissions are shown thus […] PUBLIC VERSION This document is made available for information purposes only. Subject: State aid SA.43127 (2015/NN) (ex 2015/N) – Poland - Restructuring of the Polish Regional Railways Sir, The Commission wishes to inform Poland that, having examined the information supplied by your authorities on the measure referred to above, it has decided to initiate the procedure laid down in Article 108(2) of the Treaty on the Functioning of the European Union. 1. PROCEDURE (1) On 21 September 2015, Poland notified a restructuring aid for Przewozy Regionalne Sp. z o.o. ("PR") in the amount of PLN 770.3 million (c. EUR 181 million) 1 . The aid was granted on 30 September 2015 in the form of equity investment by the 100% State-owned Industrial Development Agency ("IDA"). Since the aid was granted without prior authorisation by the Commission, it breached the standstill clause laid down in Article 108(3) of the Treaty on the Functioning of the European Union ("TFEU") and Article 3 of Council 1 EUR 1 = PLN 4.25.

Transcript of SA 43127 Restructuring aid to PR opening decision en...

Jego Ekscelencja Pan Jacek CZAPUTOWICZ Minister Spraw Zagranicznych Al. J. Ch. Szucha 23 00-580 Warszawa

POLSKA Commission européenne/Europese Commissie, 1049 Bruxelles/Brussel, BELGIQUE/BELGIË - Tel. +32 22991111

EUROPEAN COMMISSION

Brussels, 23.1.2018 C(2018) 205 final

In the published version of this decision, some information has been omitted, pursuant to articles 30 and 31 of Council Regulation (EU) 2015/1589 of 13 July 2015 laying down detailed rules for the application of Article 108 of the Treaty on the Functioning of the European Union, concerning non-disclosure of information covered by professional secrecy. The omissions are shown thus […]

PUBLIC VERSION

This document is made available for information purposes only.

Subject: State aid SA.43127 (2015/NN) (ex 2015/N) – Poland - Restructuring of the Polish Regional Railways

Sir,

The Commission wishes to inform Poland that, having examined the information supplied by your authorities on the measure referred to above, it has decided to initiate the procedure laid down in Article 108(2) of the Treaty on the Functioning of the European Union.

1. PROCEDURE

(1) On 21 September 2015, Poland notified a restructuring aid for Przewozy Regionalne Sp. z o.o. ("PR") in the amount of PLN 770.3 million (c. EUR 181 million)1. The aid was granted on 30 September 2015 in the form of equity investment by the 100% State-owned Industrial Development Agency ("IDA"). Since the aid was granted without prior authorisation by the Commission, it breached the standstill clause laid down in Article 108(3) of the Treaty on the Functioning of the European Union ("TFEU") and Article 3 of Council

1 EUR 1 = PLN 4.25.

2

Regulation (EU) 2015/1589.2 Therefore, the notified measure has been registered as unlawful aid (2015/NN) and the procedural rules applicable are those laid down in Chapter III of that regulation.

(2) The Commission requested additional information on (i) 27 November 2015, (ii) 23 November 2016 and (iii) 30 June 2017, to which Poland replied on (i) 16 February 2016, 4 March 2016 and 3 June 2016, (ii) 9 January 2017 and (iii) 28 July 2017. In addition, Poland submitted information on 11 January 2017, 1 February 2017 and 20 June 2017. The Commission held meetings with Poland on 8 April 2016, 26 April 2016, 21 September 2016, 11 January 2017 and 4 July 2017.

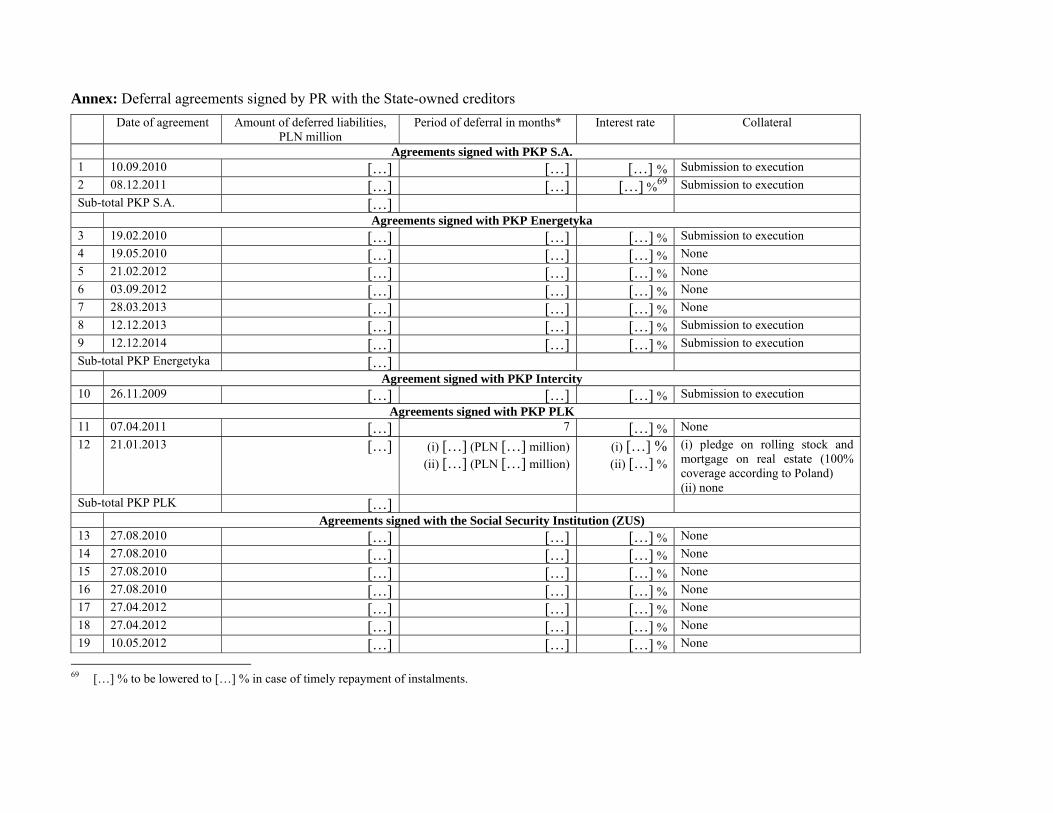

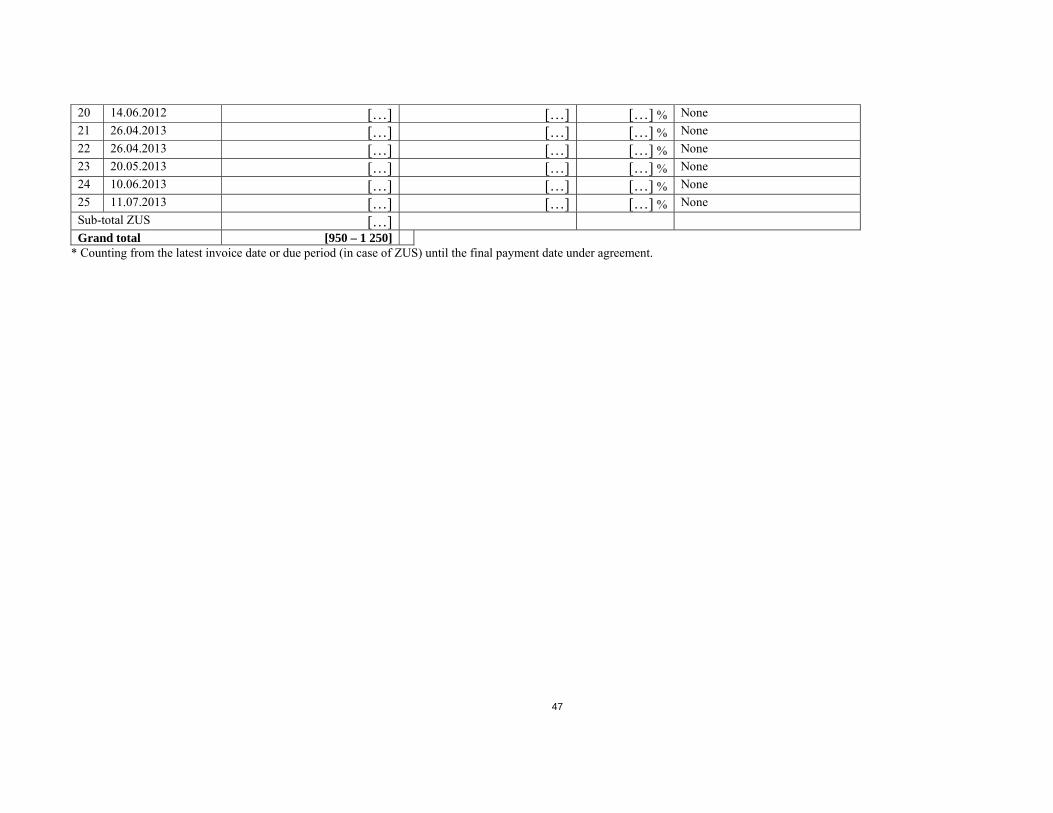

2. DESCRIPTION

2.1. Beneficiary

(3) PR is the largest passenger regional rail operator in Poland, with approximately a 27% share in the Polish market in terms of the number of passengers carried and 50% in terms of traffic volume in train/km. Based in Warsaw, PR operates in 15 out of Polish 16 regions (voivodships) and is the sole provider of public passenger regional rail transport in seven voivodships, mostly the least economically developed.

