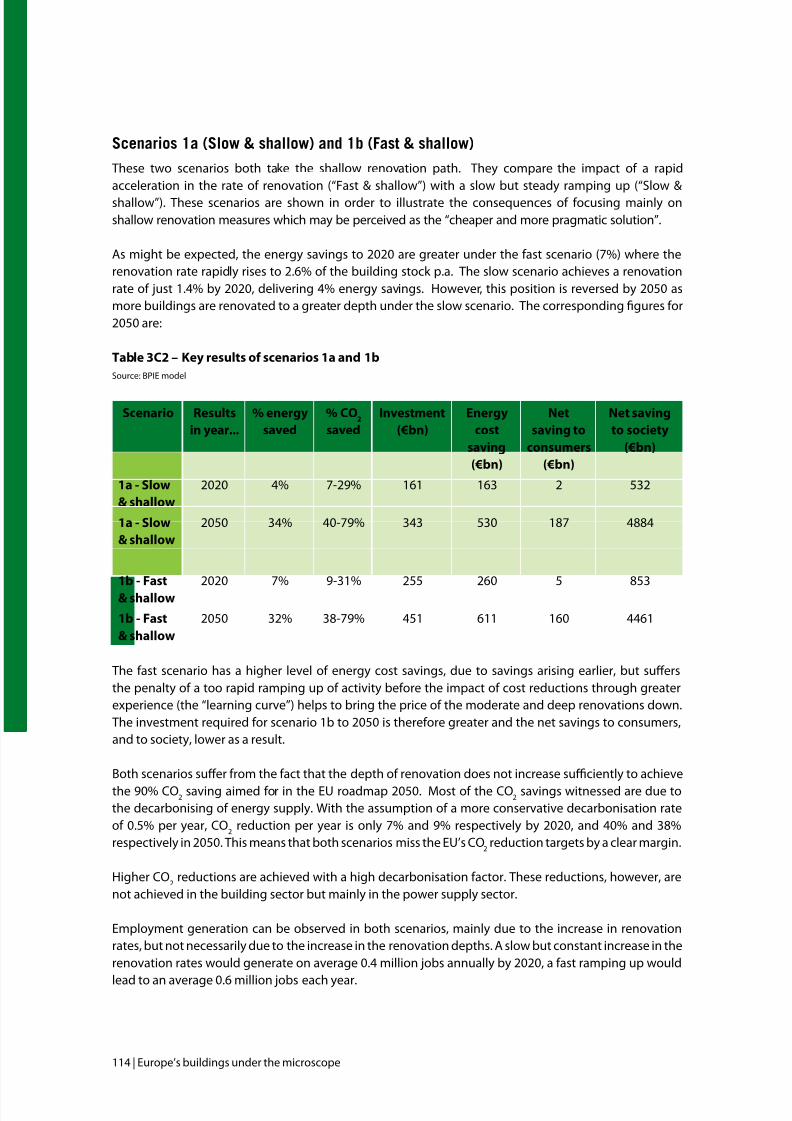

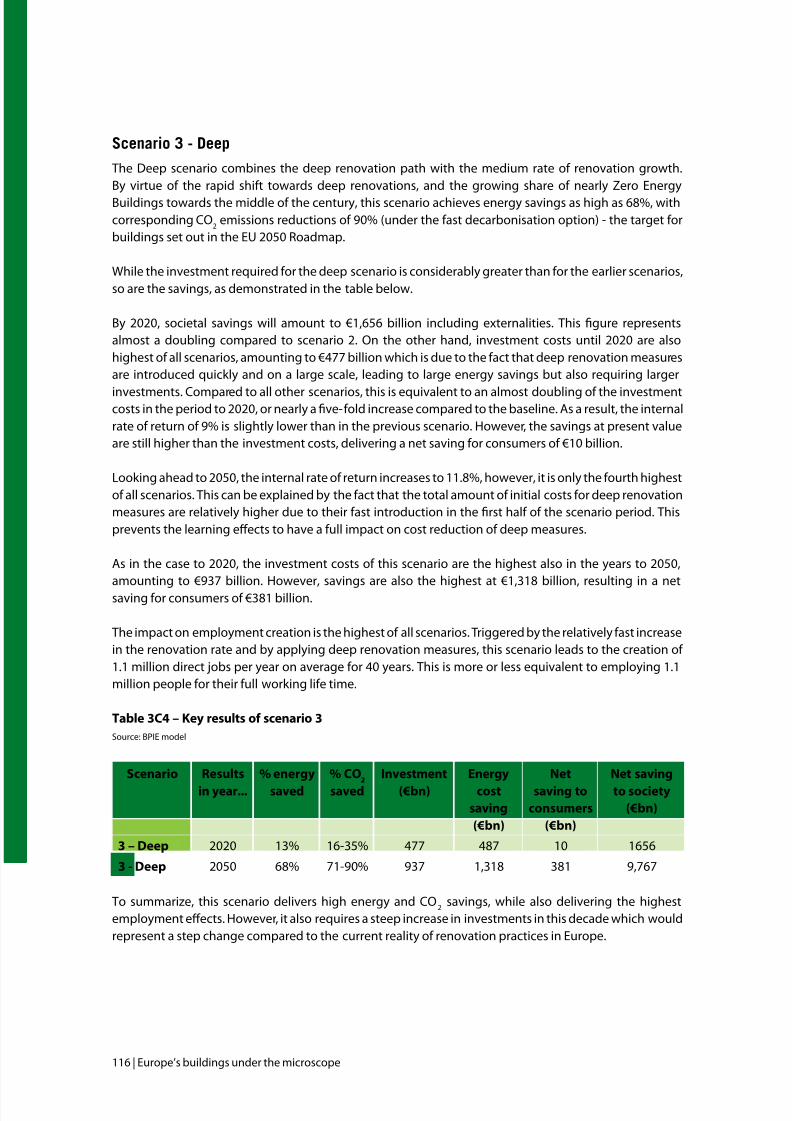

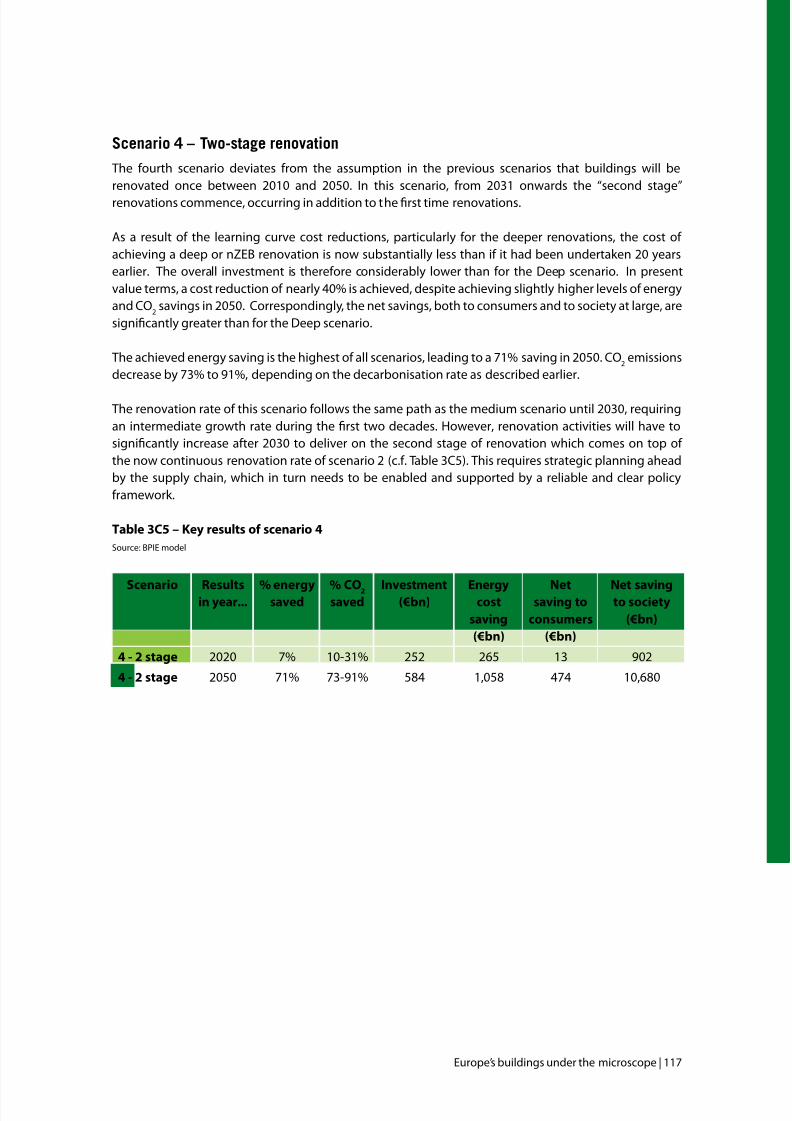

LR CbC Study

133

EuropE’s buildings undEr thE microscopE A country-by-country review of the energy performance of buildings

-

Upload

ionut-pascu -

Category

Documents

-

view

214 -

download

0

Transcript of LR CbC Study

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 1/132

EuropE’s buildings undErthE microscopEA country-by-country review of the energyperformance of buildings

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 2/132

Project lead

Marina Economidou

Editing team

Bogdan AtanasiuChantal DespretMarina EconomidouJoana MaioIngeborg NolteOliver Rap

Contributions

Jens LaustsenPaul Ruyssevelt

Dan Staniaszek David StrongSilvia Zinetti

Graphic Design

Lies Verheyen - Mazout.nu

Published in October 2011 by Buildings Perormance Institute Europe (BPIE)

Copyright 2011, Buildings Perormance Institute Europe (BPIE). Any reproduction in ull or in part o thispublication must mention the ull title and author and credit BPIE as the copyright owner. All rights reserved.

ISBN: 9789491143014

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 3/132

ForEword

Buildings are at the pivotal centre o our lives. The characteristics o a building, its design, its look andeel, and its technical standards not only inuence our productivity, our well-being, our moods and ourinteractions with others, they also dene how much energy is consumed in and by a building, and howmuch heating, ventilation and cooling energy is needed to create a pleasant environment.

We know that buildings cause a signicant amount o greenhouse gas emissions, mainly CO2, altering

our planet’s climate. By renovating buildings to high standards o eciency we can demonstrate thatambitious climate change mitigation actions and improvements in living quality can go hand in hand.The European building stock with its unique mix o historical and modern architecture provides bothsignicant opportunities and challenges.

Efective policies and incentive schemes to reduce the climate change ootprint o buildings requirea solid understanding about the current building stock. The Buildings Perormance Institute Europeintends to contribute to an improved understanding with this report – gathering acts and gures aboutthe European building stock and aggregating the ndings to allow meaningul analysis.

BPIE recognizes that the availability o data is ar rom ideal, and that dynamic policy processes in theEU Member States will outdate very quickly some o the inormation on policies and nancial supportschemes. This is why we are committed to providing updates on certain issues at regular intervals, and Ihope that we can count on the collaboration o many experts in the eld.

Today, the challenge o climate change does not get the same political and media attention as it did

some years ago. However, that does not mean that the problem has gone away, quite the opposite. Butto limit the discussion about energy ecient buildings only to climate change considerations wouldignore the many additional benets which are created through the retrotting o the European buildingstock. The revitalisation o urban quarters, improved comort levels and quality o living and workingspaces, helping people out o uel poverty and creating long term employment are just some o the manypositive efects o a European renovation ‘wave’ which is modelled in the nal part o this report.

In this respect, this report wants to encourage a wider debate on how stakeholders in the buildingsector can collaborate to transorm the European building stock into a highly ecient living and workingenvironment which enables society to become more sustainable, in all aspects o the word’s meaning.BPIE proactively seeks dialogue with the many interested parties, and is looking orward to receiving your

reaction.

