経済の数理解析 - Keio Universityweb.econ.keio.ac.jp/staff/maruyama/rcme/prog+abst06.pdf ·...

23

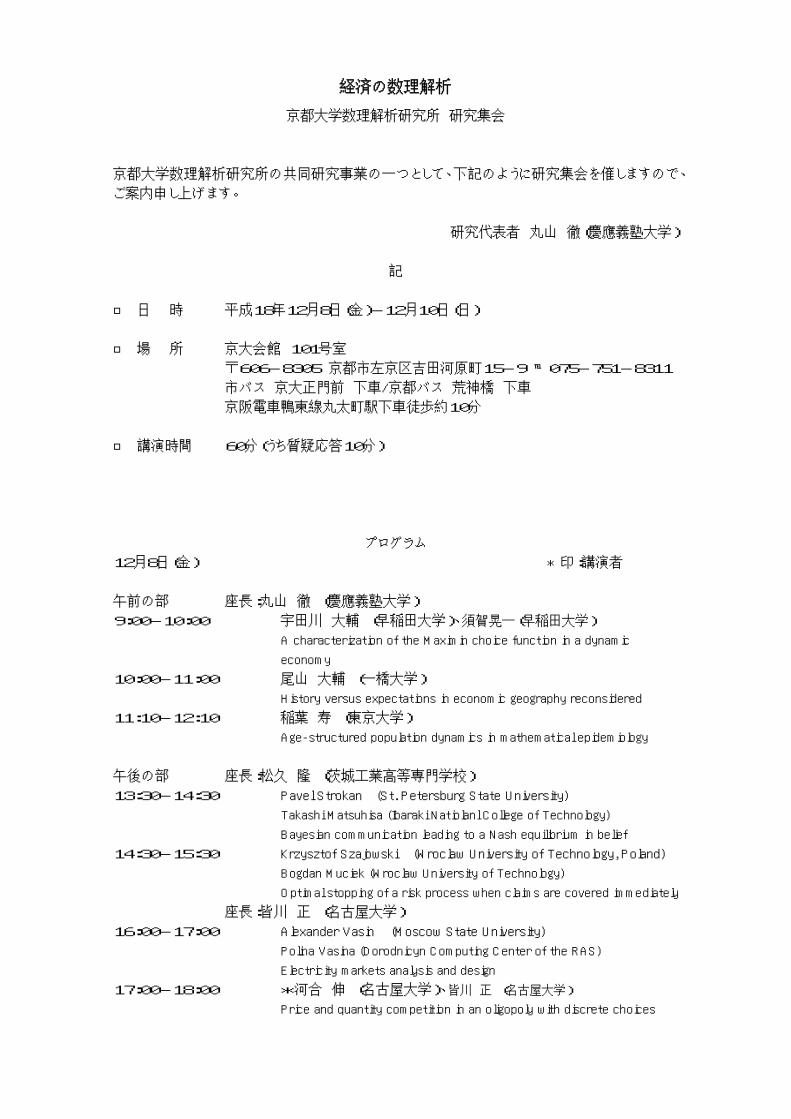

経済の数理解析 京都大学数理解析研究所 研究集会 京都大学数理解析研究所の共同研究事業の一つとして、下記のように研究集会を催しますので、 ご案内申し上げます。 研究代表者 丸山 徹(慶應義塾大学) 記 □ 日 時 平成18年12月8日(金)-12月10日(日) □ 場 所 京大会館 101号室 〒606-8305 京都市左京区吉田河原町15-9 ℡075-751-8311 市バス 京大正門前 下車/京都バス 荒神橋 下車 京阪電車鴨東線丸太町駅下車徒歩約10分 □ 講演時間 60分(うち質疑応答10分) プログラム 12月8日(金) * 印:講演者 午前の部 座長:丸山 徹 (慶應義塾大学) 9:00-10:00 宇田川 大輔 (早稲田大学)、須賀晃一(早稲田大学) A characterization of the Maximin choice function in a dynamic economy 10:00-11:00 尾山 大輔 (一橋大学) History versus expectations in economic geography reconsidered 11:10-12:10 稲葉 寿 (東京大学) Age-structured population dynamics in mathematical epidemiology 午後の部 座長:松久 隆 (茨城工業高等専門学校) 13:30-14:30 Pavel Strokan (St. Petersburg State University) Takashi Matsuhisa (Ibaraki Natiolanl College of Technology) Bayesian communication leading to a Nash equilibrium in belief 14:30-15:30 Krzysztof Szajowski (Wroclaw University of Technology, Poland) Bogdan Muciek (Wroclaw University of Technology) Optimal stopping of a risk process when claims are covered immediately 座長:皆川 正 (名古屋大学) 16:00-17:00 Alexander Vasin (Moscow State University) Polina Vasina (Dorodnicyn Computing Center of the RAS) Electricity markets analysis and design 17:00-18:00 *河合 伸 (名古屋大学)、皆川 正 (名古屋大学) Price and quantity competition in an oligopoly with discrete choices

Transcript of 経済の数理解析 - Keio Universityweb.econ.keio.ac.jp/staff/maruyama/rcme/prog+abst06.pdf ·...