(4) PR was previously owned by 16 voivodship self-governments. As a result of granting the restructuring aid, it is currently owned by IDA, which has 50% +1 shares in PR, and by 16 voivodship self-governments. It employs approximately 9,000 people and is classified as a large enterprise. All regions in which PR operates are eligible for regional aid under Article 107(3)(a) TFEU.

(5) PR's core activity is the provision of public passenger transport services at the regional level under public service contracts concluded with voivodship self-governments and financed in the form of public service compensation. In addition, on a much smaller scale, PR provides international and "trans-border" transport services and rents and repairs rolling stock. In the past PR also provided commercial inter-regional transport services but ceased operating them in September 2015.

2.2. Competition and legal context

(6) PR's competitors include eight "internal" (so called "in-house") operators3, operating essentially within a single voivodship and owned by that voivodship's authorities (self-governments), as well as one "external" operator, Arriva RP, a subsidiary of Deutsche Bahn. The competitors of PR operate on selected routes, usually concentrated around larger cities. As a result, even in the regions where there is more than one operator, PR often has a significant share in the market.

2 Council Regulation (EU) 2015/1589 of 13 July 2015 laying down detailed rules for the application of

Article 108 of the Treaty on the Functioning of the European Union, OJ L 248 of 24.9.2015.

3 Koleje Mazowieckie, Warszawska Kolej Dojazdowa, PKP Szybka Kolej Miejska, Koleje Śląskie, Koleje Wielkopolskie, Koleje Dolnośląskie, Łódzka Kolej Aglomeracyjna, Koleje Małopolskie.

3

(7) Under Polish law public rail transport at regional level is organised by voivodships and is provided on the basis of a public service contract concluded between the organiser of such transport (voivodship self-government) and the operator. The organiser can procure transport services either by way of direct award or through a competitive tender. In practice the former has been most frequently used. In the 2016/2017 timetable, c. […]*% of traffic volume is carried out under directly awarded contracts.

(8) According to Poland, where a competitive tender was organised in the past, PR was often the only bidder. This is because the other operators considered the routes under tender as not economically attractive or, in case of the "in-house" operators, were not interested in bidding outside "their" voivodships. Apart from Arriva, no other external operator, domestic or foreign, has ever expressed interest in entering the Polish regional rail market.

(9) While some rail transport sectors (e.g. freight, international passenger) have already been liberalised at the EU level, the domestic passenger market can still be closed to competition. Under the fourth railway package4 public service contracts for public passenger transport services by rail can be directly awarded until December 2023, for a maximum duration of 10 years, i.e. until December 2033. Some Member States have already opened (part of) their markets for competition on the basis of their national law. In Poland the contracts awarded by way of a competitive tender account for c. […]% of total traffic volume scheduled in the 2016/2017 timetable.

2.3. Origins of PR's financial difficulties

(10) PR began operations in October 2001 as a result of the structural reform of the railway sector. The reform was implemented mainly on the basis of the Law of 8 September 2000 on commercialisation, restructuring and privatization of the State Enterprise Polish State Railways5 ("PKP Law"). The PKP Law transformed the former State Enterprise Polish State Railways into a joint stock company, wholly-owned by the State Treasury through PKP S.A. PKP S.A., a parent company of the newly-created PKP Group, subsequently established operating subsidiaries, including the infrastructure manager (PKP PLK) and operators

* Business secret.

4 The fourth railway package is a set of six legislative text adopted in 2016 designed to complete the single market for rail services, comprising Regulation (EU) 2016/796 of the European Parliament and of the Council of 11 May 2016 on the European Union Agency for Railways and repealing Regulation (EC) No 881/2004 (OJ L 138, 26.5.2016), Directive (EU) 2016/797 of the European Parliament and of the Council of 11 May 2016 on the interoperability of the rail system within the European Union (OJ L 138, 26.5.2016), Directive (EU) 2016/798 of the European Parliament and of the Council of 11 May 2016 on railway safety (OJ L 138, 26.5.2016), Regulation (EU) 2016/2338 of the European Parliament and of the Council of 14 December 2016 amending Regulation (EC) No 1370/2007 concerning the opening of the market for domestic passenger transport services by rail (OJ L 354, 23.12.2016), Directive (EU) 2016/2370 of the European Parliament and of the Council of 14 December 2016 amending Directive 2012/34/EU as regards the opening of the market for domestic passenger transport services by rail and the governance of the railway infrastructure (OJ L 352, 23.12.2016), Regulation (EU) 2016/2337 of the European Parliament and of the Council of 14 December 2016 repealing Regulation (EEC) No 1192/69 of the Council on common rules for the normalisation of the accounts of railway undertakings (OJ L 354, 23.12.2016).

5 Official Journal of Laws of 2000, number 84, position 984 with amendments.

4

responsible for the provision of freight and passenger transport services. Among the latter was PKP PR, a subsidiary dedicated to the provision of public regional and inter-regional rail transport services. In 2008, PKP PR was acquired by the voivodships, whereupon it changed its name to PR (further references to PR mean also its legal predecessor, PKP PR).

(11) Article 79(1) of the PKP Law provided that the financial resources should be included in the State budget for the provision of regional and inter-regional passenger rail services in the total amount of PLN 2,400 million for the years 2001-2004. At least 10% of this amount should be earmarked for the acquisition of rail vehicles necessary to provide these services. Due to the lack of sufficient budget resources this amount was subsequently reduced to PLN 900 million, of which PR actually received only PLN 532 million.

(12) In addition, on the basis of the Law of 20 June 1992 on entitlements to reduced tariffs for carriage by public transport means6, PR was entitled to receive compensation from the State budget for the loss of revenue caused by the application of the statutory reduced tariffs.7 PR actually received only part of this compensation due for years 2002 and 20038, i.e. PLN 375.5 million instead of PLN 618.4 million, leading to the outstanding balance of PLN 242.9 million.

(13) According to Poland this underfinancing led to the accumulation of financial deficit by PR, which the State reimbursed in the following years. In 2006 and 2007, it granted PR PLN 242.9 million of outstanding compensation for the loss of revenue caused by the application of statutory reduced tariffs in 2002 and 2003 and in 2008, PLN 2,160 million for the provision of transport services between 1 October 2001 and 30 April 2004. The latter amount was determined on the basis of operating losses of PR incurred in the period concerned, as explained in detail in recital (44).

(14) In addition to the financial resources described above, Article 17(1) of the PKP Law obliged PKP S.A. to contribute to its newly-established subsidiaries the assets of the former State Enterprise Polish State Railways, necessary to perform their activities. In the case of PR these assets included real estate and locomotives with a total value of PLN 318 million. Due to unresolved legal status of the assets concerned and disputes with trade unions, the transfer of assets was delayed and took place only in 2008 and 2010.

(15) In order to address the problems encountered during the implementation of the structural reform (insufficient financing, delayed transfer of assets), leading to

6 Official Journal of Laws of 1992, number 54, position 254.

7 The Law provided that certain categories of passengers were entitled to reduced tariffs and rail operators (including PR) were to receive compensation for the loss of revenue caused by the application of these tariffs. This provision was repeated and specified in (i) the Law of 27 June 1997 on the rail transport (Official Journal of Laws of 1997, number 96, position 591, later repealed) – valid until 31 May 2003 and (ii) the Law of 28 March 2003 on the rail transport (Official Journal of Laws of 2003, number 86, position 789) – valid from 31 May 2003 onwards.

8 In particular, in 2002 the State reimbursed PR 52% of lost revenue for the period February - July and 65.29% for the period August - November 2002 (PR received full compensation for January and December). In 2003, the State reimbursed 68% of lost revenue for January and February and 75% from March onwards.

5

deteriorating cash flows of PR, in March 2003 Poland amended the PKP Law9 to give the PKP Group companies (including PR) the possibility to reduce their debt burden by concluding debt restructuring agreement with creditors. Such agreements could have been concluded if approved by creditors accounting for more than 50% of total debt. On the basis of this law, on 29 March 2004, PR concluded a debt restructuring agreement with PKP PLK, which alone held more than half of PR's debt. The agreement provided for restructuring of PR's liabilities towards PKP PLK and other PKP Group companies (PKP S.A., PKP Cargo, PKP Energetyka and PKP Intercity) in the total amount of PLN 1,902 million.

(16) To complement the above-described measures taken under the structural reform of the railway sector, in December 2003, the government adopted the Programme of further restructuring and privatisation of the companies of the PKP Group until the year 2006 ("Programme until 2006"). The Programme until 2006 envisaged i.a. that in 2004 the State would provide a subsidy for the acquisition of rolling stock for regional railways operators in the amount of PLN 100 million. Again, due to budgetary constraints, PR received this subsidy with delay, on the basis of the agreement concluded with the Minister of State Treasury on 27 December 2006.

(17) Poland notified to the Commission as existing aid in force on 1 May 2004 (accession date) the measure Commercialisation, restructuring and privatisation of "Polish State Railways" (PKP) State Enterprise ("Programme PL 7/2004/TREN"). The notified measure was qualified by Poland as aid for co-ordination of transport in the meaning of Article 3(1)(d) of Regulation (EEC) No 1107/70 and consisted of the following instruments: (i) organisational restructuring; (ii) increase of capital in PKP PLK; (iii) write-off or arrangement into instalments of certain public and legal debts of PKP; (iv) State guarantee to redeem bonds issued by PKP in 2001-2004 and repay bank loans taken by PKP; (v) restructuring of certain private and legal debts of PKP Group companies and (vi) restructuring of assets.