Oliver Rap

Executive Director

Buildings Perormance Institute Europe

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 4/132

4 | Europe’s buildings under the microscope

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 5/132

contEnts

ForEword

AcknowlEdgEmEnts

ExEcutivE summAry

introduction

mEthodology

pArt 1 EuropE’s buildings todAy

A. Building typology

Residential buildingsNon-residential buildings

B. CharacteristicsAgeSizeOwnership and tenureLocation

C. Energy perormanceResidential buildingsNon-residential buildings

pArt 2 policiEs And progrAmmEs For improving

EnErgy EFFiciEncy in buildings

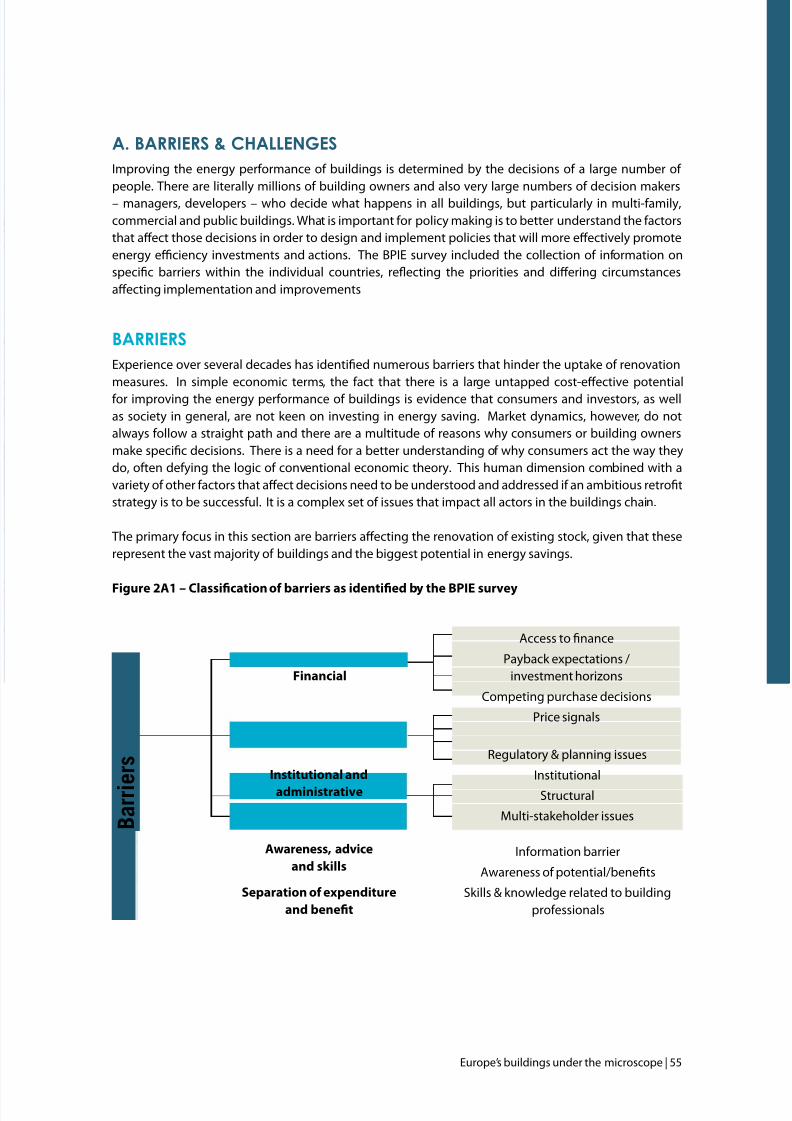

A. Barriers & challengesBarriersChallenges

B. Regulatory and legislative ramework EPBD: Main provisions, implementation and recastBuilding codes

C. Financial programmes

Review o current nancial programmesImpact o selected nancial programmes

D. Other Programmes

pArt 3 rEnovAting with purposE – Finding A roAdmAp to 2050

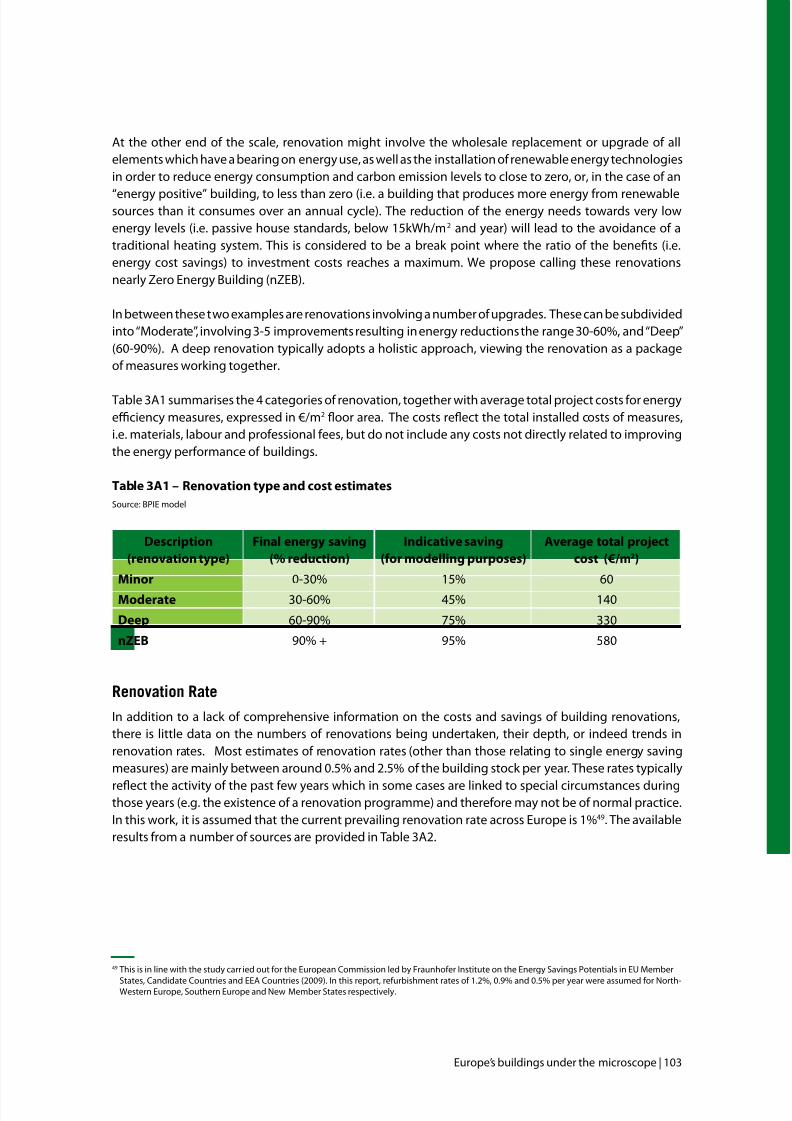

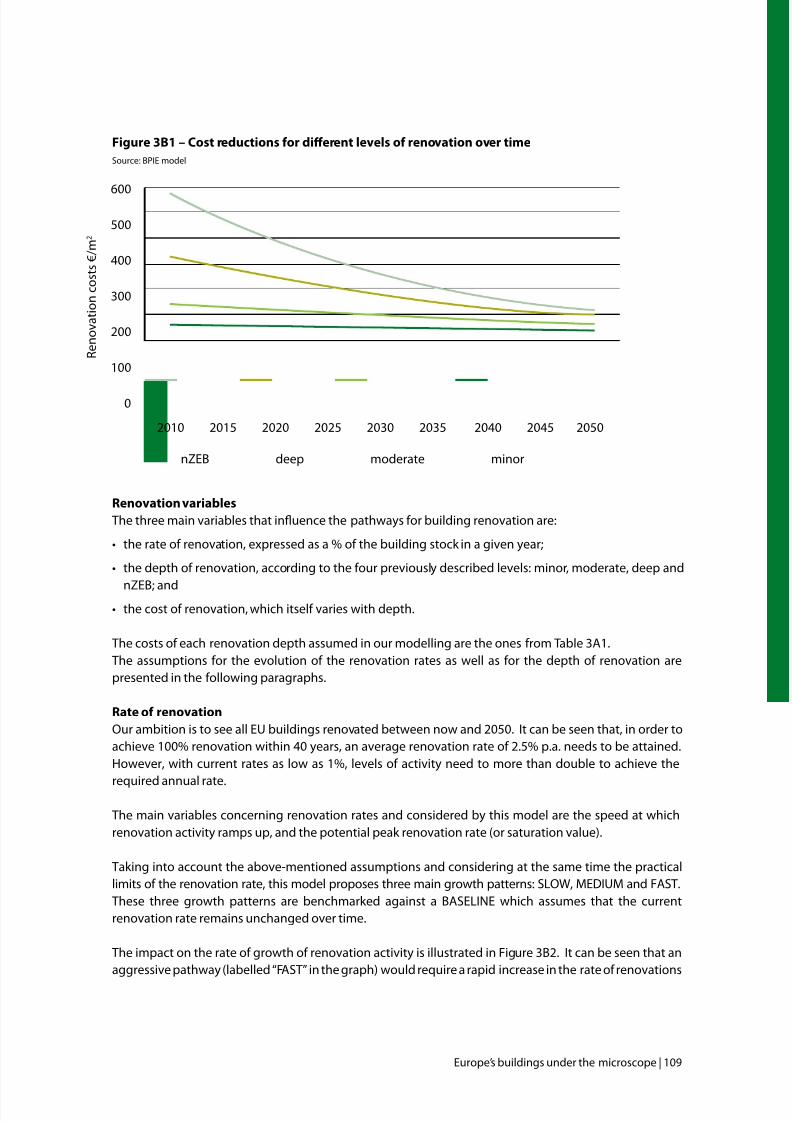

A. Economic indicators

B. Overview o the renovation model

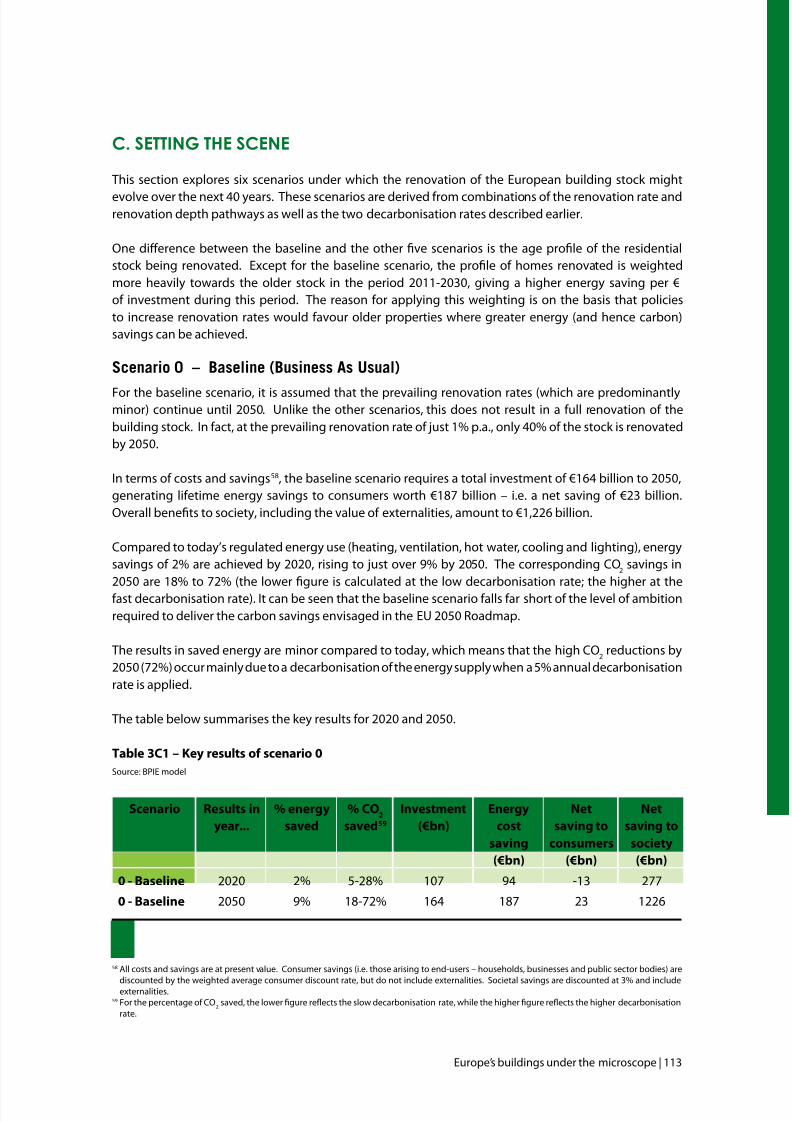

C. Setting the scene

FinAl rEmArks And policy rEcommEndAtionsdEFinitions

3

6

7

19

24

26

27

30323535

3937

41

434451

54

555561

637276

90

9094

95

98

100

106

113

123129

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 6/132

AcknowlEdgEmEnts

This project was initiated by Tudor Constantinescu, rst BPIE executive director and continued by RodJanssen in his unction as Interim Executive Director o BPIE. Rod Janssen, board member o eceee, gaveimportant drive in a critical stage o the project. We would like to thank both o them or their inspirationand guidance.

BPIE would like to express its gratitude towards the steering committee o the project or providing on-going direction and support.

This report was developed by BPIE with the input o various people. We would like to thank the ollowingteam o country experts or sharing their valuable knowledge with us and helping us develop an

understanding o the situation in their respective country:

Randall Bowie, RockwoolCéline Carré, EurimaSusanne Dyrbøl, EuroACEPascal Eveillard, Eurima

Michaela Holl, DG Energy, ECAdrian Joyce, EuroACE

Jens Laustsen, Independent ConsultantOliver Loebel, PU EuropeYamina Saheb, International Energy AgencyConstant Van Aerschot, Laarge/WBCSD

Rick Wilberorce, Glass or Europe

BPIE is thankul to the advisory committee o the project or being a sounding board and or providing chal-lenging eedback in a constructive and enthusiastic manner. The advisory committee was represented by:

AEA, Austrian EnergyAgency

3E Consulting

BSERC, Black Sea EnergyResearch Centre

IENE, Institute o Energy orSouth East Europe

SEVEn

SBi, Danish BuildingResearch Institute

EKVU

MOTIVA

Hubert Despretz,

Expert at ADEME

Wuppertal Institute

IENE, Institute o Energy orSouth East Europe

CEU 3csep

SEAI, Sustainable EnergyAuthority Ireland

Marco Caponigro, IndividualExpert and ENEA (ENEA

Energy Eciency Unit)

PAIC, Centre o processes,analysis and research

Rimantas Sevastijančiukas,Individual expert

Mario Fsadni, Individualexpert

Ministry o housing,

Spatial Planning &Environment

FEWE, Polish Foundationor Energy Eciency

ADENE, Portuguese EnergyAgency

VITAstal and Horia Petran,URBAN-INCERC

TSUS, Building Testing and

Research Institute

Building and CivilEngineering Institute

ETRES Consulting

BOVERKET, Lund University

EST, Energy Saving Trust

INFRAS

SINTEF

6 | Europe’s buildings under the microscope

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 7/132

Europe’s buildings under the microscope | 7

ExEcutivE summAry

From the emotional to the architectural value, buildings occupy a key place in our livesand society as a whole. Yet, the energy perormance o our buildings is generally sopoor that the levels o energy consumed in buildings place the sector among the mostsignicant CO

2emissions sources in Europe. While new buildings can be constructed

with high perormance levels, it is the older buildings, representing the vast majorityo the building stock, which are predominantly o low energy perormance andsubsequently in need o renovation work. With their potential to deliver high energyand CO

2savings as well as many societal benets, energy ecient buildings can have a

pivotal role in a sustainable uture.

Achieving the energy savings in buildings is a complex process. Policy making in this eld requires ameaningul understanding o several characteristics o the building stock. Reducing the energy demandrequires the deployment o efective policies which in turn makes it necessary to understand what afectspeople’s decision making processes, the key characteristics o the building stock, the impact o currentpolicies etc.

Amid the current political discussions at EU level, BPIE has undertaken an extensive survey across allEU Member States, Switzerland and Norway reviewing the situation in terms o the building stock characteristics and policies in place. This survey provides an EU-wide picture o the energy perormanceo the building stock and how existing policies inuence the situation. The data collected was also used

to develop scenarios that show pathways to making the building stock much more energy ecient, inline with the EU 2050 roadmap.

bE

Building oor space in Europe

Building gross oor space in the EU27,Switzerland and Norway

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 8/132

8 | Europe’s buildings under the microscope

A vitAl picture of the europeAn stock

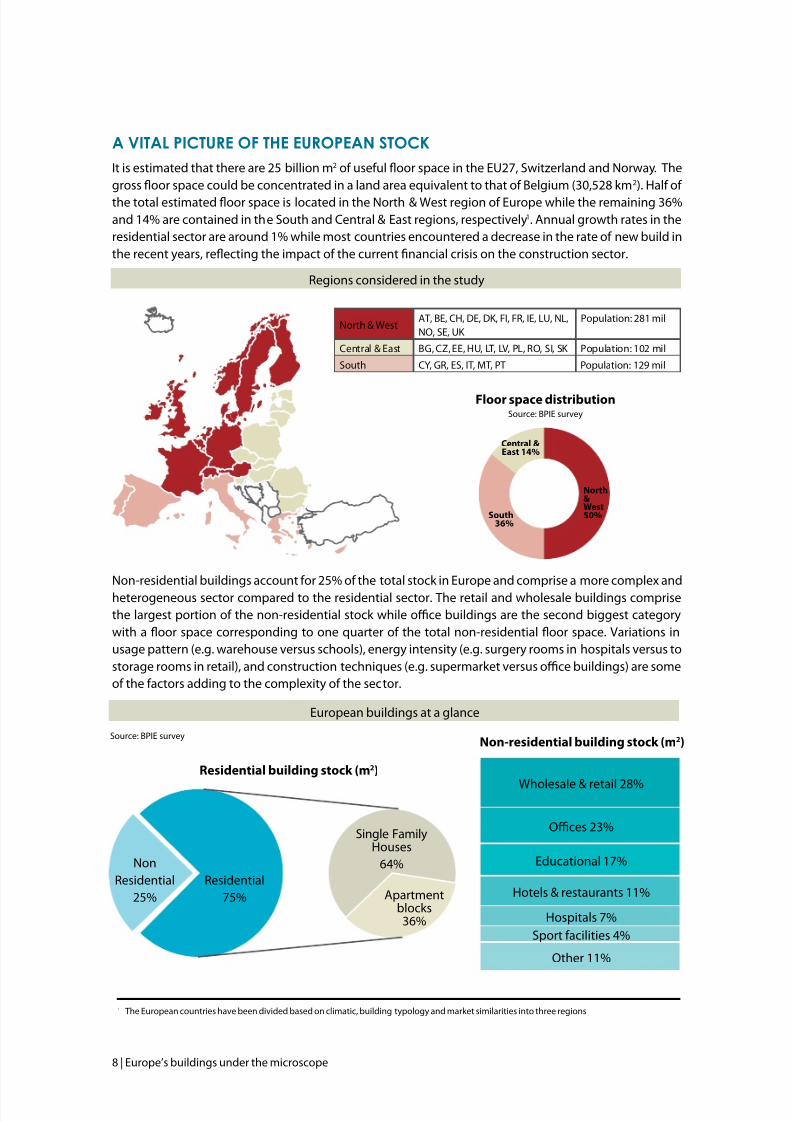

It is estimated that there are 25 billion m2 o useul oor space in the EU27, Switzerland and Norway. Thegross oor space could be concentrated in a land area equivalent to that o Belgium (30,528 km2). Hal o the total estimated oor space is located in the North & West region o Europe while the remaining 36%and 14% are contained in the South and Central & East regions, respectively1. Annual growth rates in theresidential sector are around 1% while most countries encountered a decrease in the rate o new build inthe recent years, reecting the impact o the current nancial crisis on the construction sector.

Non-residential buildings account or 25% o the total stock in Europe and comprise a more complex andheterogeneous sector compared to the residential sector. The retail and wholesale buildings comprisethe largest portion o the non-residential stock while oce buildings are the second biggest categorywith a oor space corresponding to one quarter o the total non-residential oor space. Variations inusage pattern (e.g. warehouse versus schools), energy intensity (e.g. surgery rooms in hospitals versus tostorage rooms in retail), and construction techniques (e.g. supermarket versus oce buildings) are someo the actors adding to the complexity o the sector.

Floor space distributionSource: BPIE survey

South36%

Central &East 14%

North&West50%

NonResidential

25%Residential

75%

Single FamilyHouses

64%

Apartmentblocks

36%

Non-residential building stock (m2)

Residential building stock (m2)

Wholesale & retail 28%

Oces 23%

Educational 17%

Hotels & restaurants 11%

Hospitals 7%Sport acilities 4%

Other 11%

1 The European countries have been divided based on climatic, building typology and market similarities into three regions

North & WestAT, BE, CH, DE, DK, FI, FR, IE, LU, NL,NO, SE, UK

Population: 281 mil

Central & East BG, CZ, EE, HU, LT, LV, PL, RO, SI, SK Population: 102 mil

South CY, GR, ES, IT, MT, PT Population: 129 mil

European buildings at a glance

Regions considered in the study

Source: BPIE survey

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 9/132

Europe’s buildings under the microscope | 9

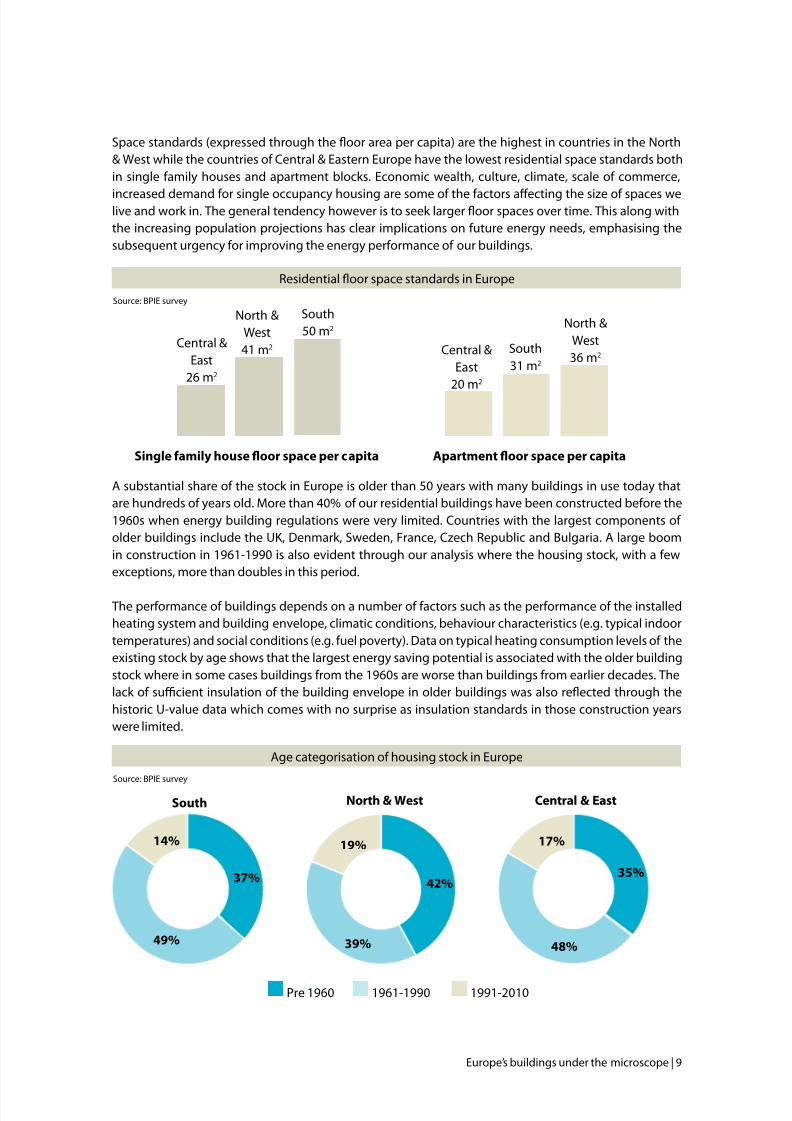

Space standards (expressed through the oor area per capita) are the highest in countries in the North& West while the countries o Central & Eastern Europe have the lowest residential space standards bothin single amily houses and apartment blocks. Economic wealth, culture, climate, scale o commerce,

increased demand or single occupancy housing are some o the actors afecting the size o spaces welive and work in. The general tendency however is to seek larger oor spaces over time. This along withthe increasing population projections has clear implications on uture energy needs, emphasising thesubsequent urgency or improving the energy perormance o our buildings.

A substantial share o the stock in Europe is older than 50 years with many buildings in use today thatare hundreds o years old. More than 40% o our residential buildings have been constructed beore the1960s when energy building regulations were very limited. Countries with the largest components o older buildings include the UK, Denmark, Sweden, France, Czech Republic and Bulgaria. A large boomin construction in 1961-1990 is also evident through our analysis where the housing stock, with a ewexceptions, more than doubles in this period.