経済の数理解析

京都大学数理解析研究所 研究集会

京都大学数理解析研究所の共同研究事業の一つとして、下記のように研究集会を催しますので、

ご案内申し上げます。

研究代表者 丸山 徹(慶應義塾大学)

記

日 時 平成18年12月8日(金)-12月10日(日)

場 所 京大会館 101号室

606-8305 京都市左京区吉田河原町15-9 075-751-8311

市バス 京大正門前 下車/京都バス 荒神橋 下車

京阪電車鴨東線丸太町駅下車徒歩約10分

講演時間 60分(うち質疑応答10分)

プログラム

12月8日(金) * 印:講演者

午前の部 座長:丸山 徹 (慶應義塾大学)

9:00-10:00 宇田川 大輔 (早稲田大学)、須賀晃一(早稲田大学)

A characterization of the Maximin choice function in a dynamic

economy

10:00-11:00 尾山 大輔 (一橋大学)

History versus expectations in economic geography reconsidered

11:10-12:10 稲葉 寿 (東京大学)

Age-structured population dynamics in mathematical epidemiology

午後の部 座長:松久 隆 (茨城工業高等専門学校)

13:30-14:30 Pavel Strokan (St. Petersburg State University)

Takashi Matsuhisa (Ibaraki Natiolanl College of Technology)

Bayesian communication leading to a Nash equilibrium in belief

14:30-15:30 Krzysztof Szajowski (Wroclaw University of Technology, Poland)

Bogdan Muciek (Wroclaw University of Technology)

Optimal stopping of a risk process when claims are covered immediately

座長:皆川 正 (名古屋大学)

16:00-17:00 Alexander Vasin (Moscow State University)

Polina Vasina (Dorodnicyn Computing Center of the RAS)

Electricity markets analysis and design

17:00-18:00 *河合 伸 (名古屋大学)、皆川 正 (名古屋大学)

Price and quantity competition in an oligopoly with discrete choices

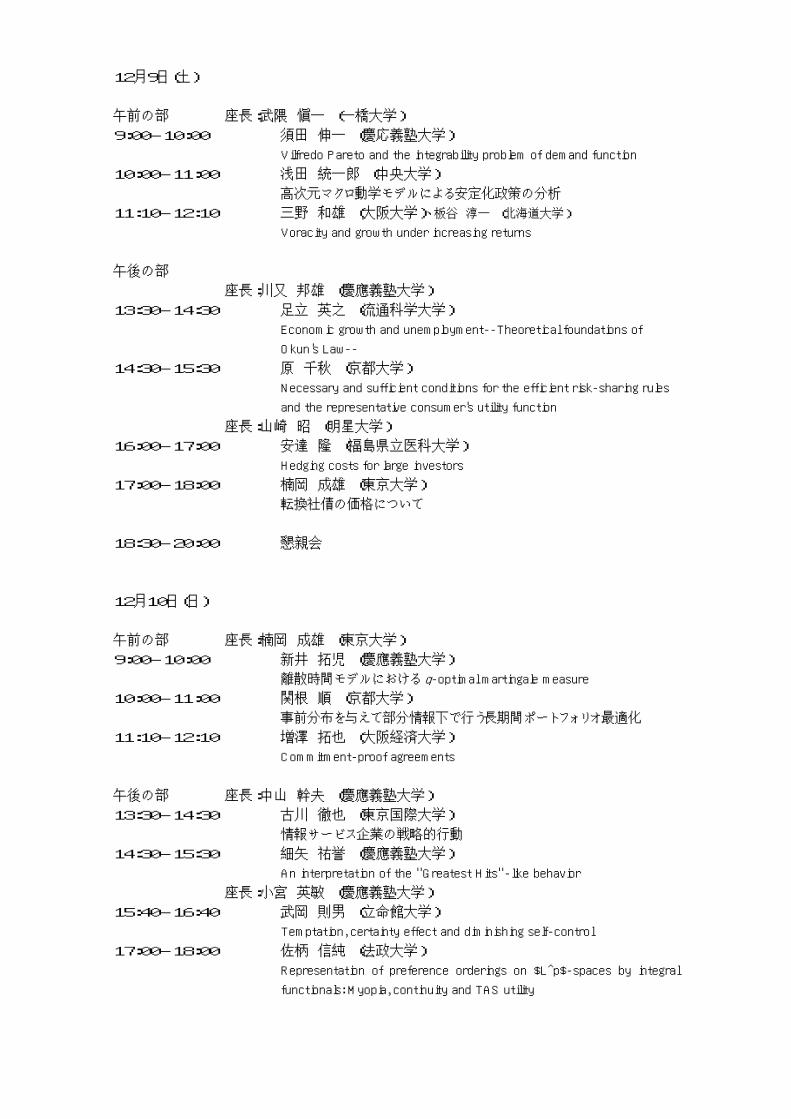

12月9日(土)

午前の部 座長:武隈 愼一 (一橋大学)

9:00-10:00 須田 伸一 (慶応義塾大学)

Vilfredo Pareto and the integrability problem of demand function

10:00-11:00 浅田 統一郎 (中央大学)

高次元マクロ動学モデルによる安定化政策の分析

11:10-12:10 三野 和雄 (大阪大学)、板谷 淳一 (北海道大学)

Voracity and growth under increasing returns

午後の部

座長:川又 邦雄 (慶應義塾大学)