(18) Under the interim procedure of the Accession Treaty10, aid granted by Poland to the transport sector before the EU accession on 1 May 2004 and still applicable until 30 April 2007 shall be regarded as existing aid, provided that it was communicated to the Commission within four months after the accession.11 The

9 Law of 28 March 2003 amending the PKP Law (Official Journal of Laws of 2003, number 80, position

720).

10 Treaty between the Kingdom of Belgium, the Kingdom of Denmark, the Federal Republic of Germany, the Hellenic Republic, the Kingdom of Spain, the French Republic, Ireland, the Italian Republic, the Grand Duchy of Luxembourg, the Kingdom of the Netherlands, the Republic of Austria, the Portuguese Republic, the Republic of Finland, the Kingdom of Sweden, the United Kingdom of Great Britain and Northern Ireland (Member States of the European Union) and the Czech Republic, the Republic of Estonia, the Republic of Cyprus, the Republic of Latvia, the Republic of Lithuania, the Republic of Hungary, the Republic of Malta, the Republic of Poland, the Republic of Slovenia, the Slovak Republic, concerning the accession of the Czech Republic, the Republic of Estonia, the Republic of Cyprus, the Republic of Latvia, the Republic of Lithuania, the Republic of Hungary, the Republic of Malta, the Republic of Poland, the Republic of Slovenia and the Slovak Republic to the European Union, OJ L 236, 23.9.2003.

11 Annex IV.3(4) of the Accession Treaty provides that "As regards aid to the transport sector, aid schemes and individual aid put into effect in a new Member State before the date of accession, and still applicable after that date, shall be regarded as existing aid within the meaning of Article 88(1) of the

6

measure referred to in the previous recital was notified within the framework of that procedure. As explained further (see recitals (52), (93), (99), (108)), only the transfer of assets (see recital (14)) and the acquisition of rolling stock (see recital (16)) appear to fulfil these conditions.

2.4. Current financial situation of PR

(19) Despite the measures taken under the structural reform of the railway sector and own restructuring initiatives of PR, including reduction of employment and costs and rationalisation of rolling stock, PR continued to be in a difficult financial condition. Before the notification of the restructuring aid, it had reported net losses each year since 2008 and negative equity each year since at least 2004. Sales revenue had steadily decreased and liabilities increased. PR had generated negative cash flows. Selected financial data of PR in the pre-notification period are presented in Table 1 below.

Tab. 1 Selected financial data of PR in 2011 – 2014, PLN million

2011 2012 2013 2014

Revenue 826.1 795 704.9 644.9

Net result -52.7 -44.3 -54.0 -5.5

Equity -292.4 -336.7 -390.7 -396.2

Liabilities 784.7 834.6 898 884.2

Cash flows -0.6 -3.9 -7.8 -1.3

Source: Financial statements of PR for years 2011-2014

(20) Due to the deteriorating financial situation, in particular liquidity problems, PR was not able to settle its liabilities on time. Between 2009 and 2014, it concluded 25 agreements with creditors deferring repayment of overdue liabilities in the total amount of PLN [950 – 1 250] million (the terms of these agreements are summarised in Annex 1). Despite that the total liabilities in the balance sheet kept increasing, falling only slightly in 2014. The balance of overdue liabilities alone (with interest) was forecast to reach PLN […] million as of 30 September 2015. The two biggest creditors of PR, PKP PLK and PKP Energetyka, called upon PR to repay all its liabilities towards them by 7 October 2015. The latter threatened to stop supplying energy if debt was not settled. PR was not able to repay this debt from its own resources, nor was it capable of obtaining the necessary financing on the market.

(21) It is in this context that Poland granted the notified restructuring aid to PR. On 30 September 2015, IDA acquired 50% plus one share in PR for a consideration of PLN 770.3 million. The purpose of this equity investment was to finance the

EC Treaty until the end of the third year after the date of accession, provided they are communicated to the Commission within four months of the date of accession. This provision shall be without prejudice to the procedures concerning existing aid provided for in Article 88 of the EC Treaty."

7

restructuring process, mostly the repayment of the above debt, with the ultimate goal of restoring long-term viability of PR.

2.5. Interested parties

(22) The Commission received letters from interested third parties who allege that before the notified restructuring aid PR had already received State aid, notably in the form of PLN 2,160 million ex-post compensation for services provided prior to Poland's accession to the EU. Therefore, according to the interested parties, the notified aid breaches the "one time, last time" principle of the Rescue and Restructuring Guidelines12 (the "Guidelines"), which provides that restructuring aid can be granted only once over a period of 10 years. In addition, the interested parties allege that the restructuring aid for PR is not accompanied by sufficient measures to limit distortions of competition. They also expressed concern that the planned direct award by local authorities of the five-year public service contracts to PR would foreclose the market.

(23) In line with Article 24(2) of Council Regulation (EU) 2015/1589, the Commission registered the letters from interested parties as general market information. The Commission has carefully examined their allegations and has taken them into account in the preliminary assessment below.

3. THE MEASURES UNDER ASSESSMENT

(24) Measure 1 (the notified restructuring aid): On 30 September 2015, the State-controlled IDA acquired 50% + 1 shares in PR for the consideration of PLN 770.3 million (c. EUR 181 million).

(25) Apart from the notified restructuring aid, on the basis of information submitted by Poland and by the interested parties, the Commission has identified additional potential State aid measures granted to PR in the past ("pre-restructuring measures"), as described below.

(26) Measure 2: Poland granted to PR (i) in 2008, PLN 2,160 million (c. EUR 508 million) of compensation for public transport services performed between 1 October 2001 and 30 April 2004 ("compensation for carriage") and (ii) in 2006 and 2007, PLN 242.9 million (c. EUR 57 million) of compensation for the loss of revenue caused by the application of statutory reduced tariffs in 2002 and 2003 ("compensation for reduced tariffs")13, for which, according to Poland, PR had not been sufficiently compensated in the past (together (i) and (ii) are further referred to as the "ex-post compensation").

12 Guidelines on State aid for rescuing and restructuring non-financial undertakings in difficulty, OJ C

249, 31.7.2014. All references to "the Guidelines" made in this decision mean the 2014 Guidelines, unless indicated otherwise.

13 The compensation for carriage was granted on the basis of Article 33m(1) of the Law of 25 April 2008 amending the PKP Law (Official Journal of Laws of 2008, number 97, position 624) and the agreement between PR and minister responsible for transport concluded on 23 June 2008. It was paid as follows: (i) PLN 500 million in 2 tranches – PLN 350 million until 30 June 2008 and PLN 150 million until 31 July 2008; (ii) PLN 883 million – in 4 equal monthly tranches, PLN 220.75 million each, paid from 1 August to 30 November 2008; (iii) PLN 770 million – in 6 tranches paid between 15 April and 31 October 2009. The compensation for reduced tariffs was granted on the basis of the Law of 16 December 2005 on the Railway Fund (see footnote 19) and regulations of the Minister of Finance (see footnote 21) and was paid as follows: (i) PLN 110.8 million in 2006 and (ii) PLN 132.1 million in 2007.

8

(27) Measure 3: On 29 March 2004, PR concluded a debt restructuring agreement with PKP PLK providing for the restructuring of PR's liabilities in the amount of PLN 1,902 million (c. EUR 448 million), towards the State-owned PKP Group companies (PKP PLK, PKP S.A., PKP Cargo, PKP Energetyka and PKP Intercity).14 The agreement envisaged a 40% write-off of debt and postponement of repayment of the outstanding debt balance until 31 December 2007. The agreement was modified between 2005 and 2008 with the effect that the repayment period was extended until 29 November 2009.

(28) Measure 4: Between 2009 and 2014, PR concluded 25 agreements with the State-owned creditors (PKP S.A., PKP Energetyka, PKP Intercity, PKP PLK and the Social Security Institution, or "ZUS") providing for deferral of its overdue liabilities towards these creditors in the total amount of PLN [950 – 1 250] million (c. EUR [224 - 294] million). The terms of these deferrals are summarised in Annex 1.

(29) Measure 5: PKP S.A. transferred to PR assets with a total value of PLN 318 million (c. EUR 75 million) by way of in-kind contribution in two tranches: (i) on 30 April 2008, two office buildings and 134 locomotives with related equipment with a value of PLN 48 million and (ii) on 20 July 2010, 26 real estate items (land and buildings) with a value of PLN 270 million.15

(30) Measure 6: In 2006, Poland granted PR PLN 100 million (c. EUR 24 million) of State subsidies for improving the quality of rolling stock.16

(31) Measure 7: Poland granted PR: (i) between 2006 and 2010, training aid of PLN 0.97 million (c. EUR 0.23 million); (ii) in 2012 and 2013, recruitment aid of PLN 39,000 (c. EUR 0.01 million) and (iii) between 2010 and 2015, de minimis aid of PLN 0.7 million (c. EUR 0.17 million).

4. PRELIMINARY ASSESSMENT

4.1. Existence of State aid

(32) Article 107(1) TFEU provides that any aid granted by a Member State or through State resources in any form whatsoever which distorts or threatens to distort competition by favouring certain undertakings or the production of certain goods shall, in so far as it affects trade between Member States, be incompatible with the internal market.