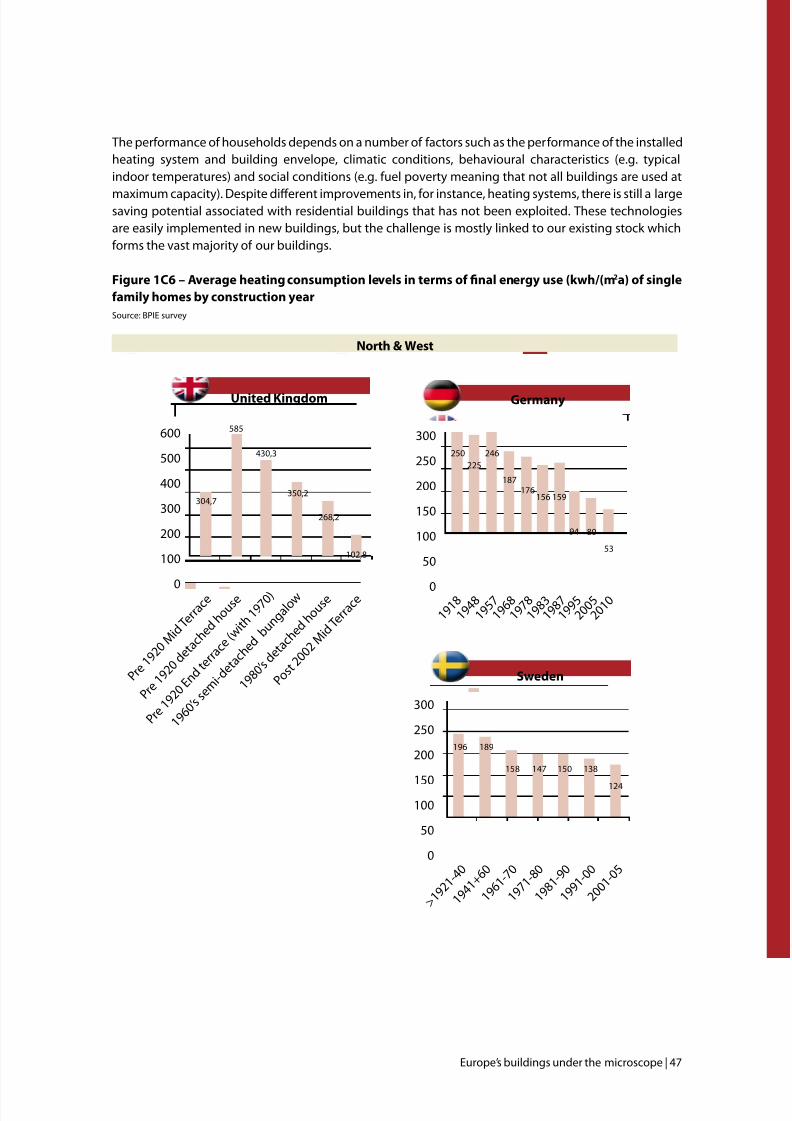

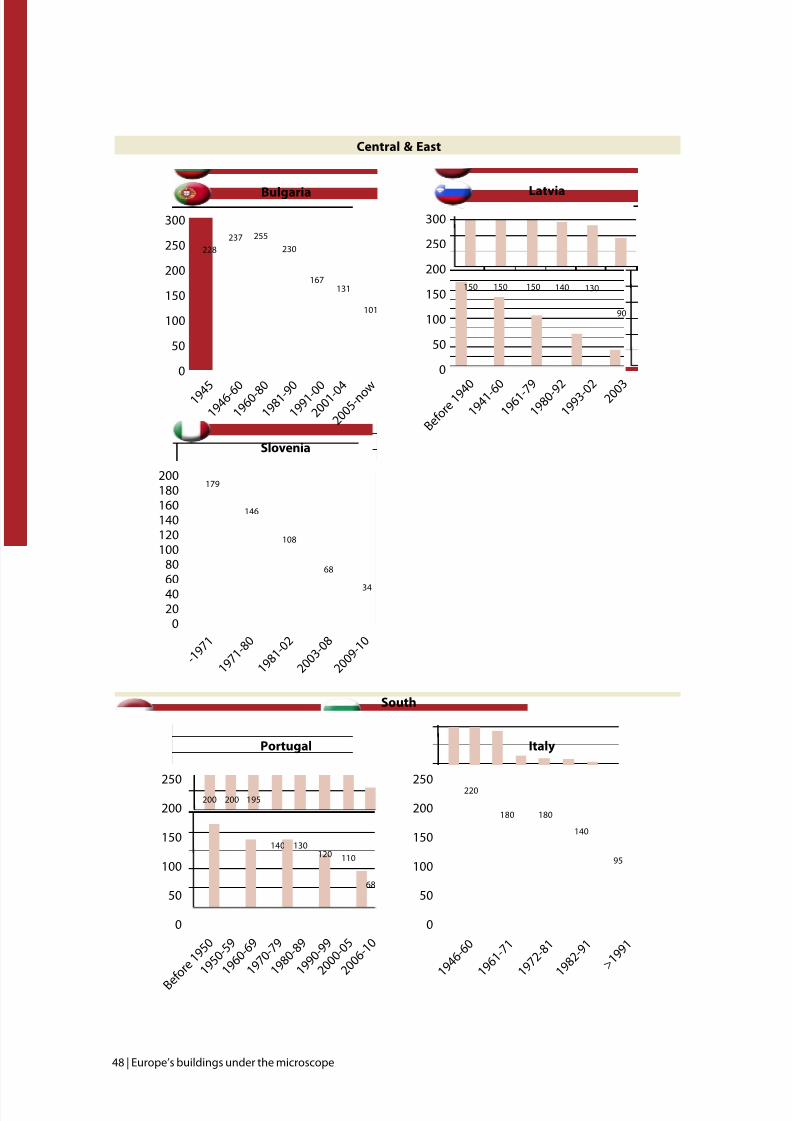

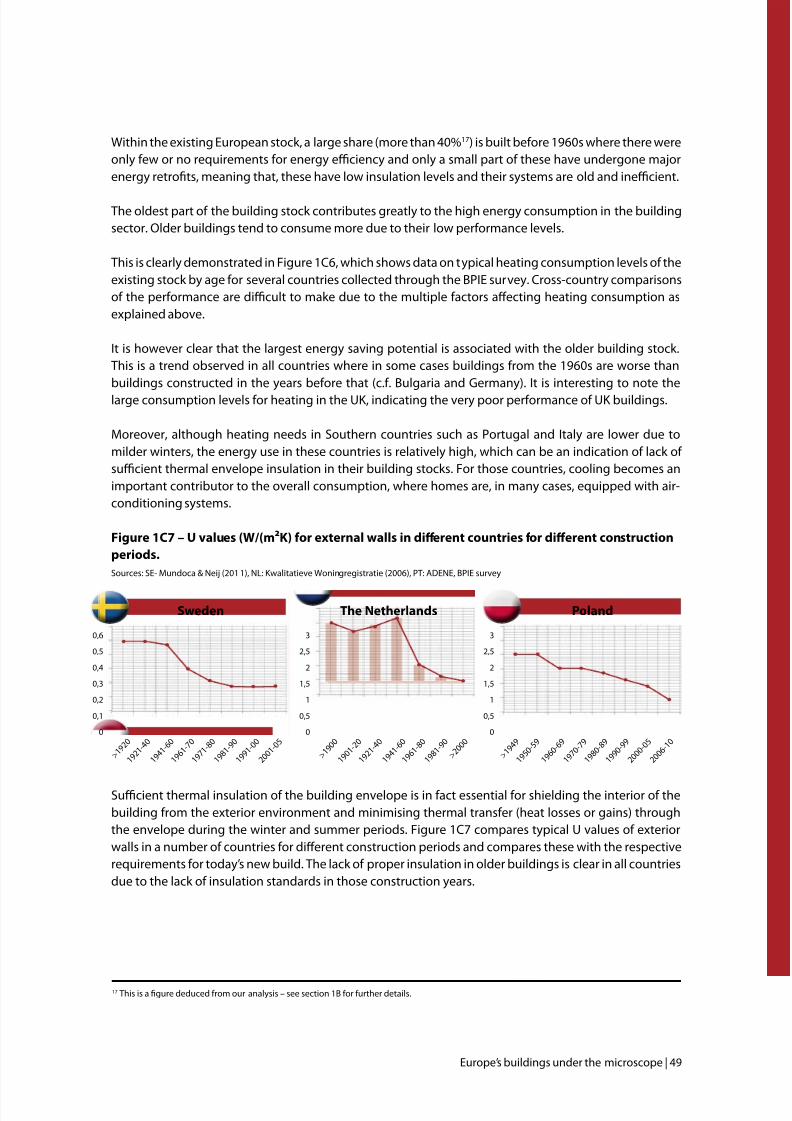

The perormance o buildings depends on a number o actors such as the perormance o the installedheating system and building envelope, climatic conditions, behaviour characteristics (e.g. typical indoortemperatures) and social conditions (e.g. uel poverty). Data on typical heating consumption levels o theexisting stock by age shows that the largest energy saving potential is associated with the older buildingstock where in some cases buildings rom the 1960s are worse than buildings rom earlier decades. Thelack o sucient insulation o the building envelope in older buildings was also reected through thehistoric U-value data which comes with no surprise as insulation standards in those construction yearswere limited.

Residential oor space standards in Europe

Single amily house oor space per capita

Central &East

26 m2

North &West41 m2

South50 m2

Apartment oor space per capita

Central &East

20 m2

North &West36 m2

South31 m2

Age categorisation o housing stock in Europe

37%

14%

49%

South North & West

42%

19%

39%

Central & East

17%

35%

48%

Pre 1960 1961-1990 1991-2010

Source: BPIE survey

Source: BPIE survey

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 10/132

10 | Europe’s buildings under the microscope

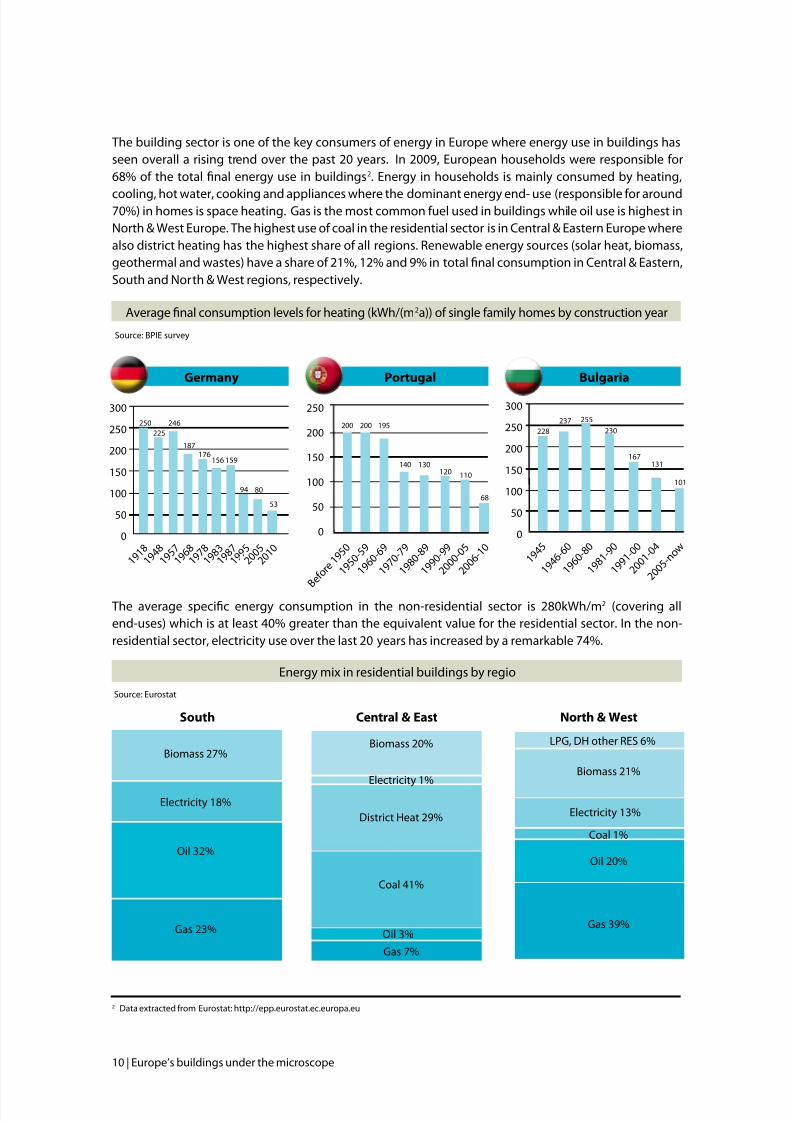

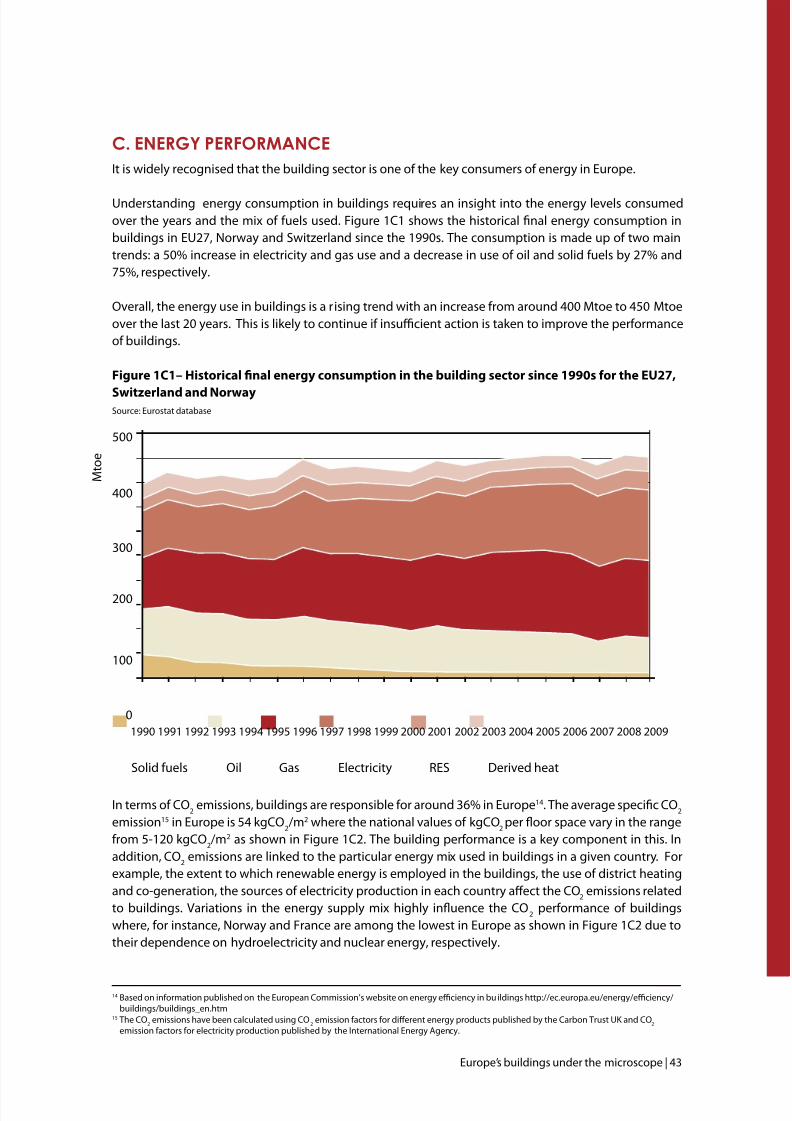

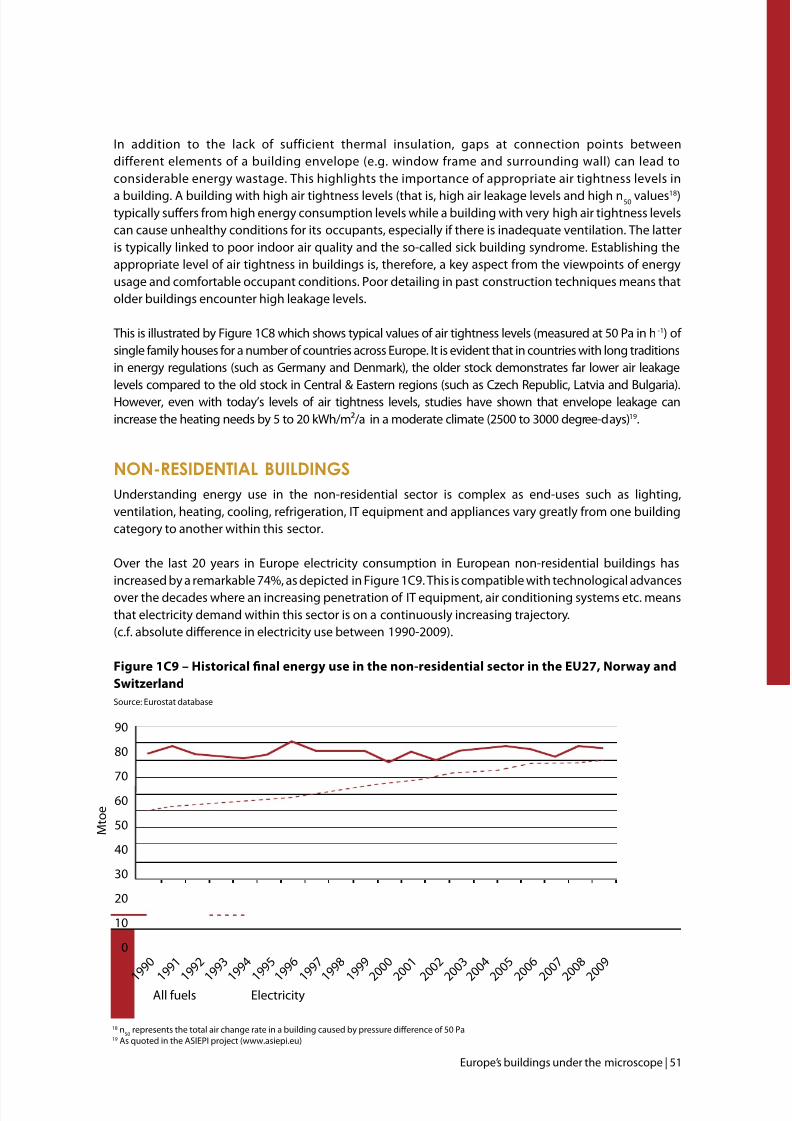

The building sector is one o the key consumers o energy in Europe where energy use in buildings hasseen overall a rising trend over the past 20 years. In 2009, European households were responsible or68% o the total nal energy use in buildings2. Energy in households is mainly consumed by heating,

cooling, hot water, cooking and appliances where the dominant energy end- use (responsible or around70%) in homes is space heating. Gas is the most common uel used in buildings while oil use is highest inNorth & West Europe. The highest use o coal in the residential sector is in Central & Eastern Europe wherealso district heating has the highest share o all regions. Renewable energy sources (solar heat, biomass,geothermal and wastes) have a share o 21%, 12% and 9% in total nal consumption in Central & Eastern,South and North & West regions, respectively.