13:30-14:30 足立 英之 (流通科学大学)

Economic growth and unemployment--Theoretical foundations of

Okun's Law--

14:30-15:30 原 千秋 (京都大学)

Necessary and sufficient conditions for the efficient risk-sharing rules

and the representative consumer's utility function

座長:山崎 昭 (明星大学)

16:00-17:00 安達 隆 (福島県立医科大学)

Hedging costs for large investors

17:00-18:00 楠岡 成雄 (東京大学)

転換社債の価格について

18:30-20:00 懇親会

12月10日(日)

午前の部 座長:楠岡 成雄 (東京大学)

9:00-10:00 新井 拓児 (慶應義塾大学)

離散時間モデルにおける q-optimal martingale measure

10:00-11:00 関根 順 (京都大学)

事前分布を与えて部分情報下で行う長期間ポートフォリオ最適化

11:10-12:10 増澤 拓也 (大阪経済大学)

Commitment-proof agreements

午後の部 座長:中山 幹夫 (慶應義塾大学)

13:30-14:30 古川 徹也 (東京国際大学)

情報サービス企業の戦略的行動

14:30-15:30 細矢 祐誉 (慶應義塾大学)

An interpretation of the "Greatest Hits"-like behavior

座長:小宮 英敏 (慶應義塾大学)

15:40-16:40 武岡 則男 (立命館大学)

Temptation, certainty effect and diminishing self-control

17:00-18:00 佐柄 信純 (法政大学)

Representation of preference orderings on $L^p$-spaces by integral

functionals: Myopia, continuity and TAS utility

Axiomatic Characterization of the Maximin

Principle in the Arrow-Dasgupta Economy∗

Koichi Suga†

Waseda UniversityDaisuke Udagawa‡

Waseda University

November, 2006

Abstract

This paper provides an axiomatic characterization of the Rawlsianmaximin principle in a dynamic economy Arrow (1973) and Dasgupta(1974a,b) constructed to examine behavior of the principle under thefesibility conditions of consumption and production. Our exercise givesan answer to the question of why the maximin principle generates thedifferent paths, where one is a saw-tooth shaped path and the other aconstant path. We make use of the axioms of effectiveness, weak Paretoprinciple, Hammond equity and group equity. These axioms except oneare familiar in the characterization of the maximin principle.

∗We are most grateful to John Weymark, Vanderbuilt University, and Masayuki Saito,Waseda University, for their valuable comments. We also thank the seminar participantsat Hitotsubashi University and Waseda University, especially Professors Tomoichi Shinot-suka, Kotaro Suzumura, Koichi Tadenuma, Shiro Yabushita and Naoki Yoshihara. Wethank Waseda University for financial support.

†School of Political Science and Economics, Waseda University, 1-6-1, Nishiwaseda,Shinjuku-ku, Tokyo, 169-8050, JAPAN.

‡Graduate School of Economics, Waseda University, 1-6-1, Nishiwaseda, Shinjuku-ku,Tokyo, 169-8050, JAPAN.

1

2006 Mathematical Economics, RIMS, Kyoto University (December 8, 2006)

History versus Expectations in Economic Geography Reconsidered

Daisuke Oyama

Graduate School of Economics, Hitotsubashi [email protected]

AbstractThis paper considers a class of adjustment dynamics with forward-looking migrants ina new economic geography model a la Krugman (1991a). Specifically, we employ theequilibrium dynamics due to Krugman (1991b) and Fukao and Benabou (1993), wheremigration incurs moving costs which depend on the size of the current migration flow,so that migrants care about the future migration behavior of the economy. Our maingoal is to identify a state that is absorbing (i.e., if the initial state is in a neighborhoodof this state, then any equilibrium path converges to it) and globally accessible (i.e., forany initial state, there exists an equilibrium path that converges to this state) when thedegree of friction is small (i.e., the migration cost and/or the rate of time preference issmall). We show that such a state generically exists (which is unique by definition) andis characterized as a unique maximizer of a potential function of the static model.

The proof strategy for our result follows that of Hofbauer and Sorger (1999), whostudy stability under a different class of perfect foresight dynamics, due to Matsui andMatsuyama (1995), in potential games. We first show that equilibrium paths in ourdynamics are solutions to a certain optimal control problem with state variable inequalityconstraints (see, e.g., Hartl et al. (1995)). Global accessibility is then shown by a turnpiketheorem for the optimal control problem, while absorption follows from the observationthat the maximized Hamiltonian of the optimal control problem serves as a Lyapunovfunction for bounded trajectories.

The paper is available at:

http://www.econ.hit-u.ac.jp/~oyama/papers/hist-vs-exp.html

References

Fukao, K. and R. Benabou (1993). “History versus Expectations: A Comment,” QuarterlyJournal of Economics 108, 535-42.

Hartl, R. F., S. P. Sethi, and R. G. Vickson (1995). “A Survey of the Maximum Principlesfor Optimal Control Problems with State Constraints,” SIAM Review 37, 181-218.

Hofbauer, J. and G. Sorger (1999). “Perfect Foresight and Equilibrium Selection in Sym-metric Potential Games,” Journal of Economic Theory 85, 1-23.

Krugman, P. (1991a). “Increasing Returns and Economic Geography,” Journal of PoliticalEconomy 99, 483-499.