(33) It follows that, for a measure to be qualified as State aid within the meaning of Article 107(1) TFEU, the following cumulative criteria must be met: (i) it must be granted by the State or through State resources and must be imputable to the State; (ii) it must confer an advantage upon an undertaking; (iii) it must be selective, i.e. favour certain undertakings or the production of certain goods; and (iv) it must distort or threaten to distort competition and it must affect trade between Member States.

14 In line with amended PKP Law, it was enough for PR to conclude the agreement only with PKP PLK

because the latter held more than 50% of PR's debt (see recital (15)).

15 The contributions were made on the basis of the PKP Law (see recital (14)).

16 On the basis of the Programme until 2006 and the agreement concluded by PR with the Minister of State Treasury on 27 December 2006 (see recital (16)).

9

4.1.1. Measure 1- Equity investment by IDA (the notified restructuring aid)

(34) Poland does not dispute the classification of the measure as State aid, having itself notified it as restructuring aid.

State resources and imputability

(35) IDA is a 100% State-owned government agency. The funds for the acquisition of shares in PR were transferred to IDA by the Ministry of Infrastructure and Development from the State budget on the basis of a subsidy agreement. The measure thus clearly stems from State resources and is imputable to the State.

Selectivity

(36) The measure was granted to PR only, therefore it is selective.

Advantage

(37) It conferred an undue economic advantage on PR, since PR would not have been able to obtain such financing under normal market conditions, given its difficult financial situation.

Distortion of competition and effect on trade between Member States

(38) Although domestic passenger rail transport has not been liberalised under EU law yet, the Commission held in previous decisions concerning passenger railway companies17 that aid granted to them had an effect on competition and trade based on the fact that international passenger transport has been liberalised and that some Member States have unilaterally opened their rail passenger transport markets. In this respect it is worth noting that PR provides also international and trans-border transport services. In addition, there is inter-modal competition between regional rail and other means of transport in Poland. Furthermore, in several voivodships there is more than one regional rail operator, including a subsidiary of the company from another Member State. Therefore, the measure clearly threatens to distort competition and affects trade between Member States.

Conclusion

(39) On the basis of the above, the Commission at this stage considers that Measure 1 constitutes State aid within the meaning of Article 107(1) TFEU.

4.1.2. Measure 2 – Ex-post compensation

State resources and imputability

(40) The ex-post compensation was granted from the State budget on the basis of the Law of 25 April 2008 amending the PKP Law18 and the agreement between PR

17 Commission decision C(2017) 4047 final of 16 June 2017 on the State aid SA.32544 (2011/C)

implemented by Greece in favour of the Greek Railway Group TRAINOSE S.A., not yet published; Commission decision C(2017) 4051 final of 16 June 2017 on the State aid SA.31250 (2011/C) planned to be implemented by Bulgaria in favour of BDZ Holding EAD SA, BDZ Passenger EOOD and BDZ Cargo EOOD and other, not yet published.

18 See footnote 13.

10

and the minister responsible for transport concluded on 23 June 2008 (compensation for carriage) and on the basis of the Law of 16 December 2005 on the Railway Fund19 and regulations of the Minister of Finance (see recital (45)). Thus the measure clearly involves State resources and is imputable to the State.

Advantage

(41) As regards economic advantage, it follows from the Altmark judgment that compensation granted by the State or through State resources to undertakings as consideration for PSO imposed on them does not confer such an advantage on the undertakings concerned and hence does not constitute State aid within the meaning of Article 107(1) TFEU, provided that four cumulative conditions are satisfied20:

First, the recipient undertaking is actually required to discharge a PSO and those obligations have been clearly defined;

Second, the parameters on the basis of which the compensation is calculated have been established beforehand in an objective and transparent manner;

Third, the compensation does not exceed what is necessary to cover all or part of the costs incurred in discharging the PSO, taking into account the relevant receipts and a reasonable profit for discharging those obligations;

Fourth, where the undertaking which is to discharge a PSO is not chosen in a public procurement procedure, the level of compensation needed has been determined on the basis of an analysis of the costs which a typical undertaking, well run and adequately provided with means of transport so as to be able to meet the necessary public service requirements, would have incurred in discharging those obligations, taking into account the relevant receipts and a reasonable profit for discharging the obligation(s).

(42) As regards the first Altmark condition, Member States have a wide margin of discretion in defining a given service as a PSO. The Commission's assessment of the exercise of that discretion is limited to checking whether the Member State has made a manifest error when defining a particular service as a PSO. In this respect, the Commission observes that PR provided regional passenger rail transport services which are often unprofitable (especially in remote areas and on less frequented routes) and which are commonly not provided on a purely commercial basis but are rather co-financed by the State. In view of that it can be at least considered that Poland has not made a manifest error by classifying the services provided by PR as PSO.

(43) According to Poland this PSO was imposed on PR by the fact of its establishment on the basis of the PKP Law. It appears however that the PKP Law merely provided that PKP S.A. should establish subsidiaries that will provide passenger rail carriage and thus did not clearly define PR's PSO. In 2001-2004, PR did not conclude any contracts with the minister responsible for transport concerning the provision of the inter-regional services. It did conclude some agreements with

19 Official Journal of Laws of 2005, number 12, position 61.

20 Case C-280/00 Altmark Trans and Regierungspräsidium Magdeburg, [2003] EU:C:2003:415, paragraphs 87 and 88.

11

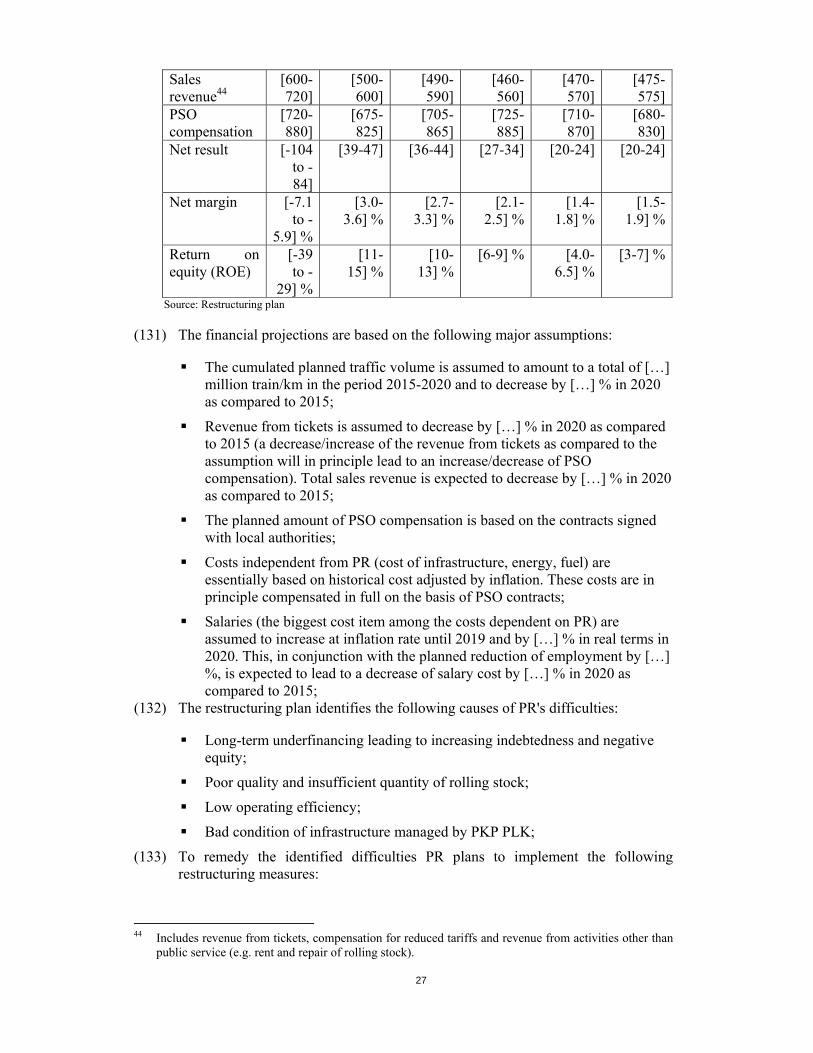

local authorities concerning the provision of regional services but these agreements had only an implementing character in relation to the source of the PSO imposed on PR, i.e. the PKP Law, and were de facto subsidy agreements (as mentioned in recital (11) regional services were financed in the form of a lump sum State subsidy whose amount was defined annually in the budget law and then was transferred to local authorities). Therefore, on the basis of information currently at the Commission's disposal, the first condition appears not to be satisfied.

(44) As regards the second Altmark condition, the Commission notes that the compensation for carriage was calculated on the basis of a difference between PR's revenue from the provision of regional and inter-regional services generated between 1 October 2001 and 30 April 2004, the associated costs and the financing actually paid in the past. The outcome of this calculation (PLN 2,718 million) was then decreased by the outstanding compensation for reduced tariffs paid in 2006 and 2007 (see recital (13)) and part of the debt written off under the debt restructuring agreement (Measure 3) in the amount of PLN 315 million. This algorithm was not established in advance and was not based on any objective and transparent parameters (such as e.g. volume of work and fee in PLN per train/km). Rather, it was determined ex-post and based on the operating losses of PR. Therefore, the second condition appears not to be met as far as the compensation for carriage is concerned.