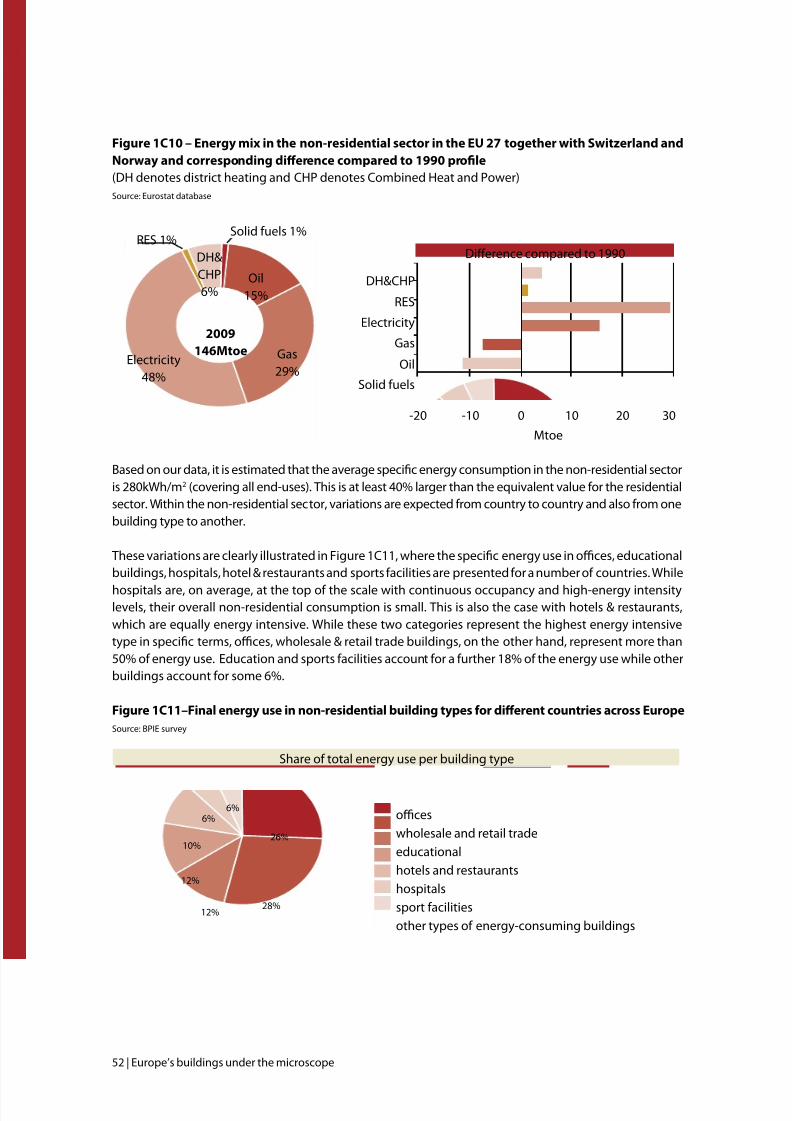

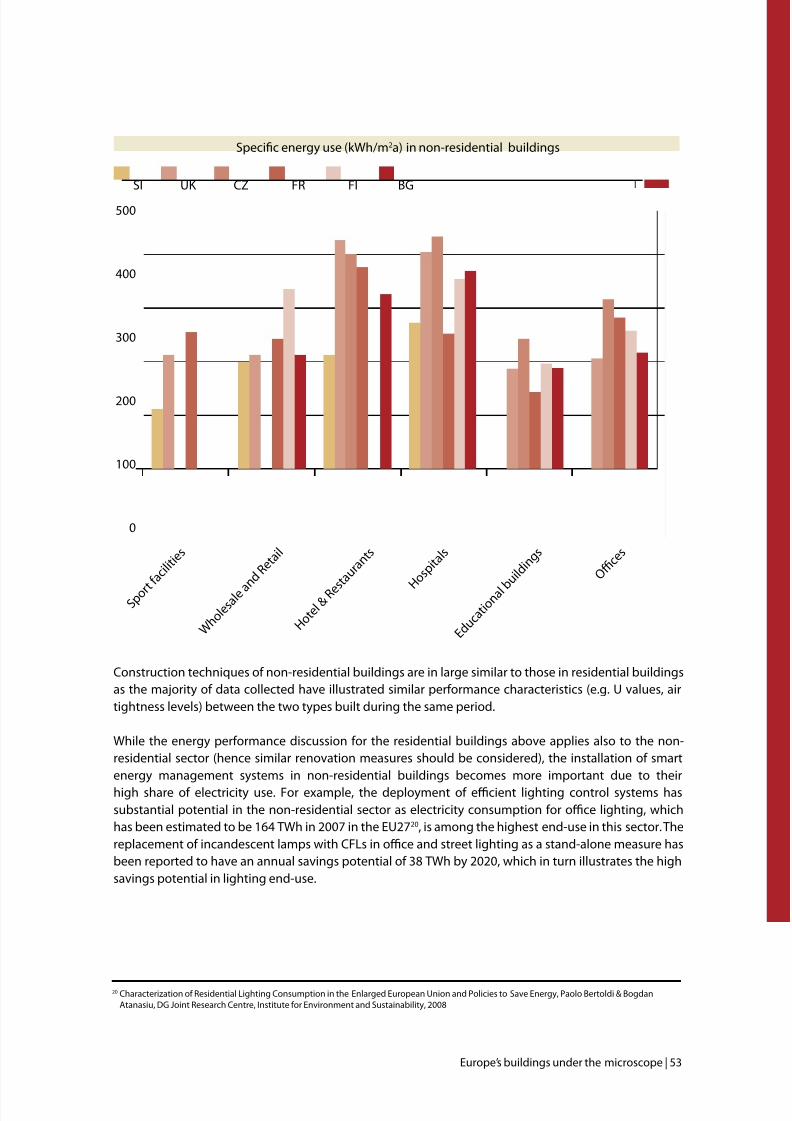

The average specic energy consumption in the non-residential sector is 280kWh/m2 (covering allend-uses) which is at least 40% greater than the equivalent value or the residential sector. In the non-residential sector, electricity use over the last 20 years has increased by a remarkable 74%.

Energy mix in residential buildings by regio

Average nal consumption levels or heating (kWh/(m2a)) o single amily homes by construction year

Germany

300

250

200

150

100

50

0

1 9 1 8

1 9 4 8 1 9

5 7 1 9

6 8 1 9

7 8 1 9

8 3 1 9

8 7 1 9

9 5 2 0

0 5 2 0

1 0

225246250

187

159156176

8094

53

Portugal

B e o r e

1 9 5 0

1 9 5 0

- 5 9

1 9 6 0

- 6 9

1 9 7 0

- 7 9

1 9 8 0

- 8 9

2 0 0 0

- 0 5

2 0 0 6

- 1 0

1 9 9 0

- 9 9

200 200 195

140 130120 110

68

250

200

150

100

50

0

Bulgaria

300

250

200

150

100

50

0

1 9 4 5

1 9 4 6

- 6 0

1 9 6 0

- 8 0

1 9 8 1

- 9 0

1 9 9 1

- 0 0

2 0 0 5

- n o w

2 0 0 1

- 0 4

228237 255

230

167131

101

South

Biomass 27%

Electricity 18%

Oil 32%

Gas 23%

Central & East

Biomass 20%

District Heat 29%

Coal 41%

Gas 7%

Oil 3%

Electricity 1%

North & West

Gas 39%

Oil 20%

Electricity 13%

Biomass 21%

LPG, DH other RES 6%

Coal 1%

2 Data extracted rom Eurostat: http://epp.eurostat.ec.europa.eu

Source: BPIE survey

Source: Eurostat

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 11/132

Europe’s buildings under the microscope | 11

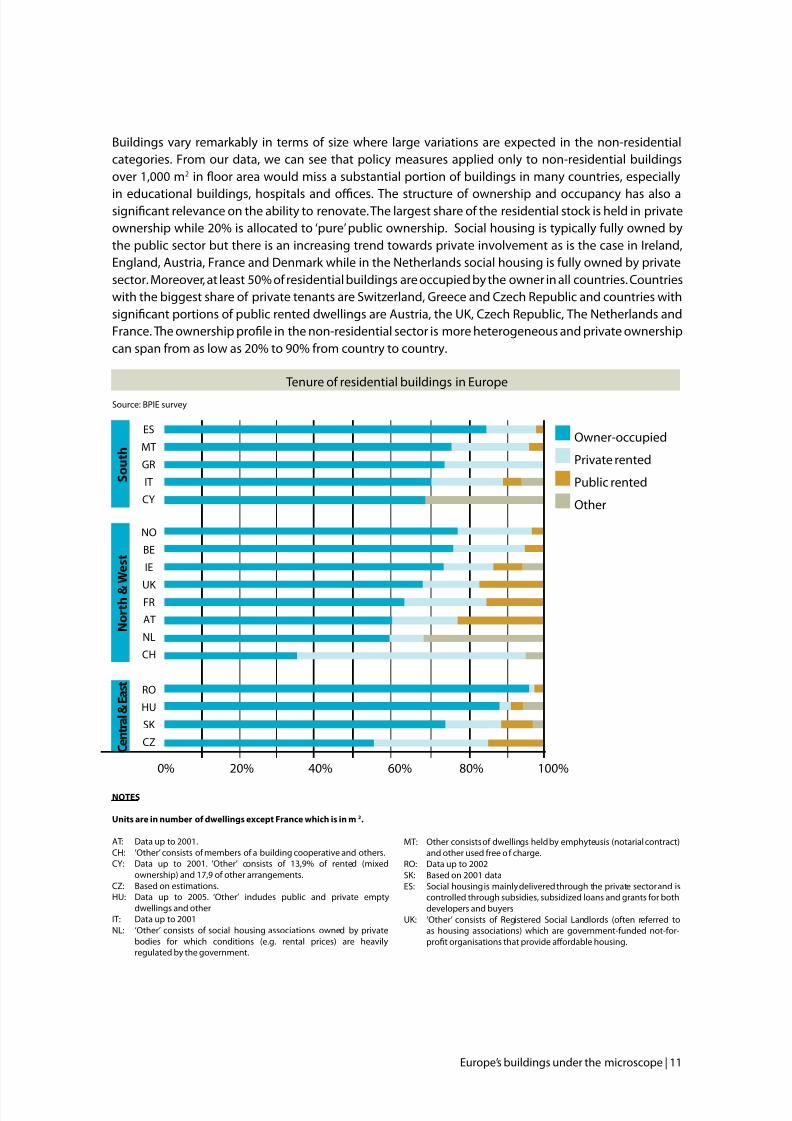

Buildings vary remarkably in terms o size where large variations are expected in the non-residentialcategories. From our data, we can see that policy measures applied only to non-residential buildingsover 1,000 m2 in oor area would miss a substantial portion o buildings in many countries, especially

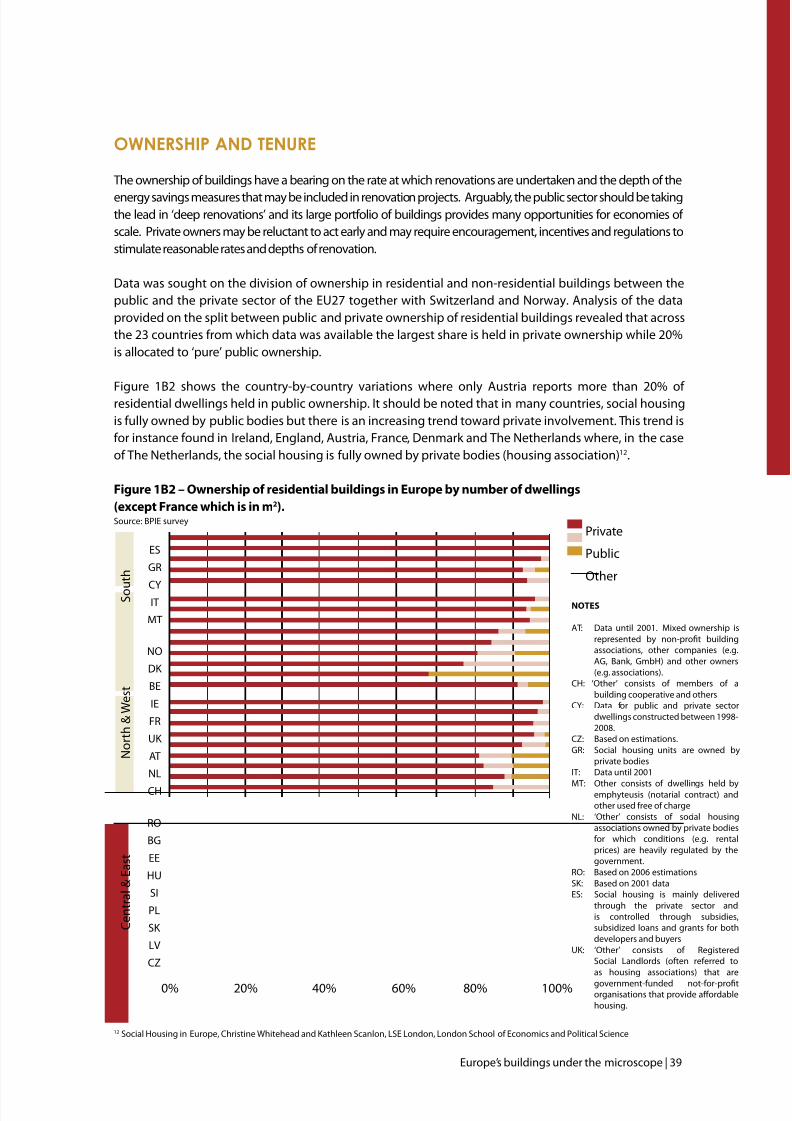

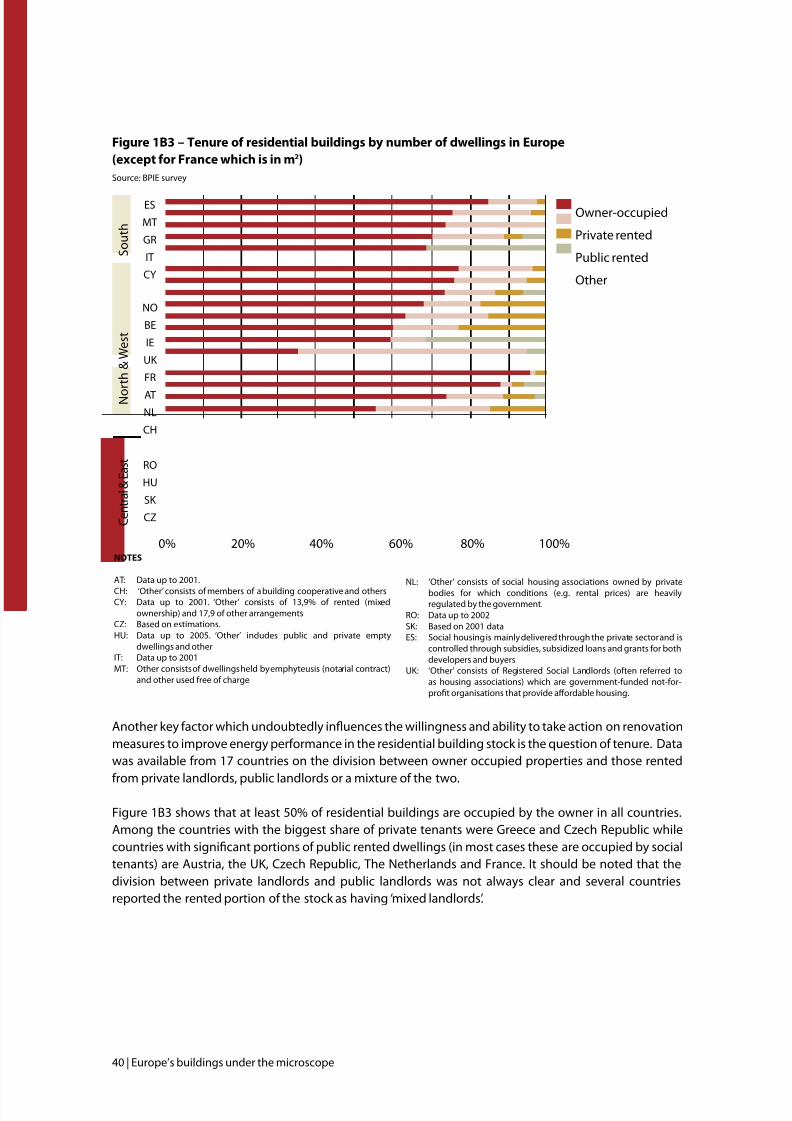

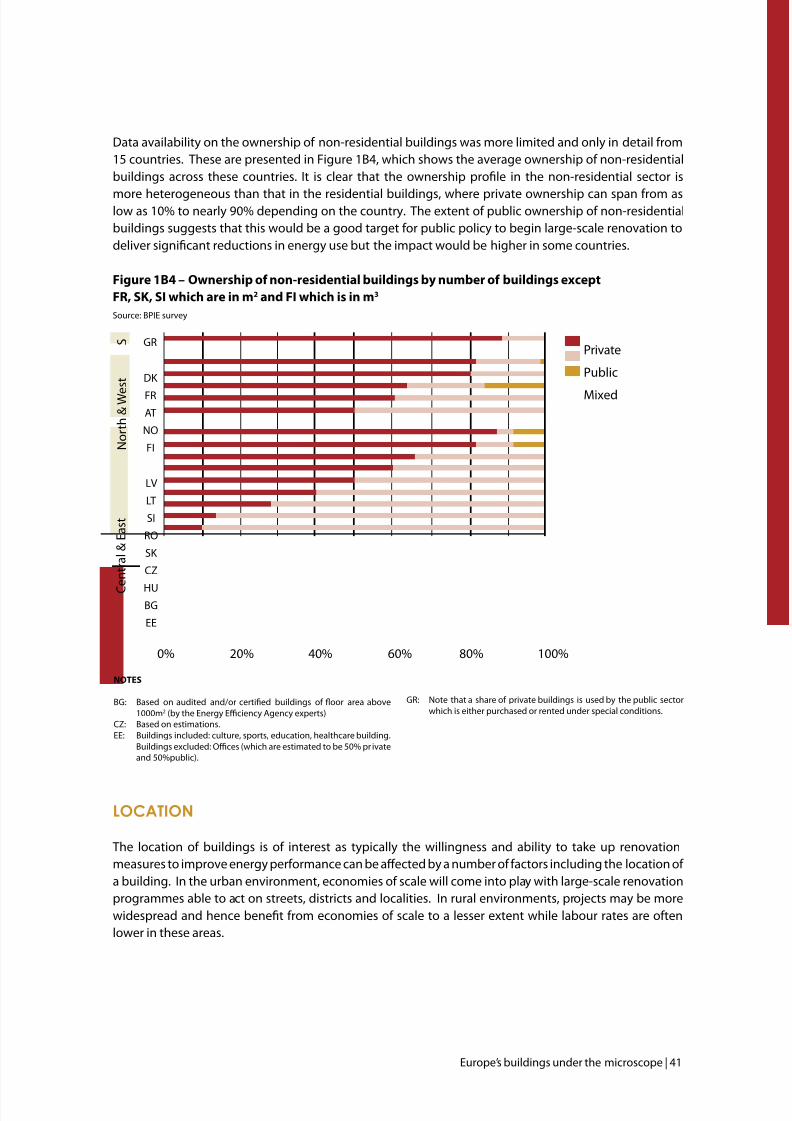

in educational buildings, hospitals and oces. The structure o ownership and occupancy has also asignicant relevance on the ability to renovate. The largest share o the residential stock is held in privateownership while 20% is allocated to ‘pure’ public ownership. Social housing is typically ully owned bythe public sector but there is an increasing trend towards private involvement as is the case in Ireland,England, Austria, France and Denmark while in the Netherlands social housing is ully owned by privatesector. Moreover, at least 50% o residential buildings are occupied by the owner in all countries. Countrieswith the biggest share o private tenants are Switzerland, Greece and Czech Republic and countries withsignicant portions o public rented dwellings are Austria, the UK, Czech Republic, The Netherlands andFrance. The ownership prole in the non-residential sector is more heterogeneous and private ownershipcan span rom as low as 20% to 90% rom country to country.

Tenure o residential buildings in Europe

NOTES

Units are in number o dwellings except France which is in m2.

AT: Data up to 2001.CH: ‘Other’ consists o members o a building cooperative and others.CY: Data up to 2001. ‘Other’ consists o 13,9% o rented (mixed

ownership) and 17,9 o other arrangements.CZ: Based on estimations.HU: Data up to 2005. ‘Other’ includes public and private empty

dwellings and otherIT: Data up to 2001NL: ‘Other’ consists o social housing associations owned by private

bodies or which conditions (e.g. rental prices) are heavilyregulated by the government.