Krugman, P. (1991b). “History versus Expectations,” Quarterly Journal of Economics 106,651-67.

Matsui, A. and K. Matsuyama (1995). “An Approach to Equilibrium Selection,” Journal ofEconomic Theory 65, 415-434.

Age-Structured Population Dynamics in Mathematical

Epidemiology

稲葉 寿 (東京大学大学院数理科学研究科)

ヒト集団や動植物個体群における感染症の流行は、健康で安全な生活を営むという現代社会の普遍的課題に

とって最大の脅威の一つである。1980年代に世界的流行が始まった HIV/AIDS、1990年代における BSE(牛

海綿状脳症)、 vCJD(変異性クロイツフェルト・ヤコブ病)、さらに 2002年 11月に中国広東省を発して、世

界的に流行した致死性の肺炎(SARS: 重症急性呼吸器症候群)流行等の新興感染症は、現代社会がもつ感染症

流行リスクに対する脆弱性を改めて認識させるものであった。一方で、よく知られたインフルエンザや結核、

熱帯地域におけるマラリア等も根絶の難しい感染症であり、相変わらず大きな被害を生み出している。感染症

の流行現象は実験室的観察でこれを扱うことはできないから、どのように流行が発生し、予防のためにどのよ

うな介入行為が有効であるか等を知るためには、これを定量的に数理モデルを用いて分析する必要がある。

感染症の流行過程の数理的研究は長い研究の伝統があり、その端緒は 18世紀のダニエル・ベルヌーイによ

る天然痘死亡率に関する研究に遡ると言われるが、今世紀初頭のロス卿によるマラリア流行に関する閾値定理

の発見やケルマックとマッケンドリックによる 1920年代から 30年代にかけての一連の業績によってその基

礎が与えられた。その後 1970年代に至るまではその進歩は緩慢なものであったが、上記のように、1980年代

以降、新興再興感染症の脅威が明らかとなるにしたがって、流行の予測と効果的な予防や治療を評価するため

の数理モデル研究は、欧米の数理生物学、応用数学の研究者によって非常に注目され、強力に推進されるよう

になった。理論的な側面から見ると、同時期に年齢構造、空間構造、生理的構造などの内的構造を考慮に入れ

た個体群動態の数学的理論 (structured population dynamics)が発達してきており、感染症モデルはその最

も興味深い応用分野とみなされたという事情もある。

本講演でははじめに感染症流行の数理モデル、特に年齢構造をもつ個体群ダイナミクスとして定式化される

SIR型モデルの基本的な構造と結果について紹介する。古典的結果はホスト人口の定常性を前提としているも

のが大部分であるが、人口現象と感染症流行の相互作用を考えていくためには、ホスト人口サイズの変動を取

り扱えるようにモデルを拡張していく必要がある。本講演では、一次同次の非線形モデルとして定式化される

ケースを考え、ホスト人口が安定人口モデルで記述される場合における指数関数型成長解の線形安定性の原理

を確立する。この結果を利用して、麻疹や水疱瘡などの小児に普遍的な感染症に関する古典的なモデルである

MSEIRモデルの閾値定理を示す。

参考文献

[1] H. Inaba (2006), Mathematical analysis of an age-structured SIR epidemic model with vertical

transmission, Disc. Cont. Dyn. Sys, Ser. B, 6(1): 69-96.

[2] H. Inaba (2006), Age-structured homogeneous epidemic systems with application to the MSEIR

epidemic model, to appear in J. Math. Biol.

1

! !

!

Æ

Price and Quantity Competition in an Oligopoly

with Discrete Choices

Shin Kawai∗and Tadashi Minagawa†

Graduate school of Economics,

Nagoya University,

Furo-cho, Chikusa-ku, Nagoya, 464-8601, Japan.

Abstract

This paper investigates the price and quantity competition in an oligo-

poly with capacity constraints; a Bertrand-Edgeworth competition. We

assume that consumers take into account the probability of purchase given

prices and quantities. In the preceding Bertrand-Edgeworth competition

models, two rationing rules, efficient and propotional rationing, have been

proposed. We consider a consumer’s rational behavior instead of these

rules, and show that there is a range of a continuum of symmetric Nash

equilibrum above marginal cost.

JEL classification: L13, D43

Keywords: Bertrand-Edgeworth, Oligopoly, Rationing Rules

∗Tel.: +81-52-789-5456. Fax.: +81-52-789-5456. E-mail: [email protected]†Tel.: +81-52-789-2384. Fax.: +81-52-789-4924. E-mail: [email protected]

1

Vilfredo Pareto and the Integrability Problem of

Demand Functions

Shinichi Suda Keio University

ABSTRACT

On the occasion of the centennial since the publication of Vilfredo Pareto’s Manuale di Economia Politica, I will reexamine the problem of integrability in the theory of consumer behavior. The integrability problem concerns, in short, whether one can “recover” a preference ordering that generates the given demand function. In the first part, I will review the development of Pareto’s treatments on this problem, from the year of 1892 to 1909, when a revised French version of Manuale was published as Manuel d’économie politique. The latter contains the enlarged mathematical appendix, reflecting the comments given by an Italian mathematician, Vito Volterra, in his review article of Manuale. In the second part, I examine the modern answers to the problem of integrability, featuring especially on the theorems by Samuelson (1950), Hurwicz and Uzawa (1971) and Debreu (1972), and consider the significance of the problem in the modern general equilibrium theory. Samuelson, P. A. (1950), “The Problem of Integrability in Utility Theory,”

Economica, N.S., 17, 355-385. Hurwicz, L. and H. Uzawa (1971), “On the Integrability of Demand

Functions,” Chap. 6 in Preferences, Utility and Demand, edited by J. Chipman, L. Hurwicz, M. Richter, and H. Sonnenschein. New York: Harcourt Brace, Jovanovich.