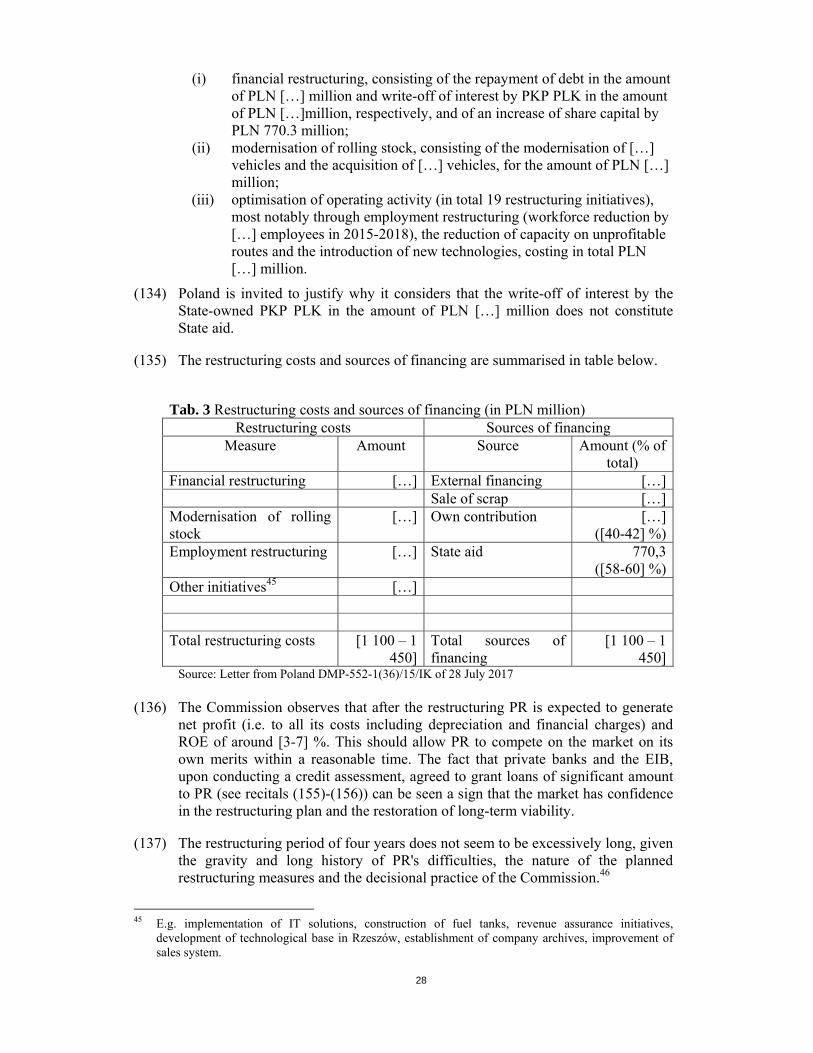

(45) When it comes to compensation for reduced tariffs, it was calculated as a difference between the compensation due and the compensation actually paid (see recital (12)). The former was established based on the parameters fixed ex-ante in the regulations issued by the Minister of Finance21, such as the number of passengers carried at different reduction rates and the amount of lost revenue adjusted by the discounted and returned tickets and value added tax. Although the compensation itself was paid ex-post, the parameters on the basis of which it was calculated were established beforehand and the amount ultimately paid was justified on the basis of these parameters. Therefore, in this case the second condition appears to be met.

(46) As regards the fourth Altmark condition, PR was not selected to provide the PSO by way of competitive, transparent, non-discriminatory and unconditional tender procedure, nor was the level of compensation (both for carriage and for reduced tariffs) determined through a benchmarking exercise. Therefore, the fourth condition appears not to be met. Since the case-law requires that all four aforementioned Altmark conditions must be cumulatively satisfied in order to exclude the presence of an advantage where compensation is granted to undertakings in consideration for PSO discharged by them, in view of the above, there is no need to assess whether the third condition was met or not. On this basis it appears that the ex-post compensation conferred an economic advantage on PR.

21 Regulation of the Minister of Finance on the subsidy for passenger rail transport of 10 June 2002

(Official Journal of Laws 2002, number 77, position 696) and amending regulations of 6 August 2002 (Official Journal of Laws 2002, number 69, position 764), 17 December 2002 (Official Journal of Laws 2002, number 128, position 1095), 21 December 2002 (Official Journal of Laws 2002, number 236, position 1984) and 29 April 2003 (Official Journal of Laws 2003, number 77, position 683).

12

Selectivity, distortion of competition and effect on trade between Member States

(47) The conclusion concerning selectivity, the distortion of competition and the effect on trade made in recitals (36) and (38) with respect to Measure 1 applies accordingly to the present measure.

Conclusion on the existence of aid

(48) On the basis of the above, the Commission is of the preliminary view that Measure 2 constitutes State aid within the meaning of Article 107(1) TFEU.

(49) Poland argues that the ex-post compensation does not constitute aid but a "compensatory payment" in relation to the outstanding and due payments for the entrusted PSOs ("PSO"), which had a character of damages. As such it did not confer any advantage on PR but reflects only compensation for damages due for the past under-compensation. Poland refers in this respect to the Asteris judgment.22

(50) The Commission notes that the Asteris judgment related to damages which Member State might be ordered to pay to individuals due to a technical error in the EU law. By contrast, the present measure concerns payment of compensation for the provision of public services in the past and not of damages. Notably, the PKP Law did not provide for any damages in case compensation is not paid on time. Thus, the Commission considers that the reference to the Asteris case law is inappropriate in view of the different nature of the measures at issue.

(51) Poland also claims that the ex-post compensation should not be assessed by the Commission as it relates to the pre-accession period and therefore constitutes existing aid.

(52) In this respect the Commission notes that the measure was not notified by Poland as existing aid. In particular, Programme PL 7/2004/TREN (see recital (17) does not provide for any compensation to be paid ex-post. Moreover, the compensation for carriage (accounting for 90% of total ex-post compensation) was granted (and paid) more than three years after EU accession, i.e. after the deadline envisaged in the interim procedure. Therefore, in the view of the Commission the measure cannot be considered as existing aid.

4.1.3. Measure 3 - Debt restructuring in 2004-2009

State resources and imputability

(53) All the creditors of the PKP Group which participated in the restructuring of PR's debt were public undertakings. The resources of public undertakings constitute State resources within the meaning of Article 107(1) TFEU because the State is

22 Judgment of the Court of 27 September 1988 in Joined Cases 106 to 120/87 Asteris EA and Others v

Hellenic Republic and European Economic Community ECLI:EU:C:1988:457, paragraph 24. The Court ruled that "Damages that the national authorities of a Member State may be ordered to pay to individuals in compensation for damage [caused by the non-payment of aid under the CAP resulting from a technical error in the Community legislation] they have caused to those individuals do not constitute aid within the meaning of Articles 92 and 93 of the Treaty".

13

capable of directing the use of these resources.23 In addition, as envisaged in the amended PKP Law (see recital (15)), the debt restructuring was initiated by the decision of the minister responsible for transport upon agreement of the minister responsible for public finance. Therefore, it was clearly imputable to the State.

Advantage

(54) According to the original debt restructuring agreement signed on 29 March 2004, 40% of the principal debt amount of PR and interest accrued until the entry into force of the agreement were to be written off, 19.18% of the principal amount was to be repaid in three equal instalments on 30 April 2004, 31 May 2004 and 30 June 2004 and the remaining balance principal amount was to be repaid in 24 monthly instalments, payable from January 2006 to December 2007. Interest accrued after the entry into force of the agreement was to be written off on the final day of the implementation of the agreement, that is to say 31 December 2007 at the latest. Finally, PR was to repay in each calendar year at least 54% of its current liabilities resulting from contracts signed with the PKP Group companies and to settle all outstanding current liabilities due from previous periods until 31 December 2007.24

(55) On 20 December 2005 and on 28 December 2006, PR signed agreement with PKP PLK which confirmed the cancellation of interest accrued in 2005 and 2006. 25 On 2 April 2007, PR signed with PKP Group companies an annex to the 2004 agreement, which envisaged notably an extension of the repayment period from 31 December 2007 until 29 November 2009. All new current liabilities were to be fully repaid as from 1 January 2008, as envisaged in the 2004 agreement. On 6 May 2008, PR signed an agreement with PKP PLK and on 29 July 2008, PR signed an agreement with PKP Cargo. These agreements confirmed the amount of liabilities owed by PR to PKP PLK and PKP Cargo as of 31 December 2007 (PLN 1,908 million) and provided for a detailed schedule of repayment until 29 November 2009. It was also agreed that interest on debt restructured under the 2004 agreement will not accrue until 29 November 2009 (under the original agreement interest was not to accrue until 31 December 2007).

23 Judgment of the Court of Justice of 16 May 2002, France v Commission (Stardust), C-482/99,

ECLI:EU:C:2002:294, paragraph 38. See also Judgment of the Court of Justice of 29 April 2004, Greece v Commission, C-278/00, ECLI:EU:C:2004:239, paragraphs 53 and 54, and Judgment of the Court of Justice of 8 May 2003, Italy and SIM 2 Multimedia SpA v Commission, Joined Cases C-328/99 and C-399/00, ECLI:EU:C:2003:252, paragraphs 33 and 34.

24 These terms of debt restructuring were applicable to the creditors from the PKP Group, accounting for 99.3% of the restructured debt amount. Debt towards other creditors was to be restructured as follows: 30% of principal amount, interest accrued until entry into force of the agreement and thereafter was to be written off and 70% of principal amount was to be repaid in 28 monthly instalments, starting one year after the entry into force of the agreement. From the information provided by Poland it appears that the original terms of debt restructuring towards these creditors (not belonging to the PKP Group) agreed in 2004 were not subsequently modified.