MT: Other consists o dwellings held by emphyteusis (notarial contract)and other used ree o charge.

RO: Data up to 2002SK: Based on 2001 dataES: Social housing is mainly delivered through the private sector and is

controlled through subsidies, subsidized loans and grants or bothdevelopers and buyers

UK: ‘Other’ consists o Registered Social Landlords (oten reerred toas housing associations) which are government-unded not-or-prot organisations that provide afordable housing.

Source: BPIE survey

Owner-occupied

Private rented

Public rented

Other

0% 20% 40% 60% 80% 100%

S o u t h

N o r t h &

W e s t

C e n t r a l & E a s t

ES

MT

GR

IT

CY

NO

BE

IE

UK FR

AT

NL

CH

RO

HU

SK

CZ

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 12/132

12 | Europe’s buildings under the microscope

the europeAn policy scene

There are many reasons why investments in energy saving measures in buildings are oten overlooked,

rejected or only partially realised. Experience over several decades has identied numerous barriers thathinder energy saving investments. Financial, institutional and administrative, awareness/inormation andsplit incentives are the main categories o barriers identied by the BPIE survey which have a particularimpact on existing buildings. Although nancial barriers were one o the highest ranking barriercategory among the country responses, alternative investments are in many cases preerred to energysaving measures due to the lack o awareness, interest or in act, ‘attractiveness’ o energy eciency asan investment option. For the market to work well, correct and appropriate inormation is essential.Ambitious renovations comprise a major decision and can only work i the right advice is available orthe consumer. In addition, energy eciency service industries should be ully capable o delivering thosemeasures; and ultimately sucient satisaction levels should be guaranteed or the consumer. The splitincentive is probably the most long-lasting barrier, particularly due to the complex structure o occupancyboth in terms o the residential and non-residential sector.

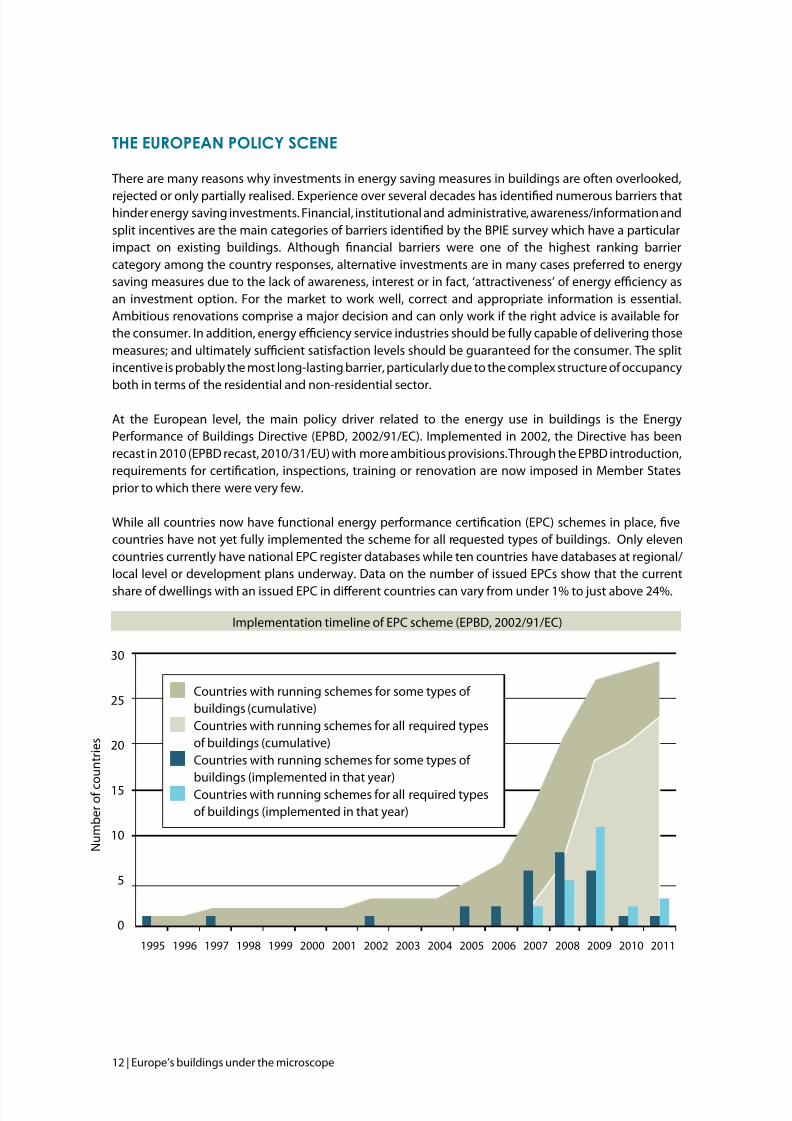

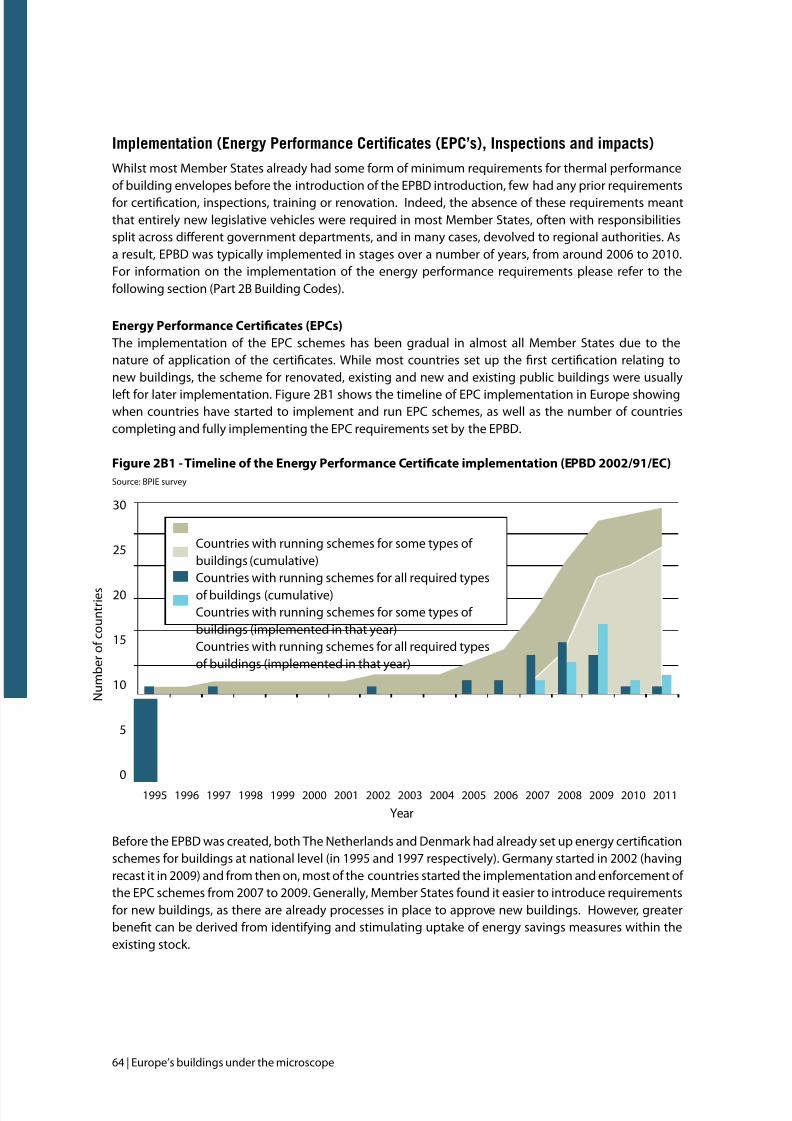

At the European level, the main policy driver related to the energy use in buildings is the EnergyPerormance o Buildings Directive (EPBD, 2002/91/EC). Implemented in 2002, the Directive has beenrecast in 2010 (EPBD recast, 2010/31/EU) with more ambitious provisions. Through the EPBD introduction,requirements or certication, inspections, training or renovation are now imposed in Member Statesprior to which there were very ew.

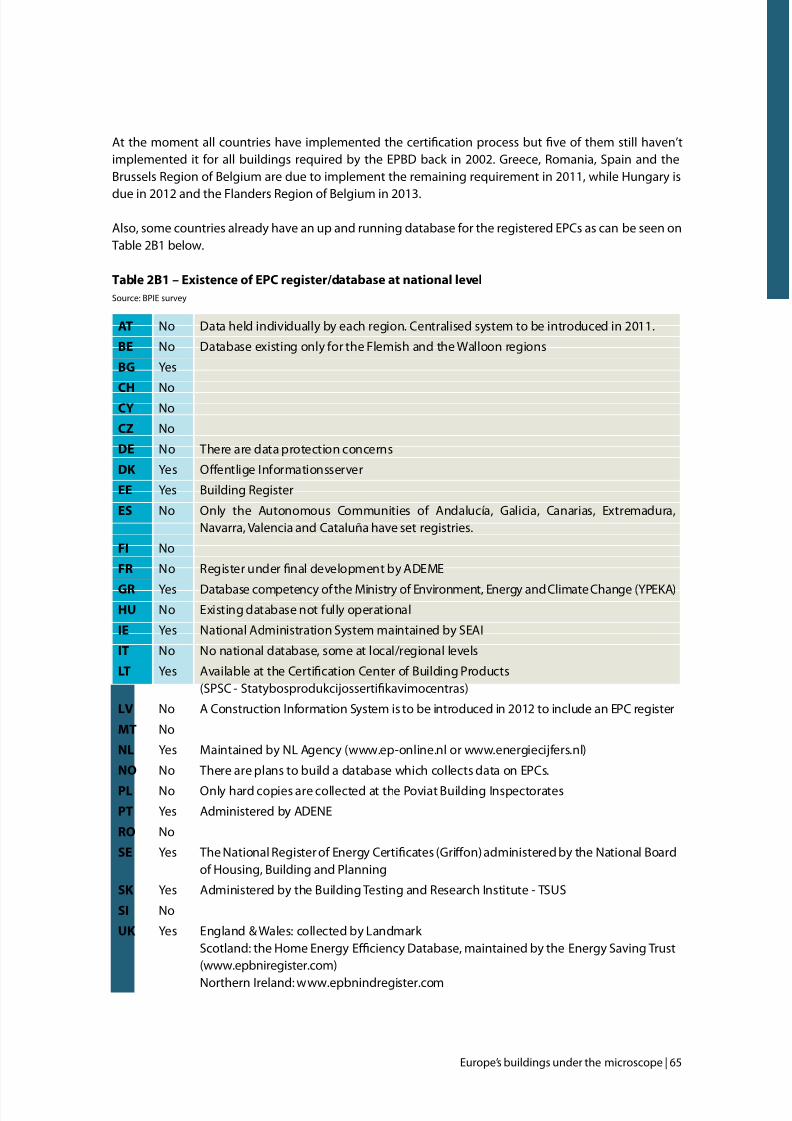

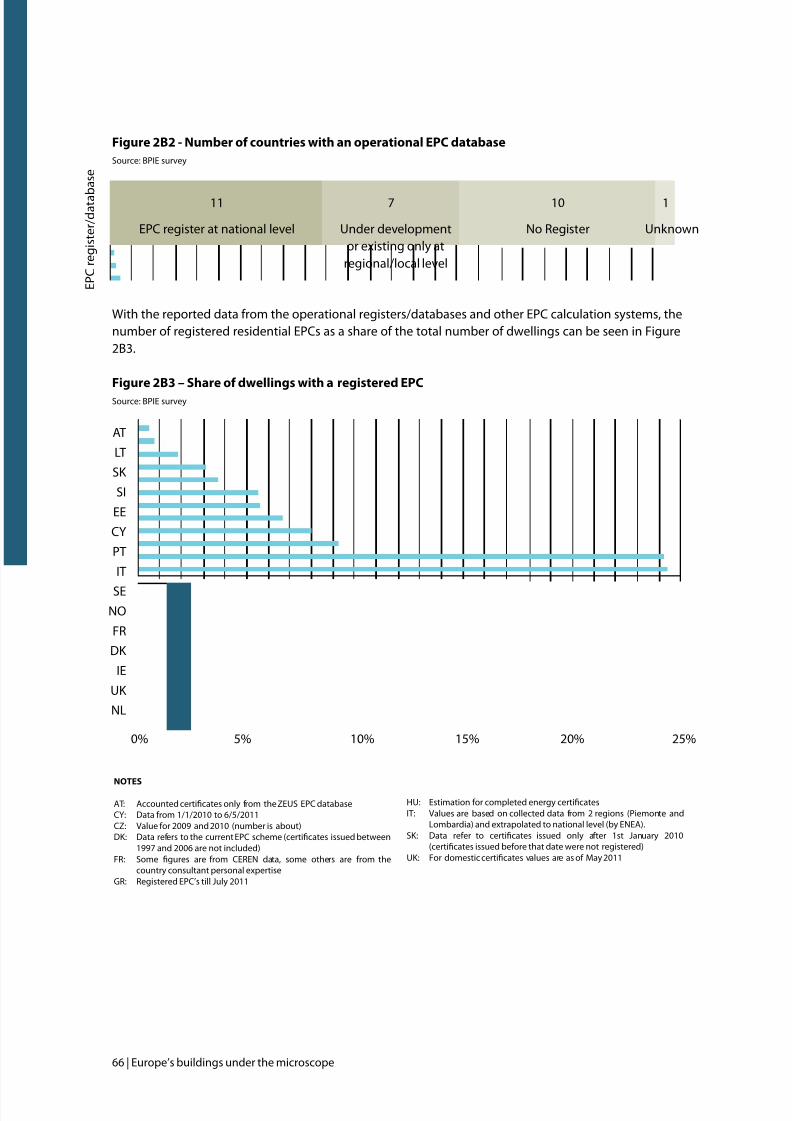

While all countries now have unctional energy perormance certication (EPC) schemes in place, vecountries have not yet ully implemented the scheme or all requested types o buildings. Only elevencountries currently have national EPC register databases while ten countries have databases at regional/local level or development plans underway. Data on the number o issued EPCs show that the current

share o dwellings with an issued EPC in diferent countries can vary rom under 1% to just above 24%.

Implementation timeline o EPC scheme (EPBD, 2002/91/EC)

30

25

20

15

10

5

0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

N u m b e r o c o u n t r i e s

Countries with running schemes or some types o buildings (cumulative)

Countries with running schemes or all required typeso buildings (cumulative)

Countries with running schemes or some types o buildings (implemented in that year)

Countries with running schemes or all required typeso buildings (implemented in that year)

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 13/132

Europe’s buildings under the microscope | 13

The absence o previous requirements in most Member States meant that entirely new legislative vehicleswere required and consequently that the rst EPBD was typically implemented in stages over a number o years, rom around 2006 to 2010. Despite the act that signicant developments happened over the last

years, current EU legislation only partially covers the eld o buildings renovation. The EPBD stipulates theimplementation o energy saving measures only in case o deep renovation o the building without speciyingthe depth o renovation measures. It is clear that more targeted measures are required or ostering the deeprenovation o the existing building stock.

A key driver or implementing energy eciency measures are the building energy codes, through whichenergy-related requirements are incorporated during the design or retrot phase o a building. While severalMember States had some orm o minimum requirements or thermal perormance o building envelopesin the 1970s, the EPBD was the rst major attempt requiring all Member States to introduce a generalramework or setting building energy code requirements based on a “whole building” approach. Examiningthe requirements set by each Member State, it is clear that large variations exist in terms o the approach eachcountry has taken in applying building energy codes. In some countries two approaches exist in parallel, onebased on the whole building approach and the other one on the perormance o single elements. In others, thesingle element requirements act as supplementary demands to the whole building approach. In some casesthe requirements or renovating buildings can be as ambitious as the new build requirements. Major changesare expected through the application o the cost-optimality concept in energy perormance requirementsas introduced by the recast EPBD which should also gradually converge to nearly zero energy standards, arequirement or new buildings rom 2020 onwards. An appropriate level o enorcement compliance withbuilding energy codes should also be o concern and a point o attention or policy makers as it is necessary toensure that enough rigour and attention to detail are undertaken when applying energy eciency measures.

As Europe strives towards increasing building energy perormance, the role o available nancial programmesand innovative mechanisms become increasingly important. About 333 nancial schemes have been screened

through the BPIE survey. These cover a wide range o nancial instruments rom grants to VAT reduction andapply to a range o building types. The measures surveyed are encouraging, but many o them are only modestin their ambition. The major concern is that the use o nancial instruments today only achieves the business-as-usual case in Europe with very ew nancial instruments providing enough unding or deep renovations,and ultimately do not correspond to Europe’s 2050 aspirations.

Types o nancial programmes and incentives on the energy perormance o buildings

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 14/132

14 | Europe’s buildings under the microscope

There are steps underway to improve the availability o new nancing instruments. Innovative approachesinclude Energy Supplier Obligations, energy service companies, the use o EU Structural Funds more efectivelyand possible targets to renovate specic building sub-sectors (e.g. the proposal in the drat Energy Eciency

Directive to Member States to renovate a certain percentage o public buildings annually) which will requireMember States to “unlock” unding or such renovations.

the wAys forwArd

Building energy perormance needs to be signicantly improved in order to reduce overall energydemand and, importantly, reduce carbon dioxide emissions in line with the cost-efective potential andEurope’s GHG emissions objectives. The question or policymakers is how to proceed.

To help policy makers determine the appropriate way orward, a renovation model has been specicallydeveloped or this project. The scenarios illustrate the impact on energy use and CO

2

emissions at diferentrates (percentage o buildings renovated each year) and depths o renovation (extent o measuresapplied and size o resulting energy and emissions reduction) rom now up to 2050. The model hasassessed energy saved, CO

2saved, total investment required, energy cost savings, employment impact

and a range o cost-efectiveness indicators. These assessments allow policy makers the opportunityto ocus on what they consider the highest priorities. The model considers eatures such as the age o buildings and quality o building energy perormance. When considering the share o buildings that canundergo low energy renovation, a practical limit is applied in the residential and non-residential buildingsectors in the 2011 to 2050 timerame. This practical limit is afected by a number o considerations suchas demolitions, heritage buildings, recent renovations and new buildings. The model applies diferentdiscount rates, learning curves and uture energy prices (based on Eurostat and Primes orecasts) in orderto derive how costs will evolve rom now until 2050. Two decarbonisation pathways are considered, a

slow pathway based on what has been witnessed since 1990 and a ast pathway based on what is neededto achieve the levels o carbon reduction assumed in the EU 2050 Roadmap. The model was used to create scenarios with various speeds (slow, medium and ast) and depths o renovation (minor, moderate, deep and nearly zero energy). All but one scenario assume that a buildingwill be renovated once between 2010 and 2050. The so-called two-stage scenario allows or a secondrenovation during the 2010-2050 period. Individual scenarios combine diferent speeds and depths,and are compared to a business-as-usual scenario, which assesses what would happen i there were nochanges rom the approach taken today.