Debreu, G. (1972), “Smooth Preferences,” Econometrica, 40, 603-615.

A High-Dimensional Keynesian Macrodynamic Model with and without Time Delay of Policy Response Toichiro Asada Faculty of Economics, Chuo University, Tokyo, Japan 中央大学経済学部 浅田統一郎 Abstract. In this paper, we study the macroeconomic effect of government’s fiscal stabilization policy with and without time delay of policy response by using the analytical framework of ‘nonlinear high-dimensional Keynesian macrodynamic model’, which consists of a system of nonlinear differential equations with many variables. We can summarize the main conclusions of this paper as follows. (1) If the speed of the quantity adjustment of disequilibrium in the goods market is sufficiently high, the system becomes unstable under the lack of government’s active stabilization policy. (2) If the delay of government’s policy response is sufficiently short, the sufficiently active fiscal stabilization policy can stabilize the economy. (3) If the delay of policy response is sufficiently long, the economy becomes unstable irrespective of the value of the fiscal parameter. (4) Under some combinations of parameter values, endogenous cyclical fluctuations occur.

Voracity and Growth under Increasing

Returns

Jyunichi Itaya (Hokkaido University)

Kazuo Mino (Osaka University)

Abstract This paper investigates a growing economy without secure property rights based on the differential-game modelling. We extends the base model by introducing variable labor supply and increasing returns to scale. It is assumed that capital stock is jointly owned by multiple interest groups and that each group participates production activities by supplying its labor force. In this setting, there are two opposing factors that affect long-term growth: over consumption in the absence of secure property rights and the scale effect due to the presence of increasing returns. The growth performance of the economy thus depends on which factor dominates. In addition to characterizing the balanced-growth equilibrium, we examine local determinacy of equilibrium.

経済成長と失業

――オークンの法則の理論的基礎――

流通科学大学 足立英之

ソロー・モデルをはじめとする経済成長モデルは、完全雇用を前提としており、失業は

説明できない。というよりも、長期的な成長を扱うモデルは、失業を説明することは意図

していないと言う方が正確かもしれない。他方、Okun (1962) は、経済成長率が失業率の変化と負の相関関係をもつという事実をアメリカ経済のデータの分析から発見した。それ

はオークンの法則と呼ばれる。しかし、オークンの法則はあくまで経験法則であり、それ

を基礎づける理論はまだ明らかにされていない。このように、完全雇用を前提とした堅固

な成長理論がある一方で、経済成長が失業と密接に関係していることを示す堅固な経験法

則が存在していることは、一見奇異に見える。 現代のマクロ経済学では、成長を扱う長期の理論と変動を扱う短期の理論が完全に分割

され、それぞれ別の理論として教えられており、両者がどのように繋がるのかは必ずしも

明らかにされていない。しかし、最近 Blanchard (1997) は、彼が中期のモデルと呼ぶ興味深いモデルを展開し、1970年代後半以降におけるヨーロッパ諸国の高失業の原因と所得分配の動向を説明する試みを行っている。Solow (2000) も、ヨーロッパ諸国の長期にわたる失業や日本の 1990年代の長期不況などを分析するためには、長期理論と短期理論に中間に位置する中期の理論が必要であると説いている。 本報告では、Blanchard (1997) の労働市場の考え方をソロー・モデルに導入し、中期の成長モデルを構築する。このモデルは、ソロー・モデルとは異なり、成長過程における失

業率の動きを説明することができる。そして、このモデルを用いれば、経済成長と失業率

の変化の間の逆相関関係(オークンの法則)が理論式として導き出される。周知のように、

失業率の変化に対する GDPの変化率の大きさを表す係数は、オークン係数と呼ばれ、アメリカではその係数値は2ほどであるとされている。しかし、その値はアメリカと日本の間

で大きく異なることもいくつかの実証研究によって明らかにされている。経験的法則とし

てのオークンの法則を理論的に基礎づけることによって、どのような要因がオークン係数

の違いをもたらすかについて明らかにすることができる。 Blanchard, O.J.(1997):“The Medium Run,” Brooking Papers on Economic Activity, Vol.2. Okun, A.M.(1962):“Potential GNP: Its Measurement and Significance,” American Statistical Association,

Proceedings of the Business and Economics Section.

Solow, R.M.(2000): “Towards a Macroeconomics of the Medium-Run,”Journal of Economic Perspectives, Vol.14

Necessary and Sufficient Conditions for

The Efficient Risk-Sharing Rules and

The Representative Consumer’s Utility Function

Chiaki Hara* Institute of Economic Research, Kyoto University

August 16, 2006

Abstract

We show that for every collection of increasing risk-sharing rules, one for each consumer, and for every increasing and concave expected utility function, there exists a collection of increasing and concave expected utility functions for which the given risk-sharing rules are efficient and the given utility function coincides with the corresponding representative consumer's utility function. This result shows that the efficiency property imposes no restriction on the risk-sharing rules beyond comonotonicity, or on the representative consumer's utility function beyond monotonicity and risk aversion. We also obtain contrasting results when the individual consumers are assumed to exhibit constant relative risk aversion.