25 There were interpretation differences between PR and PKP PLK as regards provisions of the 2004 agreement concerning interest accrued after its entry into force. Finally, the parties confirmed the original interpretation according to which the 2004 agreement provided for write-off of all interest, including interest accrued from entry into force of the 2004 agreement until its final settlement.

14

(56) As regards the original debt restructuring agreement, considered on a stand-alone basis (i.e. without the subsequent modifications), there is no need to assess whether it conferred an economic advantage on PR, because it had been signed more than 10 years before the notification of the present restructuring aid, i.e. beyond the limitation period for the recovery of aid by the Commission laid down in Article 17 of Council Regulation (EU) 2015/1589.

(57) When it comes to the subsequent modifications described above, in order to determine whether they conferred an economic advantage on PR, the Commission must establish whether by agreeing to postpone the repayment of debt on the agreed terms the creditors of PR behaved in a way comparable to that of a private creditor in a similar situation (the so called market economy creditor principle, or "MECP"). The Commission's assessment focuses on the transaction from the perspective of the hypothetical prudent private creditor26.

(58) A rational private creditor would have normally compared the financial outcome of contemplated courses of action, i.e. (i) the extension of debt repayment period agreement and (ii) the enforcement of the original debt restructuring agreement, in order to choose the one ensuring the higher expected recovery amount.

(59) In the present case Poland has not provided any evidence or arguments demonstrating that the creditors of PR performed any such comparative analysis, nor that the chosen course of action, i.e. modification of the original debt restructuring agreement, ensured the highest expected debt recovery. On the contrary, Poland considers the whole measure (i.e. both the original debt restructuring agreement and its subsequent modifications) to constitute State aid (see recital (65)) and thereby implies that it conferred an economic advantage on PR.

(60) The Commission notes that the modification of the original debt restructuring agreement described in recital (55), in particular those made in 2007 and 2008, effectively consist in a 23-month interest free postponement of repayment of liabilities owed by PR to the PKP Group companies (as compared to the terms of the debt restructuring agreement signed in 2004) in the amount of at least PLN 1,908 million.27 Such interest-free postponement of the repayment period by almost two years relieved PR from meeting its payment obligations according to the original schedule agreed in 2004 and thus provided PR with additional liquidity which could have been used to finance PR's operations. PR would arguably not have been able to raise such interest-free liquidity on the market from private creditors even if it was in a very good financial situation, let alone as a company in financial difficulties. In the past the Commission concluded that similar interest-free postponement of the repayment of debt constituted aid.28

26 Case C-300/16P Commission v Frucona Košice, ECLI:EU:C:2017:706, paragraph 28. 27 This is the amount of liabilities owed to PKP PLK and PKP Cargo as of 31 December 2007, as

confirmed by the agreements signed on 6 May 2008 and 29 July 2008, respectively. This amount does not include liabilities owed by PR to the remaining PKP Group companies (PKP S.A., PKP Intercity and PKP Energetyka) participating in the original debt restructuring agreement, whose repayment was also postponed (by the annex of 2 April 2007), as Poland did not provide the relevant amount.

28 Commission Decision of 9 July 2014 in case SA.38324 Restructuring aid for Alestis, OJ C 418, 21.11.2014, p. 1, rec. 38-39.

15

(61) In view of the above, the Commission at this stage considers that the measure does not comply with the MECP and therefore conferred an economic advantage on PR. If there is evidence to the contrary, Poland and any interested parties are invited to provide comments on the existence of aid and any available contemporaneous evidence (e.g. internal analyses by the creditors, reports prepared by external consultants) demonstrating that the decision to postpone the repayment of debt, as agreed in 2007 and 2008, was more beneficial to the creditors than the alternative scenario of enforcing the repayment according to the original schedule, agreed in 2004.

Selectivity, distortion of competition and effect on trade between Member States

(62) The conclusion concerning selectivity, the distortion of competition and the effect on trade made in recitals (36) and (38) with respect to Measure 1 applies accordingly to the present measure.

Conclusion

(63) On the basis of the above, the Commission at this stage considers that Measure 3 constitutes State aid within the meaning of Article 107(1) TFEU.

(64) The Commission considers at this stage that the aid amount can be determined e.g. as a difference between the NPV of the debt calculated according to the original repayment schedule (i.e. agreed on 29 March 2004) and the NPV of the debt calculated according to the new repayment schedule, as modified in 2007 and 2008, i.e. assuming the postponement of debt repayment by 23 months without interest, discounted at an appropriate discount rate. Commission does not have enough information, in particular the precise repayment schedules and information on collateral securing the restructured liabilities, to calculate the exact aid amount. On the basis of available information the aid amount can be roughly approximated to PLN 173-260 million (EUR 41-61 million) assuming the application of discount rates according to the Reference Rate Communication29 for companies in difficulty with high (lower range of the estimated aid amount) and low (higher range) level of collateral.

(65) Poland argues that the measure "fits into the objective of the structural reform of the railway sector" and was notified as existing aid under the interim procedure. Poland claims that subsequent modifications resulted directly from the implementation of the original debt restructuring agreement of 2004 and did not in principle deviate from the original framework. Therefore the measure should be considered as existing aid.

(66) As noted in recital (55) the original debt restructuring agreement signed on 29 March 2004, was subsequently modified by annexes and agreements signed between 2005 and 2008. In view of that the Commission must assess whether these subsequent modifications were indeed only a mere implementation of the original debt restructuring agreement and did not change its main parameters, as claimed by Poland, or whether they were of such a nature that they should rather be considered as new aid.

29 Communication from the Commission on the revision of the method for setting the reference and

discount rates, OJ C 14/6, 19.1.2008.

16

(67) The Commission considers that modifications affecting the main parameters of the original debt agreement, such as e.g. interest rate, repayment period or debt amount, should be viewed as amounting to an alteration of existing aid. In this respect the Commission notes firstly that these modifications changed the duration of debt restructuring from 45 to 68 months. Secondly, they lowered the real amount of PR's debt. This is because the longer the repayment period, all other factors constant, the lower the net present value ("NPV") of debt liabilities to be repaid. On this basis the Commission is of the opinion that the annexes and agreements signed between 2005 and 2008 entailed a significant modification of the original debt restructuring agreement as they changed its main parameters in favour of PR and therefore, the subsequent modifications of the original debt restructuring agreement must be considered as new aid.

4.1.4. Measure 4 - Deferral of liabilities in 2009-2014

(68) Poland argues that the deferral agreements signed with the State-owned creditors do not constitute aid because they were granted on market terms. Firstly, Poland claims that PR was an important customer of PKP PLK and PKP Energetyka, therefore these creditors had particular interest in continuing their business relations with PR despite delayed repayment of liabilities. In addition, they granted deferrals to PR on terms comparable to those offered to other creditors. Secondly, taking into account the average duration of execution of debt in Poland as well as the average recovery rates from insolvent debtors30, deferrals can be considered to be more favourable to creditors than the alternative scenario of PR's insolvency. This was also demonstrated by an ex-post NPV analysis made by Poland. Thirdly, the interest rates were set at levels comparable to the average interest rates charged in the non-financial sector in Poland. Fourthly, the risk for creditors was limited by the expectation that PR will continue to receive PSO compensation. Finally, the late payment of liabilities would be a common market practice in Poland, where only 23% of payments were made on time and 57.8% of payments were at least 30 days overdue in 2012.

State resources and imputability

(69) First of all, the Commission observes that all the creditors who signed deferral agreements with PR were either State-owned undertakings or a public institution (ZUS).

(70) As regards ZUS, it is part of public administration, under full supervision by the State and is financed from the State budget. Therefore there is no doubt that its decisions to defer PR's liabilities are imputable to the State and that these deferrals involve State resources.

(71) As regards the remaining creditors, as mentioned in recital (53), resources of public undertakings constitute State resources within the meaning of Article 107(1) TFEU. Because the deferrals involve a potential loss of resources by these creditors, they must be considered as involving State resources.

30 According to Poland (i) the average time to execute receivables in Poland according to the World

Bank – 830 days in 2008-2012 and 685 days in 2013-2016; (ii) the average recovery rate from insolvent debtors in Poland according to the World Bank – 34.1% in 2009 and 2010, 35.8% in 2011, 31.5% in 2012, 54.5% in 2013, 54.8% in 2014, 57.0% in 2015 and 58.3% in 2016.

17

(72) Considering imputability, the Commission notes that in 2009-2014, PKP S.A., PKP Intercity, PKP PLK and PKP Energetyka all belonged to the PKP Group which is 100% owned by the State and is supervised by the minister responsible for transport. Although the mere fact that a measure is taken by a public undertaking is not per se sufficient to consider it imputable to the State, the imputability may be inferred from a set of indicators arising from the circumstances of the case and the context in which the measure was taken.31 These indicators include e.g. the nature of its activities and the exercise of the latter on the market in normal conditions of competition with private operators, the degree of the supervision exercised by the public authorities over the management of an undertaking and whether an undertaking could autonomously take a decision in question or any other indicator showing the involvement of the public authorities in adopting the measure in question or the unlikelihood of their not being involved, taking account of the scope of the measure, its content or the conditions it contains.