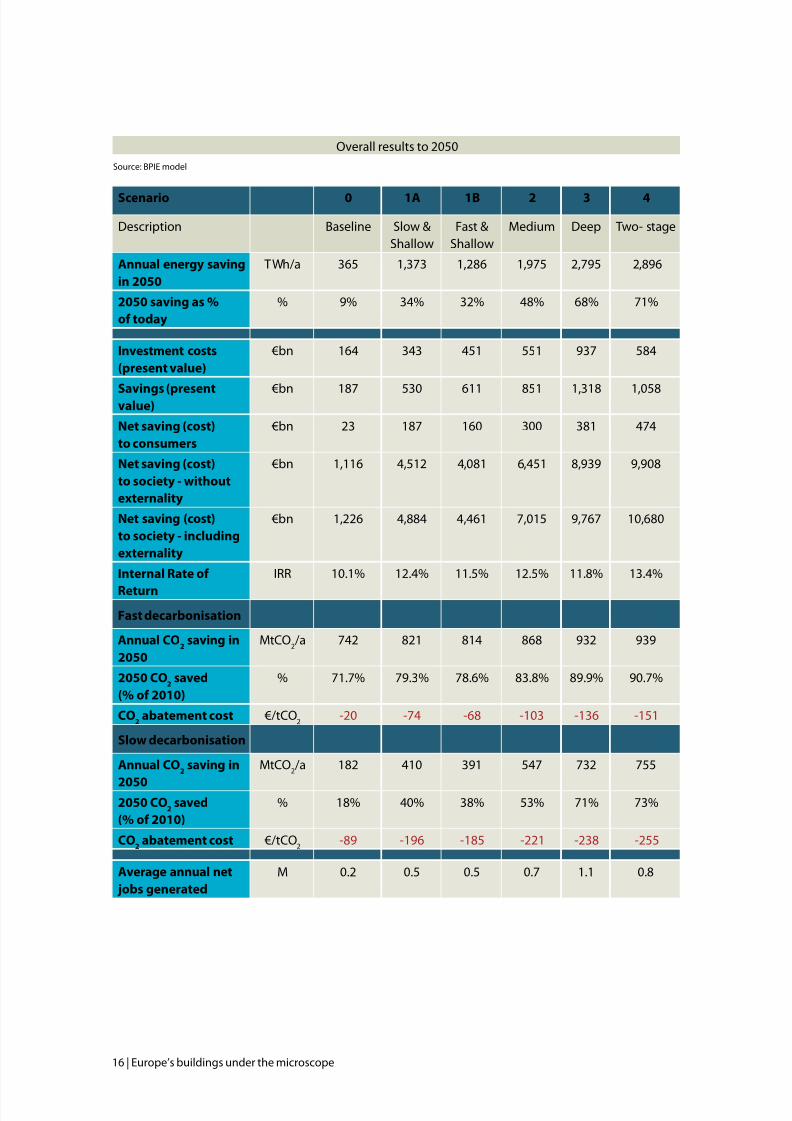

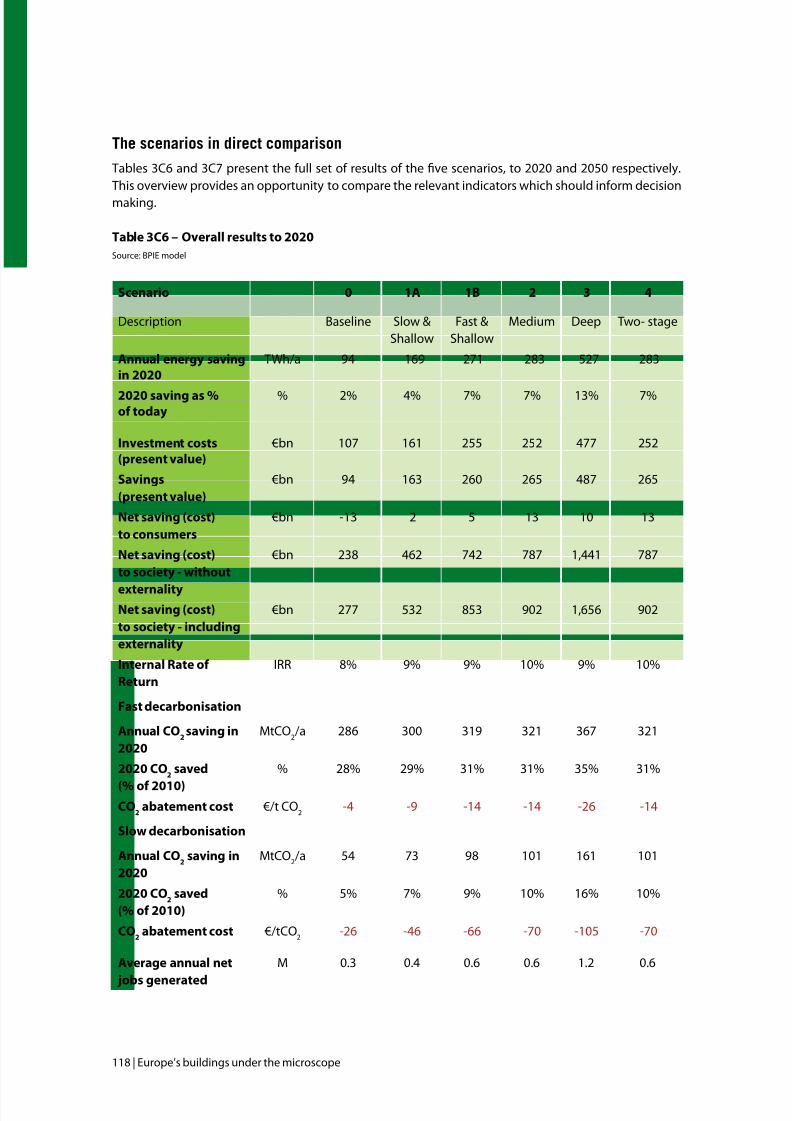

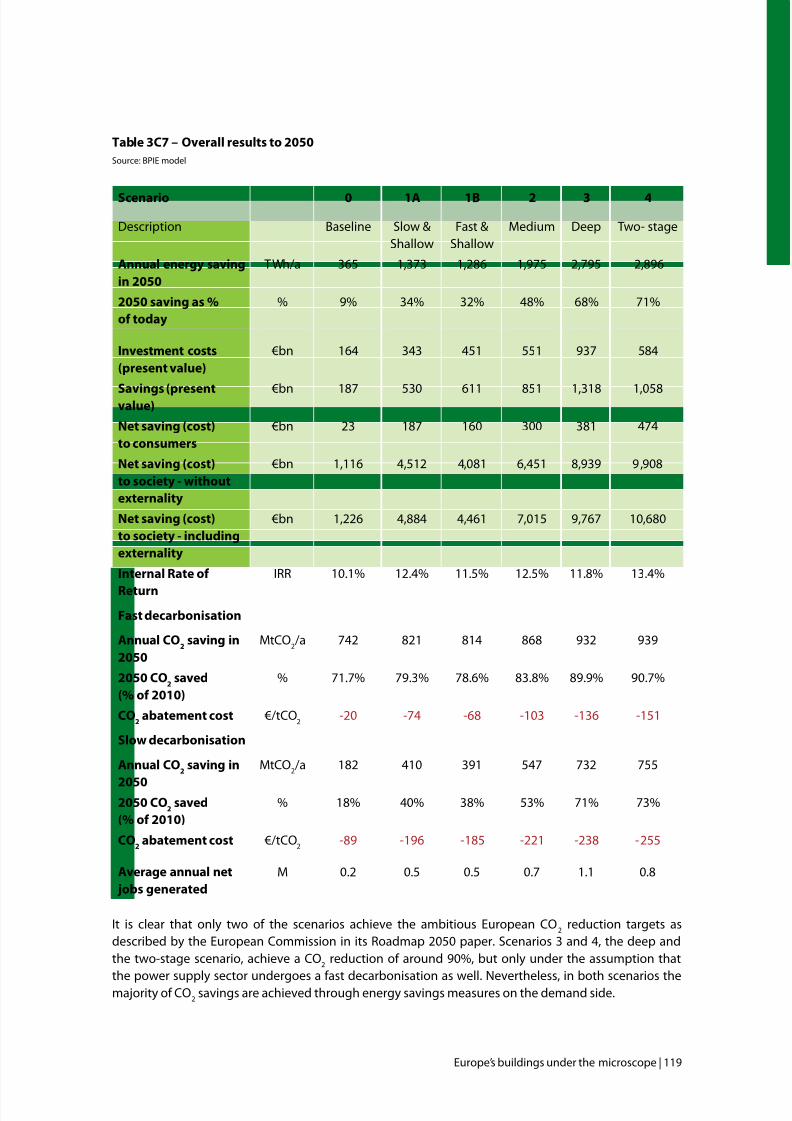

The results vary considerably as can be expected. Considering the results or 2020, the annual energysavings range rom 94 TWh in the business-as-usual case to 527 TWh or the most ambitious deepscenario (and 283 TWh or both the medium and two-stage scenarios). In 2050, the corresponding annualenergy savings o the deep and two-stage scenarios are 2795 TWh and 2896 TWh respectively while only365 TWh annual savings are achieved in the business-as-usual case.

The results look signicantly diferent or CO2

savings where the deep and two-stage scenarios are muchcloser in impact. Under the assumption o ast decarbonisation o electricity and ossil uels, the 2050savings o the deep and two-stage scenarios correspond to the 90% which are in line with the EuropeanCO

2reduction targets3. These levels o savings can only be achieved given that both renovation and

power sector decarbonisation strategies are adopted. Yet, there is a signicant diference in investmentcosts (on a present value basis). For the deep scenario the investment is €937 billion, while a signicantlylower €584 billion or the two-stage scenarios is needed.

3 as described by the European Commission in its Roadmap 2050 paper

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 15/132

Europe’s buildings under the microscope | 15

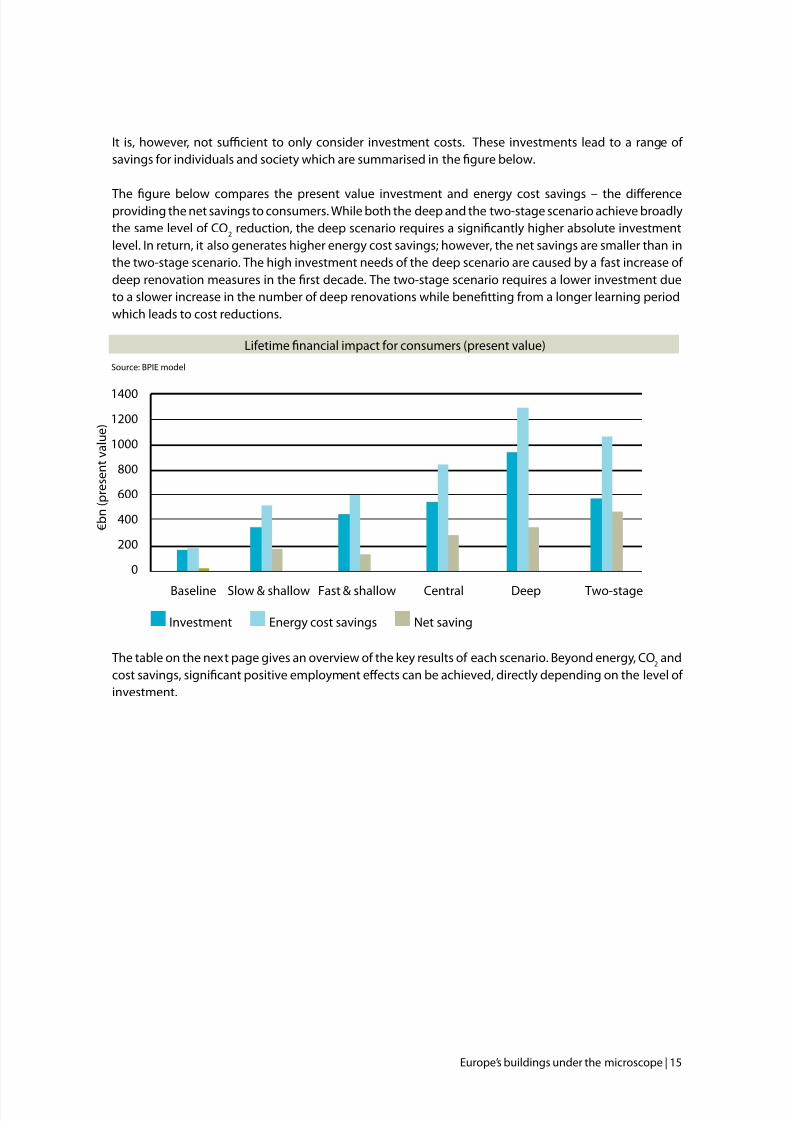

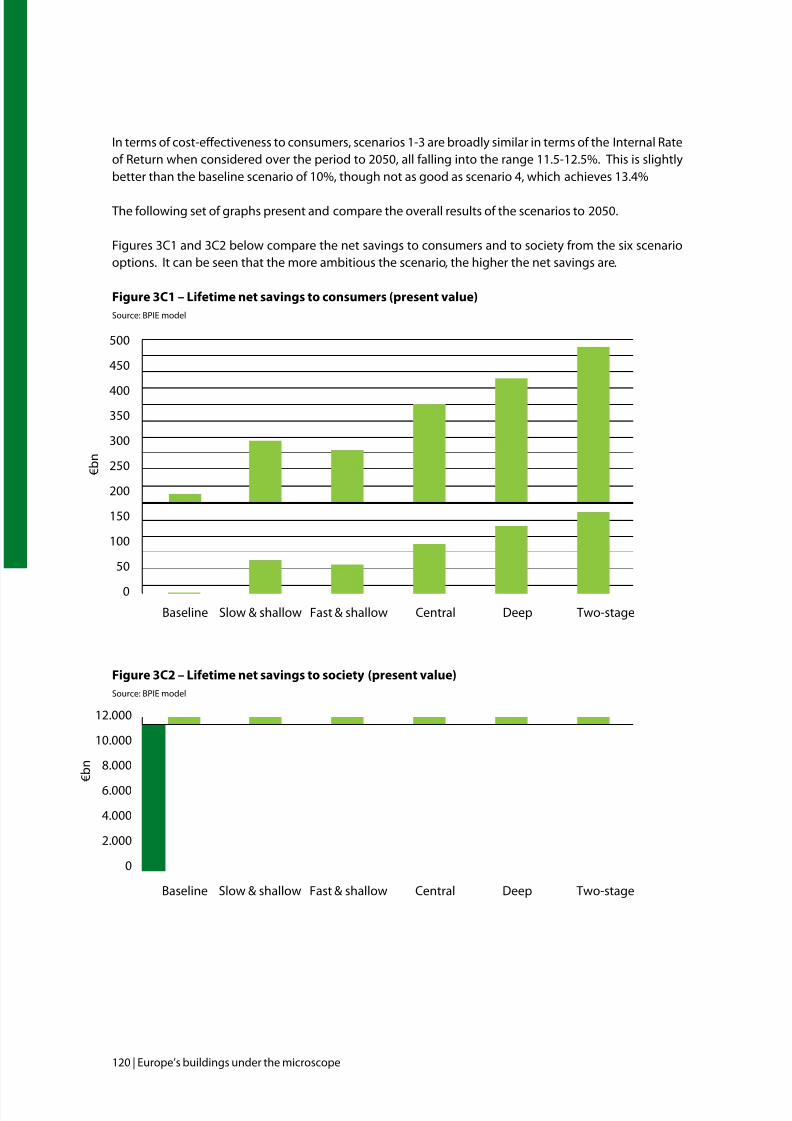

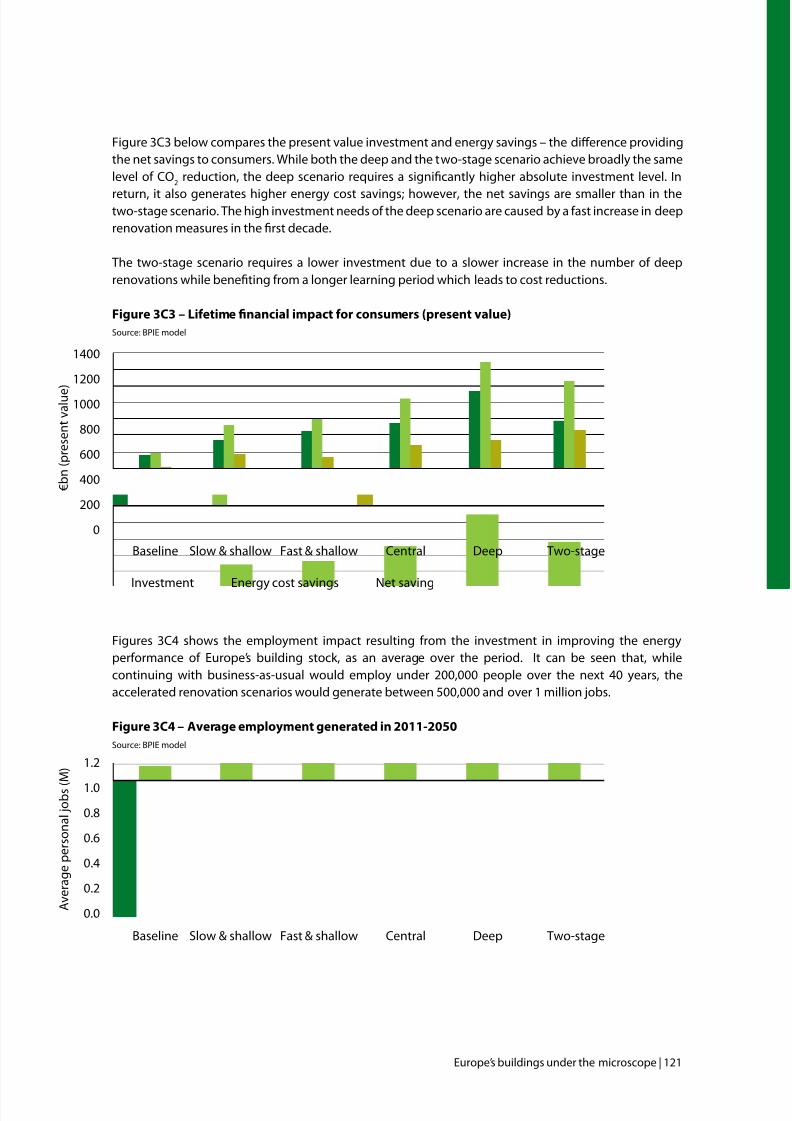

It is, however, not sucient to only consider investment costs. These investments lead to a range o savings or individuals and society which are summarised in the gure below.

The gure below compares the present value investment and energy cost savings – the diferenceproviding the net savings to consumers. While both the deep and the two-stage scenario achieve broadlythe same level o CO

2reduction, the deep scenario requires a signicantly higher absolute investment

level. In return, it also generates higher energy cost savings; however, the net savings are smaller than inthe two-stage scenario. The high investment needs o the deep scenario are caused by a ast increase o deep renovation measures in the rst decade. The two-stage scenario requires a lower investment dueto a slower increase in the number o deep renovations while benetting rom a longer learning periodwhich leads to cost reductions.