京都大学数理解析研究所 研究集会「経済の数理解析」(2006.12.9)

Hedging costs for large investors

安達 隆 (福島県立医大 : [email protected])

T > 0を有限時間, W (t); 0 ≤ t ≤ Tを完備確率空間 (Ω,F ,P)上の d次元ブラウン運動, F = Ft; 0 ≤ t ≤ TをW によって生成される増大情報系, P を ∫ T

0|p(t)|2 dt < ∞ a.s.を充たす F-発展的可測なRn 値確率過程 pの

集合とする. ここで, 自然数 d, n は n ≤ d であるものとする.市場では 1つの債券と n個の株式が取引されており, また, 2人の大投資家 I0, I1がいるものとする. Π k ⊂ P を

Ikがとることのできる取引戦略 (株式の所有数) πk の集合とする. 大投資家達が戦略 π = (π0, π1) ∈ Π := Π 0×Π 1

を選択したとき, 債券価格過程 Bπ(·)と株価過程 Sπ(·) は次の確率微分方程式に従うものとする:

dB(t) = B(t)rπ(t)dt, B(0) = 1,

dS(t) = diag[S(t)]bπ(t)dt + σπ(t)>dW (t)

, S(0) = s ∈ (0,∞)n.

このとき, 投資家 Ik の割引資産過程Xxk,πk (·) は次式により与えられる:

Xk(t) = xk +∫ t

0

πk(u)>dSπ(u), t ∈ [0, T ], k = 0, 1.

ここで, 記号>は転置を表し, diag[s] は対角成分が s1, . . . , snである n次対角行列, Sπ(·) := Bπ(·)−1Sπ(·)は割引株価過程, rπ(·), bπ(·) = (bπ

1 (·), . . . , bπn(·))>, σπ(·) = (σπ

1 (·) · · · σπn(·))は一様に有界な F-発展的可測な確率過程で,

それぞれR+ 値, Rn 値, Rd ⊗Rn 値をとるものとする. また, 上付き添字 “π”は確率過程 hπ(t, ω)が大投資家の時刻 tまでの戦略 π(u, ω), 0 ≤ u ≤ t から影響を受けることを意味する.今, 投資家 I0 が投資家 I1 に条件付き請求権 BπCπ, T π を販売するとしよう. ここで, Cπ(·)は非負値の F-適

合確率過程, T π は I1 が請求権を行使できる F-停止時 τ の (T を含む)集合である. つまり, I1 が時刻 τ(ω) ∈ T π

に支払い請求したならば, I0は Bπ(τ(ω), ω)Cπ(τ(ω), ω) を支払うものとする. このとき, I0と I1の最小複製費用

hup, hlow はそれぞれ次のように定義される:

hup := inf

x0 ≥ 0

∣∣∣∣∣∀π1 ∈ Π 1, ∃π0 ∈ Π 0 s.t.

Xx0,π0 (τ) ≥ Cπ(τ) a.s., ∀τ ∈ T π.

hlow := sup

x1 ≥ 0

∣∣∣∣∣∀π0 ∈ Π 0, ∃π1 ∈ Π 1, ∃τ ∈ T π s.t.

X−x1,π1 (τ) + Cπ(τ) ≥ 0 a.s.

これらを確率的ゲームにおける値関数として表現するために, Dを本質的に有界で F-発展的可測なRd値確率過程

ν の集合とし, 確率測度の系 Pν ; ν ∈ Dを

Pν(Λ) := E [1lΛZν(T )] = E[1lΛ exp

∫ T

0

ν(t)>dW (t)− 12

∫ T

0

|ν(t)|2dt

], Λ ∈ FT

で定義する. このとき, 次の結果を得る.

定理 最小複製費用 hup, hlow は次の表現を持つ :

hup = supπ1∈Π 1

infπ0∈Π 0

supτ∈T π

supν∈D

Eν

[(Cπ(τ)−X0,π

0 (τ))+

]

hlow = limm→∞

infπ0∈Π 0

supπ1∈Π 1

supτ∈T π

infν∈D

Eν

[(Cπ(τ) + X0,π

1 (τ)) ∧m

]

ここで, a+ := a ∨ 0 = maxa, 0, a ∧ b := mina, b で Eν は Pν の下での期待値を意味する. さらに,

(i) 各 π ∈ Π , τ ∈ T π に対して, ある定数 p > 1があって, E[|X0,π0 (τ)|p] < ∞ ならば,

hup =(

supπ1∈Π 1

infπ0∈Π 0

supτ∈T π

supν∈D

Eν

[Cπ(τ)−X0,π

0 (τ)])+

(ii) 各 π ∈ Π , τ ∈ T π に対して, ある定数 p > 1があって, E[Cπ(τ)p + |X0,π1 (τ)|p] < ∞ ならば,

hlow = infπ0∈Π 0

supπ1∈Π 1

supτ∈T π

infν∈D

Eν

[Cπ(τ) + X0,π

1 (τ)].