(73) In this respect, the Commission observes that PR provides public transport services which are not exercised in normal market conditions, but are largely directly procured and financed by the State. Also the creditors, at least PKP PLK (the monopolist infrastructure manager) and PKP Intercity (to the extent it provided public inter-regional services), did not compete in normal market conditions with private operators. Moreover, insolvency of PR, the only provider of regional rail transport in almost half of the regions, could have led to serious disruption in the provision of important public service. Therefore, the State had particular interest in ensuring the liquidity of PR.

(74) The State has traditionally exercised a high degree of supervision over the management and activities of the PKP Group companies, not least through its influence on selection of their boards of directors and management boards, whose composition often fluctuated in coincidence with changes in the political scene. In addition, in the past the PKP Group companies were not always autonomous in taking important business decisions. For example, the State was directly involved in structural reorganization of the railway sector, transfer of assets among the PKP Group companies or financial restructuring. Most notably, the State initiated the restructuring of PR's debt (Measure 3), which included the same creditors who later agreed to defer PR's liabilities. This is not surprising, given that the PKP Group is one of the largest employers in Poland (the creditors concerned employed more than 50,000 people in 2014) and plays an important role in shaping transport policy of the State.

(75) Finally, taking into account the scope of the measure (the amount of deferred liabilities accounted for approximately [>120] % of PR's average annual revenue in the period concerned), its impact on the creditors (PR was the third biggest customer of PKP PLK and PKP Energetyka), the strong organisational links between the debtor, the creditors and the State and, last but not least, the apparently non-market conditions on which the deferrals were granted (see below), it seems unlikely that the decisions of the public undertakings concerned to defer liabilities of PR could have been taken without any involvement whatsoever of the State.

31 Judgment of the Court of Justice of 16 May 2002, France v Commission (Stardust), C-482/99,

ECLI:EU:C:2002:294, paragraph 55.

18

(76) On the basis of the above, the Commission is of the opinion that the public authorities can be considered as having been involved in one way or another in the decisions to defer PR's liabilities. Poland itself does not argue that the measure is not imputable to the State. On this basis, the Commission is of the preliminary view that the measure imputable to the State.

Advantage

(77) In order to determine whether the measure conferred an economic advantage on PR, the Commission must establish whether by agreeing to defer liabilities of PR the creditors behaved in a way comparable to that of a private creditor in a similar situation. In this respect, the Commission has found what follows.

(78) As a matter of fact, between 2009 and 2014, four State-owned undertakings and ZUS concluded with PR, a company in difficult financial situation and also owned by the State, 25 agreements to defer repayment of overdue liabilities in the total amount of PLN [950 – 1 250] million, accounting, as mentioned above, for approximately [>120] % of PR's average annual revenue in this period.

(79) Poland has not submitted any contemporaneous evidence demonstrating that the decision to defer liabilities on the agreed terms was more favourable to the creditors than alternative courses of action, such as e.g. execution of debt. The ex-post NPV analysis made by Poland cannot be considered as sufficiently reliable evidence because it is not independent (the State is an interested party as the owner of the debtor and the creditors) and, more importantly, it was prepared ex-post, i.e. after the decisions to defer liabilities were taken. A rational market creditor would have assessed different scenarios before taking a decision to defer liabilities, with the aim to choose the one that would have guaranteed the highest expected recovery rate.

(80) Moreover, the terms on which the deferrals were granted (see Annex 1) appear rather favourable, taking into account the poor financial condition of the debtor. More concretely, the deferral periods were long, ranging from six to 21 months, and in case of one agreement concluded with PKP PLK, this period amounted to […] months, that is to say, much longer than the average period of the execution of debt from an insolvent debtor, as claimed by Poland (see footnote 30). Notably, this agreement accounted for […] % of the total deferred liabilities concerned.32 In addition, the interest rates applied by the creditors were low if compared to the plausible benchmark, such as the proxy market rates resulting from the application of the Reference Rate Communication ("reference rate").33 In particular, under all the agreements the interest rates applied were lower than the reference rate applicable to a company in difficulty, such as PR.34 Even if assumed, as claimed by

32 The shares of liabilities provided in this recital have been calculated by the Commission on the basis of

information provided by Poland.

33 Communication from the Commission on the revision of the method for setting the reference and discount rates, OJ C 14/6, 19.1.2008.

34 The reference rate is established assuming "low" collateral for all agreements (submission to execution or no collateral at all) except from one agreement with PKP PLK of 2013 where collateral might be considered as "high" (pledge on rolling stock covering, according to Poland, 100% of secured liability amount).

19

Poland, that PR merited a rating "B" (weak) in 2009-2013 and CCC (bad/financial difficulties) from 2014 onwards, the interest rates actually applied were lower than the corresponding reference rates under as many as 18 agreements, accounting for […] % of total deferred liabilities. Moreover, under six agreements (accounting for […] % of total deferred liabilities) the interest rates were even lower than the reference rate applicable to an AAA (strong)-rated company. Finally, the collateral was weak under all but one agreement (see footnote 34) and consisted merely in the submission to execution.35 Under 18 agreements (accounting for […] % of total deferred liabilities) there was no collateral at all.

(81) Poland argues that PR was an important customer of PKP PLK and PKP Energetyka, therefore these creditors had a particular interest in continuing their business relations with PR. Indeed, as mentioned above, PR was the third biggest customer of PKP PLK and PKP Energetyka during the period concerned, accounting for an average of […] % and […] % of their revenue, respectively. This can be one of the factors that a private creditor would have taken into account, but it is not per se sufficient to justify market-conformity of the deferrals on the agreed terms. In any case, this argument does not apply to the remaining creditors, for whom PR was not such an important customer.

(82) The argument of Poland that PKP PLK and PKP Energetyka concluded similar deferral agreements with other business partners is not sufficient evidence of market-conformity of their agreements with PR. Without knowing the precise conditions of these agreements and the financial situation of the debtors, it cannot be excluded that these deferrals were also not granted on market terms. In any case, what is clear is that these deferrals involved smaller amounts of liabilities and shorter repayment periods. In any event, in order to argue market-conformity, Poland would rather have to demonstrate that private creditors have or would have granted deferrals to PR on similar terms as the public creditors concerned. In this respect, the Commission notes that PR did actually sign deferral agreements with two private creditors. Nevertheless, these agreements do not seem to demonstrate market-conformity either, since they involved smaller amount of liabilities and, crucially, envisaged a combination of higher interest rate and shorter repayment periods than the deferral agreements signed by PR with PKP Group companies and ZUS.

(83) Poland argues that the interest rates applied in the deferral agreements were set at levels comparable with the average interest rates charged in the non-financial sector in Poland36. This does not however suffice to justify that they were market-conform, because the average debtor in the non-financial sector could have been in a better financial condition and/or could have offered a better collateral, and thus could have had higher credit worthiness than PR. Likewise, the argument that late payment of liabilities is allegedly a common market practice in Poland does not prove that the terms of the deferral agreements were market-conform.

35 Submission to execution, provided for in article 777 of the Civil Proceedings Code, is a popular form

of the collateral in Poland which enables a creditor to initiate the execution without the necessity to open court proceedings and to substantiate the creditor's rights. The court has three days to validate a registered claim of a creditor, upon which the creditor can ask a bailiff to implement the execution.

36 According to the National Bank of Poland the average interest rate on enterprise loans with maturity of up to one year was 6.5% in 2009, 6.2% in 2010 and 2011, 6.4% in 2012, 5.0% in 2013 and 4.3% in 2014.

20

(84) Finally, the argument of Poland that the risk for creditors was limited by the expectation that PR will continue to receive PSO compensation is disputable, given that such compensation must be used to finance PSO services and not to repay overdue liabilities. In addition, it does not justify the particular terms on which the deferral agreements were concluded. Therefore, the Commission considers that the measure conferred an economic advantage on PR.

Selectivity, distortion of competition and effect on trade between Member States

(85) The conclusion concerning selectivity, the distortion of competition and the effect on trade made in recitals (36) and (38) with respect to Measure 1 applies accordingly to the present measure.

Conclusion

(86) On the basis of the above, it is the Commission's preliminary view that Measure 4 constitutes State aid within the meaning of Article 107(1) TFEU.

4.1.5. Measure 5 - Contribution of assets in 2008 and 2010

State resources and imputability

(87) The assets were contributed to PR by PKP S.A., a public undertaking 100% owned by the State. As mentioned in recital (53), resources of public undertakings constitute State resources within the meaning of Article 107(1) TFEU. The contributions were made on the basis of the PKP Law (see recital (14)), therefore they are clearly imputable to the State. Poland does not contest it.

Advantage

(88) The measure conferred an undue economic advantage, as no rational market vendor would have supplied assets to PR free of charge.

Selectivity, distortion of competition and effect on trade between Member States

(89) The conclusion concerning selectivity, the distortion of competition and the effect on trade made in recitals (36) and (38) with respect to Measure 1 applies accordingly to the present measure.

Conclusion

(90) The measure appears to fulfil all the criteria of State aid under Article 107(1) TFEU. Nevertheless, the Commission observes that it was notified by Poland as existing aid under the interim procedure. In particular, the programme PL 7/2004/TREN (see recital (17)) clearly includes the measure consisting in the contribution by PKP S.A. to its newly-created subsidiaries of the assets, necessary to carry out the latter's activities. In addition, although the actual transfer of assets to PR formally took place only in 2008 and 2010, i.e. more than three years after accession, it was a mere implementation of the provisions of the PKP Law of 2000.