The table on the next page gives an overview o the key results o each scenario. Beyond energy, CO2

andcost savings, signicant positive employment efects can be achieved, directly depending on the level o investment.

Lietime nancial impact or consumers (present value)

1400

1200

1000

800

600

400

200

0

Baseline Slow & shallow Fast & shallow Central Deep Two-stage

€ b n ( p r e s e n t v a l u e )

Investment Energy cost savings Net saving

Source: BPIE model

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 16/132

16 | Europe’s buildings under the microscope

Scenario 0 1A 1B 2 3 4

Description Baseline Slow &Shallow

Fast &Shallow

Medium Deep Two- stage

Annual energy saving

in 2050

TWh/a 365 1,373 1,286 1,975 2,795 2,896

2050 saving as %

o today

% 9% 34% 32% 48% 68% 71%

Investment costs

(present value)

€bn 164 343 451 551 937 584

Savings (presentvalue) €bn 187 530 611 851 1,318 1,058

Net saving (cost)

to consumers

€bn 23 187 160 300 381 474

Net saving (cost)

to society - without

externality

€bn 1,116 4,512 4,081 6,451 8,939 9,908

Net saving (cost)

to society - including

externality

€bn 1,226 4,884 4,461 7,015 9,767 10,680

Internal Rate o

Return

IRR 10.1% 12.4% 11.5% 12.5% 11.8% 13.4%

Fast decarbonisation

Annual CO2

saving in

2050

MtCO2/a 742 821 814 868 932 939

2050 CO2

saved

(% o 2010)

% 71.7% 79.3% 78.6% 83.8% 89.9% 90.7%

CO2

abatement cost €/tCO2

-20 -74 -68 -103 -136 -151

Slow decarbonisation

Annual CO2

saving in

2050

MtCO2/a 182 410 391 547 732 755

2050 CO2

saved

(% o 2010)

% 18% 40% 38% 53% 71% 73%

CO2

abatement cost €/tCO2

-89 -196 -185 -221 -238 -255

Average annual net

jobs generated

M 0.2 0.5 0.5 0.7 1.1 0.8

Overall results to 2050

Source: BPIE model

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 17/132

Europe’s buildings under the microscope | 17

In all the scenarios, the estimated CO2

emission reduction by 2050 is determined by the energy savings butalso by the decarbonisation o the energy supply sector. It is interesting to note that in the deep and two-stage scenarios there is a 71-73% CO

2emission reduction even under the slow decarbonisation assumption,

a gure which is close to the CO2 emission reduction or the slow and shallow scenario under the astdecarbonisation assumption. This highlights the role o renovation measures in the decarbonisation strategy.The decarbonisation o the energy supply sector is signicantly eased by decreasing the energy demand o buildings and is importantly more sustainable. Moreover, the costs or decarbonising the energy generationsystem will be signicantly less i the consumption patterns o the building sector will dramatically reduce.

Each o the scenarios 1-4 represent a signicant ramping up in renovation activity compared to the currentsituation (i.e. the baseline scenario 0). When looked at purely in terms o the investment required, theserange rom around double the baseline level or scenario 1a, through to over 5 times the baseline level orthe deep scenario 3. These are signicant increases, but certainly achievable i governments across the EUwere to agree and implement respective policies and market stimulation mechanisms. The current practice isclearly not sucient to trigger a renovation wave across Europe which would deliver the societal, economicand environmental benets possible. At a time o rising unemployment and increased energy dependency,the employment and energy saving benets to consumers rom an accelerated renovation programme wouldprovide a welcome boost to many countries continuing to sufer economic diculties ollowing the creditcrunch.

The modelling exercise gives a clear indication that an ambitious renovation strategy or Europe’s buildings iseasible. Taking into consideration the three most relevant actors, i.e. achievement o CO

2reduction targets,

investment considerations and positive employment efects, it seems that the results o the two-stage scenarioprovide the best balance o these actors, comparing all scenarios. The two-stage scenario thereore illustratesa pathway which should inuence policy choices to stimulate the renovation o the European building stock.

For policy makers the challenge only begins at this point. The question now is how to break the policy inertiaand set the necessary policies in motion to achieve this. The complex nature o the buildings sector with itsmany actors in the value chain requires efective policy actions at both EU level and Member State level.

At EU level, the recast o the EPBD will have to be implemented in a way which secures large energy savingsand it will have to be monitored or revision at the earliest possible date. Other Directives, rom Ecodesign tothe Energy Eciency Directive proposed in June 2011, will have to be aligned to maximise ambition. At thesame time, Member States need to make signicant eforts to transpose EU regulation and to implement it ina way that stimulates deep renovation o the building stock.

Beyond policy regulation, nancing rameworks need to be efective and adequate. Innovative approaches areneeded since the initial up-ront investment costs or ambitious renovations can be a real barrier. Supportingmeasures at all levels o the building value chain, rom a well-trained workorce (rom designers to tradesmen),to a continuing and growing range o energy-ecient products and to efective awareness and inormationprogrammes are essential. These strategies are inter-connected and need to be careully designed to stimulatethe necessary growth o the European deep renovation market. The ollowing recommendations provide astrategic ramework and starting point or decision makers at both the EU and national level.

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 18/132

18 | Europe’s buildings under the microscope

ma eea

• Datacollection:harmonise national data collection systems relating to the energy perormance o buildings and ensure sucient data availability. A reliable and continuous data collection process is anecessary prerequisite or reliable policy making.

• Renoation roadmap: strengthen the existing legislation at EU level through binding measuresand establish a roadmap or the renovation o the building stock with interim and long term bindingtargets as well as monitoring and reporting plans. At Member State level, it is necessary to detail deeprenovation plans comprising regulatory, nancial, inormation and training measures, with renovationtargets based on the national nancial and technical potential and tailor-made roadmaps with diferentphases moving rom voluntary to binding measures.

• Financin: establish an EU Deep Renovation Fund (possibly via the European Investment Bank anddesigned or diferent building types) which can complement the national nancing schemes andshare the risks, ofering more nancial exibility and additional condence to the private investors.

EU expenditure or the renovation o the building stock (i.e. by Structural and Regional DevelopmentFunds) should introduce the minimum requirement or implementing measures at cost-optimal levels.The development o innovative nancial instruments at Member State level can trigger increasedprivate investment by providing guidelines or nancing, promoting best practice and stimulatingMember State cooperation;

• MemberStatepolicies:eliminate market barriers and administrative bottlenecks or the renovationo the building stock and to develop long-term comprehensive regulatory, nancial, educational andpromotional packages addressing all the macro-economic benets.

• Monitorin/compliance/enforcement: establish proper monitoring systems o compliance,enorcement and quality control processes through a qualied workorce or all policy packagesostering deep renovation.

• EneryPerformanceCerticates:strengthen the implementation o the buildings energy certicationand audit schemes which can increase the value o ecient buildings and can stimulate the real-estatemarket towards green investments.

• Public sector: ensure that the public sector takes a leading role in the renovation revolution asenvisaged by the drat Energy Eciency Directive, which should kick start the market or renovationand help bring costs down or private households and businesses.

• ESCOsandsainsuarantee:remove market barriers or the ESCOs and acilitate a aster and betterdevelopment o deep renovation programmes through regulatory rameworks, encouraging the setup and development o a well-unctioning energy services market which is not limited to commercialbuildings. An innovative guarantee system should be developed or the perormance o eciency

measures in order to provide condence or the quality level o renovation measures to consumers andinvestors.

• Trainin and education: increase the skills in the construction industry by ensuring appropriateramework conditions or the Internal Market o construction products and services, improvingresource eciency and environmental perormances o construction enterprises, and promoting skills,innovation and technological development.

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 19/132

Europe’s buildings under the microscope | 19

introductionA vitAl picture of the europeAn building stock

“If you cannot measure it, you cannot improve it”Sir William Thomson, Lord Kelvin

Buildings are at the centre o our social and economic activity. Not only do we spendmost o our lives in buildings, we also spend most o our money on buildings. The builtenvironment is not only the largest industrial sector in economic terms, it is also the

largest in terms o resource ow1

. Buildings are intrinsically linked to Europe’s societies,Europe’s economies, and their uture evolution.

Energy security and climate change are driving a uture that must show a dramatic improvement in theenergy perormance in Europe’s buildings. The 27 Member States have set an energy savings target o 20% by 2020, mainly through energy eciency measures. The European Union has also committed to80-95 % GHG reduction by 2050 as part o its roadmap or moving to a competitive low-carbon economyin 20502. Buildings currently represent almost 40% o total nal energy consumption and, thereore, canmake a crucial contribution to these targets.

In the Energy Eciency Plan 20113, the European Commission states that the greatest energy savingpotential lies in buildings. The minimum energy savings in buildings can generate a reduction o 60-80

Mtoe/a4 in nal energy consumption by 2020, and make a considerable contribution to the reductiono GHG emissions. This will be achievable only i buildings are transormed through a comprehensive,rigorous and sustainable approach.

The European policy ramework or buildings has been evolving since the early 1990s. A wide array o measures has been adopted across individual Member States to actively promote the better energyperormance o buildings. Ater 2002, the issue gained strong momentum when the Directive on EnergyPerormance o Buildings (EPBD) [Directive 2002/91/EC] was adopted. The EPBD was recast in 2010 tomake the goals more ambitious and to reinorce the implementation.5

As the Commission stated in its Communication proposing the 2010 revision: “The sector has signicant

untapped potential or cost efective energy savings.”6. Realising this potential will depend crucially onthe commitment o Member States, and the involvement o stakeholders rom government, industry andcivil society.

The European Union stretches over many diferent climate zones, landscapes and cultures. Some 501million inhabitants spread over 27 countries7 reside in a wide array o building types with an equally wide

1 Paul Hawken - The HOK Guidebook to Sustainable Design.2 Directive 2010/31 o the European Parliament and o the Council o 17 May 2010 on the energy perormance o buildings and its amendments (the

recast Directive entered into orce in July 2010, but the repeal o the current Directive will only take place on 1/02/2012).3 Energy Eciency Plan 2011, Communication rom the commission to the European Parliament, the council, the European economic and social

Committee and the committee o the regions, European Commission, 2011.4 Summary o the impact assessment accompanying document to the proposal or a recast o the energy perormance o buildings directive

(2002/91/EC).5 Directive 2010/31 o the European Parliament and o the Council o 17 May 2010 on the energy perormance o buildings and its amendments (therecast Directive entered into orce in July 2010, but the repeal o the current Directive will only take place on 1/02/2012).

6 COM(2008) 780 nal.7 The data collection and analysis also include Norway and Switzerland, two countries that work closely with the EU and implement much o its

legislation.

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 20/132

20 | Europe’s buildings under the microscope

range o thermal qualities, in a constantly expanding building stock. From styles o living – single-amilydwellings or multi-amily dwellings, or example – to policies or the construction o buildings, there aresignicant diferences between countries.

National approaches to monitoring the building stock have also evolved separately. Inormation is notonly needed to track the progress o policy implementation, better inormation and data are required tohelp develop a European pathway and roadmaps to more energy ecient buildings. In order to denethe energy and CO

2reduction potential, we need to study and evaluate the technical and economic

opportunities, easibilities and limits.

Indeed, it is a major obstacle to strong policy making at EU level that there is a lack o data on the buildingsector or Europe as a whole.

There has been signicant Europe-wide legislation on buildings and there are several orthcominginitiatives underway to improve the energy perormance o new and existing buildings. Yet, much o this is done with only a minimum o act-based knowledge, analysis and evidence. As strategies or theenergy perormance o buildings evolve and become more complex, policy makers need more concreteand precise acts to be able to make cross-country comparisons and to put in place the monitoringsystems that permit measurement o the progress o the various policy instruments.

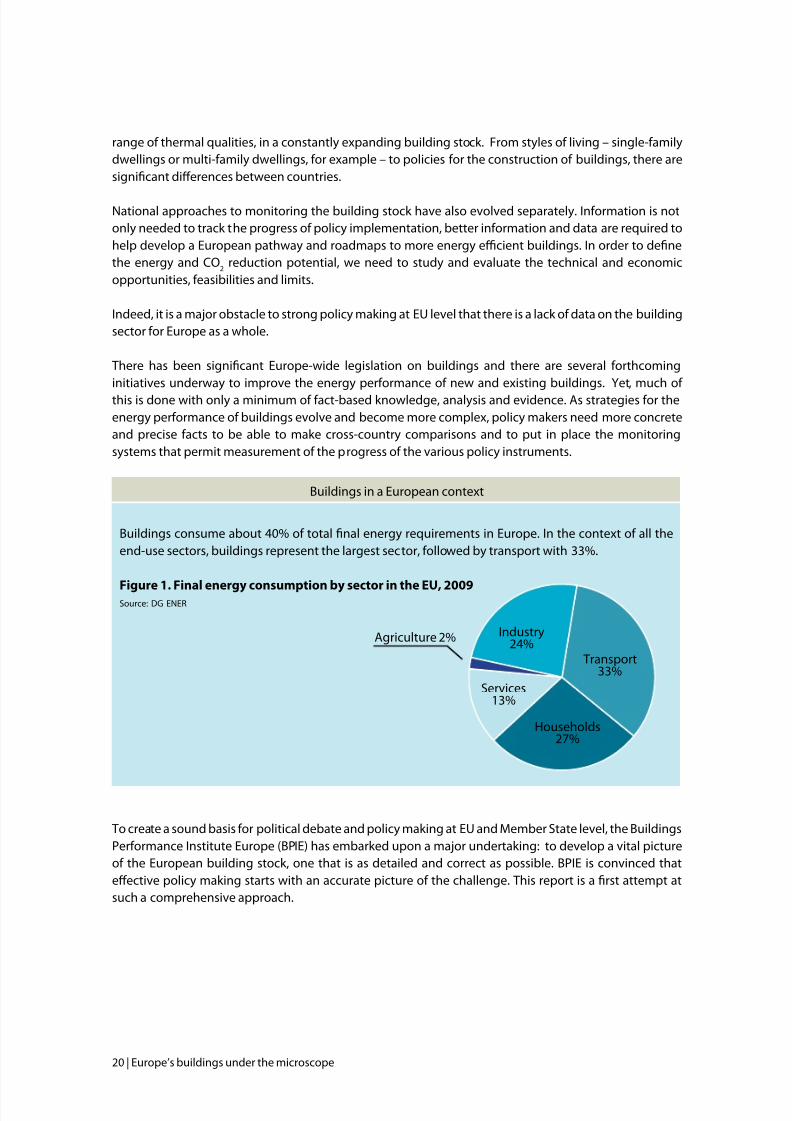

Buildings in a European context

Buildings consume about 40% o total nal energy requirements in Europe. In the context o all theend-use sectors, buildings represent the largest sector, ollowed by transport with 33%.

Figure 1. Final energy consumption by sector in the EU, 2009Source: DG ENER

To create a sound basis or political debate and policy making at EU and Member State level, the BuildingsPerormance Institute Europe (BPIE) has embarked upon a major undertaking: to develop a vital pictureo the European building stock, one that is as detailed and correct as possible. BPIE is convinced thatefective policy making starts with an accurate picture o the challenge. This report is a rst attempt atsuch a comprehensive approach.

Agriculture 2% Industry24%

Transport33%

Services13%

Households27%

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 21/132

Europe’s buildings under the microscope | 21

the chAllenge

Many experts agree that the most cost-efective way o meeting climate change targets is through improvedenergy eciency. At this point, there is growing acceptance o this principle, but there is still an imbalancebetween the resources devoted to energy supply options and energy demand-reduction options. The scenariosusually developed are designed to highlight the potential or improved energy eciency in buildings makinga cost-efective contribution to achieving climate targets.

Typically, energy eciency initiatives are crowded out by other more immediate priorities, in part becauseimproving energy eciency is a long-term policy commitment. In the buildings sector, policies are efectivenot over two or three years, but two or three decades. That is not easy to sustain. Today’s headlines includenancial crises in several EU Member States, wars in several countries and budget debates at national andEuropean levels. While they all seem like competing priorities, in act, improved energy eciency could makea positive contribution to solutions in many policy areas while actually increasing rather than decreasingavailable resources.

Why improve energy eciency in buildings?

The high level o energy consumption and GHG emissions in buildings in Europe makes this is anobvious sector to target in order to determine the potential and improve energy perormance. Whilethere has already been signicant efort to improve energy perormance in buildings, considerablepotential still remains, as was noted by the European Commission’s Communication on the proposalor the recast o the EPBD.

The justication or ocusing on the energy eciency in buildings can be summarised in the ollowingarguments that relate to both the individual’s point o view and the perspective o society as a whole:

• Securityofenergysupply;[Societal]• LowerGHGemissions,whichmeansamajorcontributiontoclimatechangestrategies;[Societal]

• Reducedenergycostsforconsumers,whichcanbeimportantinavoiding“fuelpoverty”(where

energy costs represent a disproportionate and unsustainable share o disposable income); [Private]• Cheaperthaninvestinginincreasedenergycapacity;[Societal]

• Improvedcomfort;[Private]

• ContributiontotherehabilitationofcertainbuildingtypesinthenewMemberStatesofCentral

and Eastern Europe; [Both]• Amajorcontributiontotheobjectiveofsustainabledevelopment,whichisaformalcommitment

o European countries; [Societal] and• Improvingenergyeciencyinbuildingsisimportanttothebuildingsenergyserviceindustries

that are important employers in Europe. [Both]

Any assessment o the costs and benets o building energy perormance must account or the ullrange o benets at both individual and societal level – which is oten dicult to estimate.

One major challenge is changing the mind-set concerning buildings. I the building sector is tosignicantly contribute to the 80-95% GHG reduction target or 2050, each building, on average, willhave to demonstrate very low carbon emission levels and consume very low energy in the context o adecarbonised power sector. For most o Europe’s buildings, that probably means improving the currentaverage energy consumption by a actor our or ve and the installation o renewables. For some it couldeven mean a actor 10 improvement. This may be hard to imagine but is denitely doable.8

8 The IEA analytical work related to polic y recommendations show this could be both possible and economically rational. This has been presented,or instance at Climate Change: Global Risks, Challenges and Decisions, IOP Con. Series: Earth and Environmental Science 6 (2009) in the paper“Global policy or dramatic reduction o energy consumption in bui ldings – Factor 3 is both possible and economic rational”, by Jens Laustsen,International Energy Agency IEA.

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 22/132

22 | Europe’s buildings under the microscope

Supporters o energy eciency need better arguments which will encourage both the private and publicsectors to take more interest in improving energy eciency and to explain how this paradigm shit canoccur. The main objectives o this study are to give policy-makers the acts and ofer the arguments to

make the case persuasively, and to provide useul data input to researchers who should base any politicaldiscussion upon science-based insights.

structure

This report has three parts.

Part 1 surveys 27 Member States, together with Norway and Switzerland, examining the oor space areao residential and non-residential buildings, building typologies, characteristics and energy perormanceo current stock. The inormation is drawn rom the statistical oces o national administrations and willbe presented in a orm that permits European comparisons and analysis. There are inevitably gaps, as

certain administrations have not made a priority o this kind o data collection (c.. Methodology chapter).