離散時間モデルにおける q-optimal

martingale measure

新井拓児慶應義塾大学経済学部

Abstract

本講演では,離散時間モデルにおける q-optimal martingale measureの密度関数

の計算方法を提示する.但し,1 < q < ∞とする.Schweizer (1996)において,adjustment processなるものが定義され,それを

用いた variance-optimal martingale measureの表現が導出された.さらに,彼は

その論文の中で離散時間モデルにおける adjustment processを backwardに導出

する計算方法を提示した.そして Grandits (1999)は,株価過程の有界性の下,こ

の adjustment processの backward inductionを q-optimal martingale measure

の場合に拡張した.

そこで本講演では,qの共役 pに対して株価過程が p 次可積分性を持つ場合

を検討する.ポートフォリオ価値過程全体がある種の p 次可積分性を持つよう

な可予測過程のクラスを定式化し,その空間が閉になるような良い十分条件を与

える.それによって密度関数が Lq-空間に属すような signed martingale measure

が存在するための条件が与えられる.そして,adjustment processの backward

inductionから q-optimal martingale measureを構成する.本研究の結果は,離

散時間モデルにおける p-optimal hedgingの表現の導出へつながるものである.

1

事前分布を与えて部分情報下で行う長期間ポートフォリオ最適化

(英文論文タイトル:Risk-sensitive portfolio optimization

under partial information

with non-Gaussian initial prior)

Jun Sekine,Institute of Economic Research, Kyoto University,

Yoshida-Honmachi, Sakyo-ku, Kyoto 606-8501, Japan.

Abstract

The maximization of the growth rate of expected power-utility of ter-minal wealth is considered under partial information setting. Both finiteand infinite time horizon problems are treated, assuming that the driftX of the n-dimensional risky asset price process is modelled by an unob-servable linear SDE with a given initial prior distribution. The finite timehorizon problem is solved by using 2n-dimensional Markovian “sufficientstatistics” and a closed-form expression of the optimal trading strategyis provided. As the time horizon goes to infinity, the influence of thechoice of the initial prior becomes negligible, and, as a result, the infinitetime horizon problem is solved by using a reduced n-dimensional suffi-cient statistic. In particular, the maximal growth rate and the optimaltrading strategy are described by using the stabilizing solutions to two n-dimensional matrix-valued algebraic Riccati equations, as Nagai and Peng(2002) study with a given, fixed initial position of X.

1

Commitment-Proof Agreements betweenTwo Players without Complete Information (要約)

増澤拓也

大阪経済大学経済学部 [email protected]

要約

この論文では、Greenberg (The Theory of Social Situations: A Game-

Theoretic Approach, Cambridge University Press, Cambridge, 1990) によっ

て提示された解概念 ( CSSB of individual commitment situation)をもとに、

完備情報を持たない二人ゲームにおけるコミットメントによる離反に耐える

協定とは何かを定義する事を試みる。

このような解概念を定義する目的は、外部性の発生する経済におけるただ

乗り行動が引き起こす問題を論じる事にある。N人協力ゲームにおける伝統

的な考えである、max-mini値による改善あるいは支配という考え方は、反駁

されない協定とは何かについての第一の条件を与えるが、ただ乗り行動を期

待することから生じる離反を考慮することにはならない。

Greenberg は 離反後に新たな協定が提示されるという状況を考え、協定

の列としての解 “CSSB of Individual Commitment Situation ” を定義した。

この解は、上述のただ乗り問題を論じる為に、max-mini 値の考えに基づく離

反不可能性に加え、さらに厳しい条件を課したものと評価する事ができる。本

稿では次の二点に着目し、ゲームに関する認識論理を用いて、新たな解の定

義を試みる。

1. max-mini 値は自分の利得にのみ依存しているという点で、不完備情報下

において有効な考えである。不完備情報下においては、自分の離反後に

相手がどのような行動を選択するかについての不確実性がもたらされ、

離反を困難にする場合がある。

2. 不完備情報下においては、相手が離反を起こさないという事が相手の選

好についての新たな情報をもたらし、自分の離反が自分に利益をもたら

す事を新たに知る可能性がある。

1

情報サービス企業の戦略的行動

古川徹也

(東京国際大学経済学部)