(91) According to Article 17(1) of the PKP Law, PKP S.A. was obliged to supply its subsidiaries with the assets necessary to carry out their activities. Poland demonstrated that the assets ultimately transferred to PR were indeed necessary to

21

carry out PR's activities and were actually used by PR long before the formal transfer took place.

(92) In particular, two buildings transferred in 2008 had been rented by PR from PKP S.A. already since 2001 and 2005, while the locomotives transferred in the same year were previously used by PR on the basis of agreements signed with PKP Cargo (after the establishment of the PKP Group all locomotives and associated staff were initially allocated to PKP Cargo with the task to provide traction services to the whole PKP Group). As regards the buildings transferred in 2010, the vast majority of them was included in the business plan of PR in 2001 and all of them had been rented by PR from PKP S.A. since 2001.37

(93) On the basis of the above, the Commission concludes that Measure 5 constitutes existing aid under the interim procedure.

(94) Without prejudice to the previous recital, the measure can also be seen as a mere reallocation of assets within the newly-created PKP Group. The subsidiaries of PKP Group, including PR, continued to perform the same operations with essentially the same assets as the former State Enterprise Polish State Railways, their predecessor. PKP S.A., the mother company of the new PKP Group, was legally obliged to distribute these assets among its subsidiaries, which de facto used them from their establishment. Thus the reallocation was in substance only a legal and accounting operation which did not confer any real economic advantage on PR.

4.1.6. Measure 6 - State subsidy for rolling stock in 2006

State resource and imputability

(95) The measure was granted by the State on the basis of the Programme until 2006 and the agreement concluded with the Minister of State Treasury on 27 December 2006 (see recital (16)). Therefore it clearly involves State resources and is imputable to the State. Poland does not dispute that.

Advantage

(96) The measure conferred an undue economic advantage, as no rational market investor would have provided a non-repayable grant to PR.

Selectivity, distortion of competition and effect on trade between Member States

(97) The conclusion concerning selectivity, the distortion of competition and the effect on trade made in recitals (36) and (38) with respect to Measure 1 applies accordingly to the present measure.

Conclusion

(98) The measure appears to fulfil all the criteria of State aid under Article 107(1) TFEU. Nevertheless, the Commission notes that it was notified to the Commission as existing aid under the interim procedure. The programme PL 7/2004/TREN (see

37 Except from one building in Wroclaw (regional headquarters of PR), for which PKP S.A. cancelled

rent agreement (due to reconstruction of the railway station) and instead transferred to PR a replacement building.

22

recital (17) explicitly provides for the purchase and modernisation of rolling stock. The subsidy was granted on the basis of the Programme until 2006 adopted on 16 December 2003 (i.e. before accession) by which the government committed to grant financial support to PR in the amount of PLN 100 million for improving the quality of rolling stock used for regional carriage. Finally, the subsidy was paid based on the agreement, which was signed less than three years after EU accession, i.e. within the deadline envisaged under the interim procedure.

(99) On the basis of the above, the Commission concludes that Measure 6 constitutes existing aid under the interim procedure.

4.1.7. Measure 7 - Training, recruitment and de minimis aid in 2006-2015

(100) Poland does not contest the qualification of the measure as aid.

State resources and imputability

(101) The measure was granted by public authorities, such as the Polish Agency for Enterprise Development, Labour Office and the State Fund for Rehabilitation of the Disabled. It therefore clearly involves State resources and is imputable to the State.

Advantage

(102) It was granted to PR only and on terms that PR, being in a difficult financial condition, would not have received on the market. The measure therefore conferred on PR an undue economic advantage.

Selectivity

(103) The conclusion concerning selectivity made in recital (36) with respect to Measure 1 applies accordingly to the present measure.

Distortion of competition and effect on trade between Member States

(104) Regulation (EU) 1407/201338 ("de minimis Regulation") provides that aid granted to a single undertaking shall be deemed not to meet all the criteria of Article 107(1) TFEU if the total amount of such aid does not exceed EUR 200,000 over any period of three fiscal years. As recital (3) of that regulation explains, aid granted to a single undertaking not exceeding that threshold should be deemed not to have any effect on trade between Member States and not to distort or threaten to distort competition. That provision also applies to aid granted prior to the entry into force of the de minimis Regulation (i.e. 1 January 2014), pursuant to Article 7(1) thereof.

(105) Based on the information received from Poland the aid granted to PR under Measure 7 exceeded the de minimis threshold in the period from 2009 to 2011, when it amounted in total to PLN 1 177 421 (c. EUR 277 040). Since this amount exceeds the de minimis threshold, and for the same reasons as set out in recital (38) with respect to Measure 1, the measure distorted or threatened to distort competition and had an effect on trade between the Member States.

38 Commission Regulation (EU) 1407/2013 of 18 December 2013 on the application of Articles 107 and

108 of the Treaty on the Functioning of the European Union to de minimis aid, OJ L 352/1 of 24.12.2013.

23

Conclusion

(106) On the basis of the above, the Commission at this stage considers that Measure 7 constitutes State aid within the meaning of Article 107(1) TFEU.

(107) Poland is invited to explain what was the legal basis for aid granted under Measure 7, e.g. whether it was granted under an authorised scheme or block-exempted.

4.1.8. Overall conclusion on the existence of State aid

(108) On the basis of the assessment made in Section 4.1 above the Commission is of the preliminary view that Measures 1, 2, 3, 4 and 7 constitute aid within the meaning of Article 107(1) TFEU. As regards Measures 5 and 6, the Commission concludes that they constitute existing aid.

4.2. Legality of the aid

(109) Pursuant to Article 108(3) TFEU, Member States must notify any plans to grant or alter aid, and must not put the proposed measures into effect until the notification procedure has resulted in a final decision. Article 3 of Council Regulation (EU) 2015/1589 provides that aid shall not be put into effect before the Commission has taken, or is deemed to have taken, a decision authorising such aid.

(110) In so far as the ex-post compensation may constitute State aid, the Commission must first assess whether such aid could qualify for the exemption from the notification obligation under Regulation (EEC) No 1191/69.39

(111) According to Article 17(2) of Regulation (EEC) No 1191/69, compensation paid pursuant to the Regulation is exempted from the preliminary information procedure laid down in Article 108(3) TFEU and thus from prior notification. It follows from the Combus judgment that the concept of ‘public service compensation’ within the meaning of that provision must be interpreted in a very narrow manner40. The exemption from notification provided by Article 17(2) covers only compensation for PSO imposed unilaterally on an undertaking, pursuant to Article 2 of that Regulation, which is calculated using the method described in Articles 10 to 13 of that Regulation (the common compensation procedure), and not to public service contracts as defined by Article 14.

(112) The question of whether Article 17(2) indeed dispensed Poland from prior notification in the present case therefore depends, first, on whether a PSO was in fact unilaterally imposed on PR by Poland and, second, on whether the compensation paid pursuant to that obligation complies with Regulation (EEC) No 1191/69.

(113) As mentioned in recital (43), the PSO was imposed on PR by the fact of its establishment on the basis of the PKP Law. In 2001-2004, PR did not conclude

39 Regulation (EEC) No 1191/69 of 26 June 1969 on action by Member States concerning the obligations

inherent in the concept of a public service in transport by rail, road and inland waterway, OJ L 156, 28.6.1969, p. 1.

40 Case T-157/01 Danske Busvognmænd [2004] ECR II-917, paragraphs 77 to 79.

24

any contracts with the minister responsible for transport to provide inter-regional services. It did conclude agreements with local authorities to provide regional services but these agreements were a mere implementation of the PKP Law. Likewise, the obligation to respect statutory reduced tariffs was imposed on PR on the basis of the Law of 20 June 1992 on entitlements to reduced tariffs for carriage by public transport means (see footnote 7). On this basis, the Commission considers that the obligation to carry out the services for which ex-post compensation was paid was unilaterally imposed on PR.

(114) In order to be exempted from prior notification under Article 17(2) of Regulation (EEC) No 1191/69, any compensation would still need to comply with the common compensation procedures set out in Section IV thereof.

(115) Article 10 of Regulation (EEC) No 1191/69 provides, inter alia, that the amount of the compensation must, in the case of an obligation to operate or to carry, be equal to the difference between the reduction in financial burden and the reduction in revenue of the undertaking if the whole or the relevant part of the obligation in question were terminated for the period of time under consideration. Article 11 provides a detailed formula on how compensation should be established in the case of tariff obligations. Poland has not demonstrated that the ex-post compensation was calculated according to Article 10 and Article 11 and is invited to do so.

(116) According to case law and Regulation (EEC) No 1191/6941, transport undertakings must keep separate accounts for activities subject to PSO and for other activities. In this respect, Poland confirmed that the accounting system of PR consisted of separate accounts for cost and revenues related to PSO and other activities.

(117) Article 13 of Regulation (EEC) No 1191/69 requires that the amount of the compensation should be fixed in advance. As argued in recital (44), the compensation for carriage was fixed ex-post and was not based on any ex-ante parameters. As regards the compensation for reduced tariffs, it was determined ex-ante (see recital (45)).

(118) Therefore, it is the Commission's preliminary view that the ex-post compensation was not exempted from compulsory prior notification pursuant to Article 17(2) of Regulation (EEC) No 1191/69.

(119) The other measures, considered at this stage as aid, do not appear to be exempted from the notification obligation either.

41 According to the Court of Justice in the Antrop judgment, the requirement set out in Article 10 of