年 月 日

要約

情報サービスを提供する企業の役割が,近年ますます拡大している。これら情報サービス企業に

よる財・サービスの質にかんする「評価」が,消費者の意思決定の中で重要度を増すようになると,

逆にあたかも情報サービス企業がその財の質を決定するかのような現象があらわれる。つまり,あ

る情報サービス企業が提供する情報になんらかの「権威」が加わると,財の質と無関係に情報サー

ビス企業がどのような情報を提供したかが重要度を増すようになる。情報サービス企業に「権威」

が加わり,「良いモノを情報サービス産業が見つける」のではなく,「情報サービス企業が良いという

モノが良いモノである」「情報サービス企業が良いモノを決める」という事態になる。すると,本

来情報サービス企業は情報の問題に基づく非効率性を緩和するものであるはずだが,それが非効率

性を緩和するとは限らない。

本稿の目的は,金融市場の「格付け機関」と投資家との関係をもとにして,この問題を分析する

ことである。本稿では,投資家にたいして投資対象にかんする情報を提供する格付け機関に,

潜在的に つのタイプ,すなわち常に誠実に情報提供を行うタイプと,利潤を拡大できるチャンス

があるときにのみ誠実な情報収集活動を行うタイプの 種類があるが,それを投資家は観察できな

い, 利用者人数の増大が,投資対象の成果にたいして影響を与える,という つの特徴を持つ

場合に,格付け機関の行動,投資家の行動はどのような特徴を持つかについて分析した。

このモデルでは多数の均衡があり得るが,本稿では 誠実でない格付け機関が全く情報収集活

動を行わないにもかかわらず,すべての投資家が格付け機関を利用する均衡, 誠実でない格付

け機関も情報収集活動をきちんと行う均衡,の 種類の均衡の存在と,そのときの各パラメータと

の関係について検討した。その結果,「誠実な格付け機関であると見なす確率」が十分に高いとき

は,各投資家にとっては,たとえ格付け機関が全く情報収集活動を行わなかったとしても,利用す

ることが有利になる,という の均衡も,いずれの格付け機関も第 期には情報収集活動をきち

んと行い,また同時に投資家も格付け機関を利用するという の均衡も,適当な初期信念(と格

付け機関の利用料)の大きさのもとでは存在することが言えた。またそれぞれの均衡と初期信念と

の関係にかんして,いくつかの結果が得られた。

An Interpretation of the “Greatest Hits”-likeBehavior

Yuhki Hosoya∗

Graduate School of Economics, Keio University

Abstract

We try to explain the strange behavior for suppliers of books orsoftwares which release the cheap(paperback) edition of their productsonly when this product has a good sale, though its cost is nearly zero.We construct a differential equation like the replicator dynamics ofa strategic form game, and show that if supplier’s decision is biased,then his payoff may be better than not biased.

JEL classification numbers: C73, D21.

Keywords: cheap edition, replicator dynamics, biased decision.

∗Tel: +81 42 302 1174; e-mail:[email protected]

1

Temptation, Certainty Effect, and Diminishing

Self-Control

Norio TAKEOKA

Faculty of Economics, Ritsumeikan University,

1-1-1 Noji-Higashi, Kusatsu, Shiga 525-8577, JAPAN

November 14, 2006

Abstract

Gul and Pesendorfer (2001) (Henceforth GP) provide a model of temptation andself-control. In a theory of choice under risk, experimental evidence suggests a “cer-tainty effect”, that is, a decision maker tends to put more weight on a certain objectin comparison with a lottery that is very likely but not completely certain. Thuswhat is certain may be more tempting, in other words, randomization may makeobjects less tempting. However, one of the axioms of GP, called Independence, is notconsistent with such a hypothesis. Our objective is to weaken Independence so as toexplain intuitive choice behavior under risk and temptation.

As in GP, we consider preference on menus of lotteries over consumptions, ∆(C).We axiomatize preference having the following representation: There exist expectedutility functions u, v : ∆(C) → R+ and a continuous, strictly increasing and (weakly)convex function ϕ : R+ → R+ with ϕ(0) = 0 such that preference over menus isrepresented by

U(x) = maxl∈x

(

u(l) − ϕ

(

maxl′∈x

v(l′) − v(l)))

.

As in GP, u and v are interpreted as normative ranking and as temptation ranking,respectively. Taking into account the most tempting lottery within a menu at hand,the decision maker evaluates the menu by maximizing normative utility u(l) minusself-control cost ϕ(maxl′∈x v(l′) − v(l)). Convexity of ϕ means that the marginalcost of self-control is increasing, while it is constant in GP’s model. We show alsouniqueness of the representation.

Keywords: temptation, self-control, preference for commitment, lottery, independenceaxiom, certainty effect.JEL classification: D81

Representation of Preference Orderings onLp-spaces by Integral Functionals: Myopia,

Continuity and TAS Utility

Nobusumi SagaraFaculty of Economics, Hosei University

e-mail: [email protected]

AbstractIn this paper we present an axiomatic approach for representing

preference orderings on Lp-spaces in terms of integral functionals. Weshow that if preference orderings on Lp-spaces satisfy continuity, sep-arability, sensitivity, substitutability, additivity and lower bounded-ness, then there exists a utility function representing the preferenceorderings such that the utility function is an integral functional witha normal integrand satisfying the growth condition. Moreover, if thepreference orderings satisfy the continuity with respect to the weaktopology of Lp-spaces, then the normal integrand is a convex inte-grand. We apply this result to the representation of preference or-derings over time and show that recursive integral functionals can berepresented by integral functionals with constant discount rates.

References

Buttazzo, G. and G. Dal Maso, (1983). “On Nemyckii operators and inte-gral representation of local functionals”, Rendiconti di Matematica, vol. 3,pp. 481–509.

Koopmans, T.C., (1972). “Representation of preference orderings over time”,in: C.B. McGuire and R. Radner, (eds.), Decision and Organization: AVolume in Honor of Jacob Marschak, Amsterdam, North-Holland, pp. 79–100.

Sagara, N., (2007). “Nonconvex variational problem with recursive integralfunctionals in Sobolev spaces: Existence and representation”, Journal ofMathematical Analysis and Applications, vol. 327, pp. 203–219.