Part 2 provides detailed inormation and analysis relating to current barriers, the EPBD implementation,the European building codes and major programmes that are designed to improve energy perormancein buildings.

In Part 3 the available data were used to develop and assess the energy perormance scenarios orthe buildings sector in Europe with the aim o illustrating potential energy savings and CO

2reduction

pathways, reecting the EU’s 20% energy saving target or 2020, as well as the EU’s long term 80-95%GHG emission reduction target or 2050.

The scenarios describe the impact o building retrot strategies to achieve the 2020 and 2050 targets.The scenarios are built on diferent renovation rates and depths and illustrate the impact o diferentambition levels regarding the European environment and economy.

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 23/132

Europe’s buildings under the microscope | 23

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 24/132

24 | Europe’s buildings under the microscope

mEthodology

BPIE has recently screened all EU27 countries together with Switzerland and Norwaywith the aim o collecting existing data related to buildings and building policies. Theexercise has been undertaken using a team o experts in each Member State plus Norwayand Switzerland. The data collected were mainly extracted rom ocial statistics andstudies at Member State level supported by expert estimations wherever ocial datawere unavailable. The inormation was gathered in the orm o a questionnaire whosestructure comprised ve principal levels:

Background

LegalFinancialTechnicalMonitor

The data have been used to give a resh and up-to-date picture o where we stand in terms o the energyperormance o our buildings and orm the basis upon which our scenarios are built. Through the surveycarried out by BPIE, inormation on the typology, characteristics (such as age, size, and ownership prole)and energy perormance o the building stock have been collected or the EU27 countries together withNorway and Switzerland. The dataset represents one o the most comprehensive assembled in Europeto date and ranges rom residential to non-residential buildings where the ollowing categories wereconsidered:

(a) Single amily houses(b) Apartment blocks(c) Oces(d) Educational buildings(e) Hospitals() Hotels and restaurants(g) Sports acilities(h) Wholesale and retail trade services buildings(i) Other types o energy-consuming buildings

Data have been gathered on the oor area o the building stock where 25 countries reported residentialand 19 reported non-residential oor area data in ull. A urther our countries reported partial data orthe oor area o non-residential buildings. The reported totals represented 92% o the total oor area inthe countries looked at and the nal 8% have been estimated. For the latter, estimates have been madeby taking the prevailing average across the dataset or oor area per person or the missing buildingcategory and multiplying this by the population o the country in question.

Care has been taken in the compilation o the data required to make additional estimations. For example,oor area data were reported at times in net oor area and other times in gross, net, useul or heated.Conversion actors were applied to aggregate all data in useul oor areas considering typical wallthickness levels as well as percentage oor space o buildings, which are non-heated and non-habitable

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 25/132

Europe’s buildings under the microscope | 25

areas. These actors were dened or diferent types o buildings. Comparisons were urther complicatedby inconsistent denitions o many building typologies where assumptions had to be made in order tobroadly divide the reported data in the above unction types. In some cases, appropriate division was not

possible. For example, some countries reported industrial buildings in “other types o energy consumingbuildings” while others did not. In those cases, it was not possible to extract or estimate the portion o industrial buildings in order to provide consistent inormation or this unction type across all countries.

Data have also been gathered in terms o the age, size, ownership (private/public), tenure (owneroccupied, private or social tenant) location (rural/urban) and typical energy perormance levels o thebuilding stock. Good responses have generally been obtained by several countries in residential stock while gaps in responses were more prominent in the characteristics o the non-residential stock.

the chAllenges for the future

As this is probably the rst attempt to draw together a comprehensive and detailed picture o theresidential and non-residential building stock throughout Europe, a number o issues have beenidentied, among which the two key issues are:

Commondenitionofoorarea:Countries oten have diferent approaches to the measurement o oor area which can includeexternal gross, internal gross, net, heated and treated parts o a building. The same term may nothave the same meaning or denition in diferent countries. Moreover, assuming that two countriesadopt the same denition, the diferent approaches or taking measurements (e.g. measuring theattic space) imply that comparing the resulting oor areas is dicult. For these reasons, it would behelpul to have agreement on a common measurement principle which should probably correspondto the concept o ‘treated’ oor area, reerring to the portion o the building treated with some ormo heating and/or cooling (but excluding areas such as plant rooms, car parks and other non-treatedspaces). Some have proposed that building volume is a better metric when dealing with treatedspace because it is the volume o air that is heated or cooled. A small number o countries collectdata on building volume and in any case it can be even more dicult to dene, especially in the non-residential sector with suspended ceilings and raised oors complicating the measurement.

Commonbuildincateories:Data were collected or this report using the above set o categories (a-i) or residential and non-residential buildings. Most countries were able to present data in the required ormat but severalwere only able to provide data broken down into nationally dened sets o categories. Agreementaround a common set o building categories with a clear set o denitions o what should be included

and excluded would make or more reliable and comparable data in the uture, especially or non-residential types.

Addressing the above issues would require in many cases changes to the databases that countries areusing and hence the underlying legislation. Although this would require considerable efort, monitoringand evaluating current policies related to buildings signiy the urgent need or more data on the buildingstock. I the above issues are addressed in an appropriate way without overcomplicating the additionalwork, the case would be urther reinorced or buildings being a driving sector or achieving the overallclimate targets set or the EU. Without a solid oundation o data, it is dicult to monitor the impact andultimately design efective policies.

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 26/132

26 | Europe’s buildings under the microscope

pArt 1 EuropE’s buildings todAy

“For strong policy making at EU and Member State levelit is key to establish an efcient monitoring system of theEuropean building stock assuring good data availabilityand data quality.”

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 27/132

Europe’s buildings under the microscope | 27

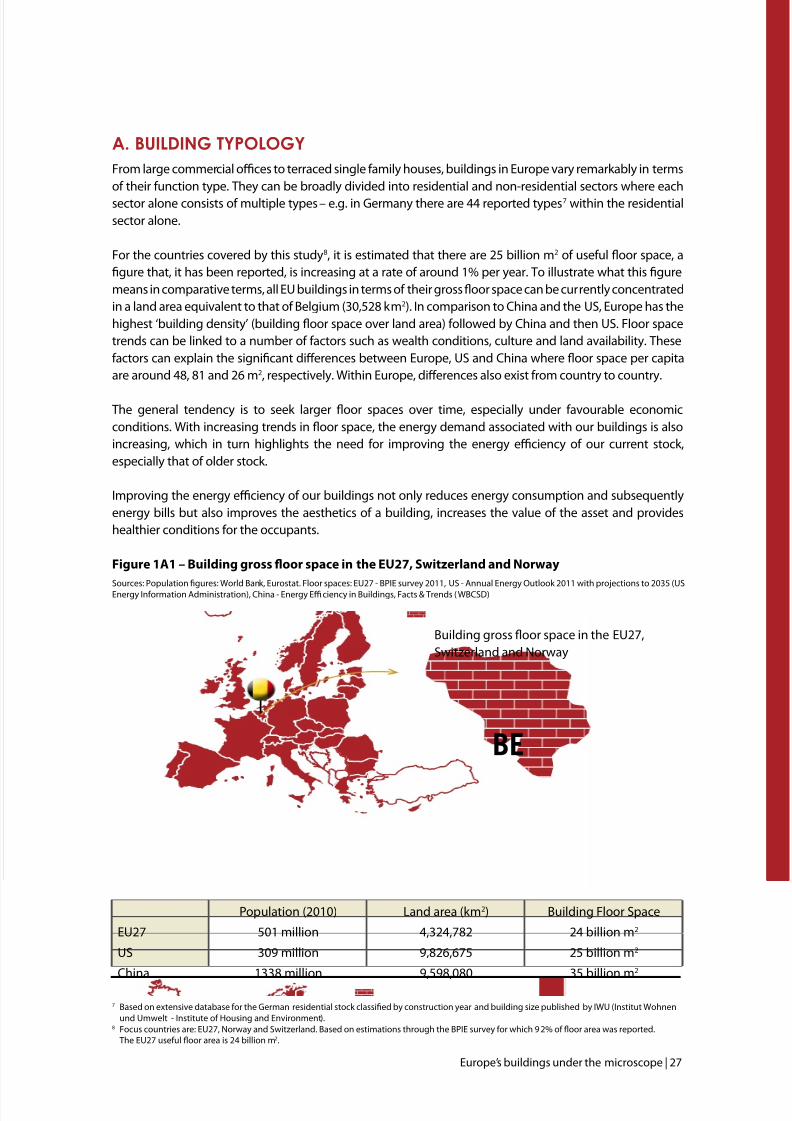

A. building typology

From large commercial oces to terraced single amily houses, buildings in Europe vary remarkably in termso their unction type. They can be broadly divided into residential and non-residential sectors where eachsector alone consists o multiple types – e.g. in Germany there are 44 reported types7 within the residentialsector alone.

For the countries covered by this study8, it is estimated that there are 25 billion m2 o useul oor space, agure that, it has been reported, is increasing at a rate o around 1% per year. To illustrate what this guremeans in comparative terms, all EU buildings in terms o their gross oor space can be currently concentratedin a land area equivalent to that o Belgium (30,528 km2). In comparison to China and the US, Europe has thehighest ‘building density’ (building oor space over land area) ollowed by China and then US. Floor spacetrends can be linked to a number o actors such as wealth conditions, culture and land availability. Theseactors can explain the signicant diferences between Europe, US and China where oor space per capitaare around 48, 81 and 26 m2, respectively. Within Europe, diferences also exist rom country to country.

The general tendency is to seek larger oor spaces over time, especially under avourable economicconditions. With increasing trends in oor space, the energy demand associated with our buildings is alsoincreasing, which in turn highlights the need or improving the energy eciency o our current stock,especially that o older stock.

Improving the energy eciency o our buildings not only reduces energy consumption and subsequentlyenergy bills but also improves the aesthetics o a building, increases the value o the asset and provideshealthier conditions or the occupants.

Figure 1A1 – Building gross oor space in the EU27, Switzerland and Norway

Sources: Population gures: World Bank, Eurostat. Floor spaces: EU27 - BPIE survey 2011, US - Annual Energy Outlook 2011 with projections to 2035 (USEnergy Inormation Administration), China - Energy Eciency in Buildings, Facts & Trends ( WBCSD)

7 Based on extensive database or the German residential stock classied by construction year and building size published by IWU (Institut Wohnenund Umwelt - Institute o Housing and Environment).

8 Focus countries are: EU27, Norway and Switzerland. Based on estimations through the BPIE survey or which 9 2% o oor area was reported.The EU27 useul oor area is 24 billion m2.

bE

Population (2010) Land area (km2) Building Floor Space

EU27 501 million 4,324,782 24 billion m2

US 309 million 9,826,675 25 billion m2

China 1338 million 9,598,080 35 billion m2

Building gross oor space in the EU27,Switzerland and Norway

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 28/132

28 | Europe’s buildings under the microscope

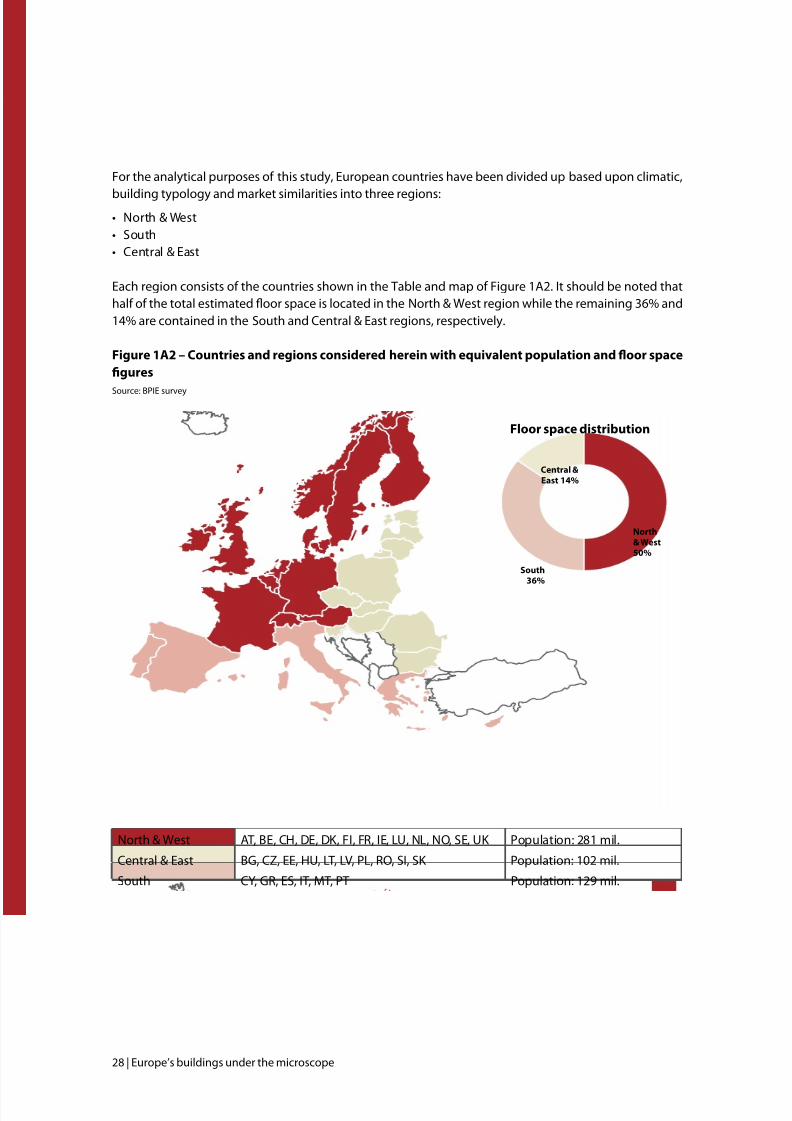

For the analytical purposes o this study, European countries have been divided up based upon climatic,

building typology and market similarities into three regions:• North&West

• South

• Central&East

Each region consists o the countries shown in the Table and map o Figure 1A2. It should be noted thathal o the total estimated oor space is located in the North & West region while the remaining 36% and14% are contained in the South and Central & East regions, respectively.

Figure 1A2 – Countries and regions considered herein with equivalent population and oor space

ures

Source: BPIE survey

North & West AT, BE, CH, DE, DK, FI, FR, IE, LU, NL, NO, SE, UK Population: 281 mil.

Central & East BG, CZ, EE, HU, LT, LV, PL, RO, SI, SK Population: 102 mil.

South CY, GR, ES, IT, MT, PT Population: 129 mil.

Floor space distribution

South36%

Central &East 14%

North& West50%

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 29/132

Europe’s buildings under the microscope | 29

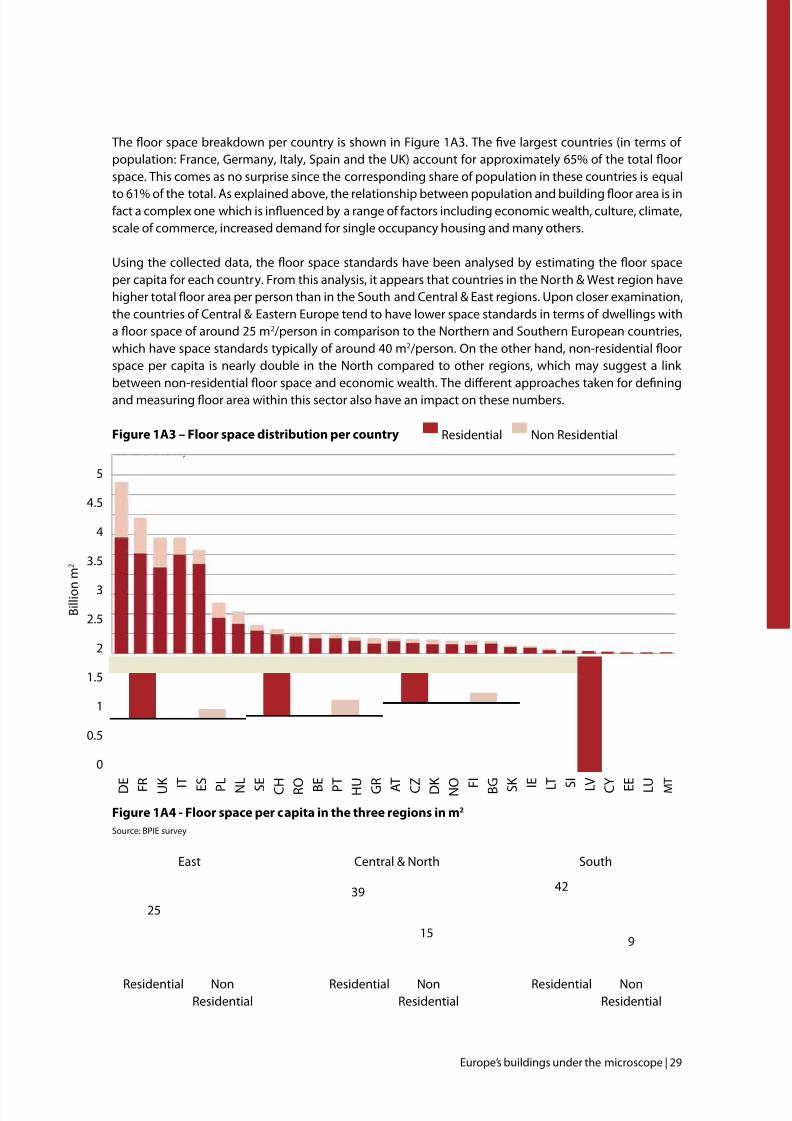

The oor space breakdown per country is shown in Figure 1A3. The ve largest countries (in terms o population: France, Germany, Italy, Spain and the UK) account or approximately 65% o the total oorspace. This comes as no surprise since the corresponding share o population in these countries is equal

to 61% o the total. As explained above, the relationship between population and building oor area is inact a complex one which is inuenced by a range o actors including economic wealth, culture, climate,scale o commerce, increased demand or single occupancy housing and many others.

Using the collected data, the oor space standards have been analysed by estimating the oor spaceper capita or each country. From this analysis, it appears that countries in the North & West region havehigher total oor area per person than in the South and Central & East regions. Upon closer examination,the countries o Central & Eastern Europe tend to have lower space standards in terms o dwellings witha oor space o around 25 m2/person in comparison to the Northern and Southern European countries,which have space standards typically o around 40 m2/person. On the other hand, non-residential oorspace per capita is nearly double in the North compared to other regions, which may suggest a link between non-residential oor space and economic wealth. The diferent approaches taken or deningand measuring oor area within this sector also have an impact on these numbers.

Figure 1A3 – Floor space distribution per country

Source: BPIE survey

Figure 1A4 - Floor space per capita in the three regions in m2

Source: BPIE survey

Residential

25

8

East

NonResidential

East

15

39

North & Central

Residential NonResidential

Central & North

9

42

South

Residential NonResidential

South

B i l l i o n

m 2

D E

F R U K I T

E S

P L

N L

S E

C H R O B E

P T

H U G R A T

C Z D K N O F

I

B G S K I E

L T

S

I

L V C Y E E

L U M T

Residential Non Residential

5

4.5

4

3.5

3

2.5

2

1.5

1

0.5

0

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 30/132

30 | Europe’s buildings under the microscope

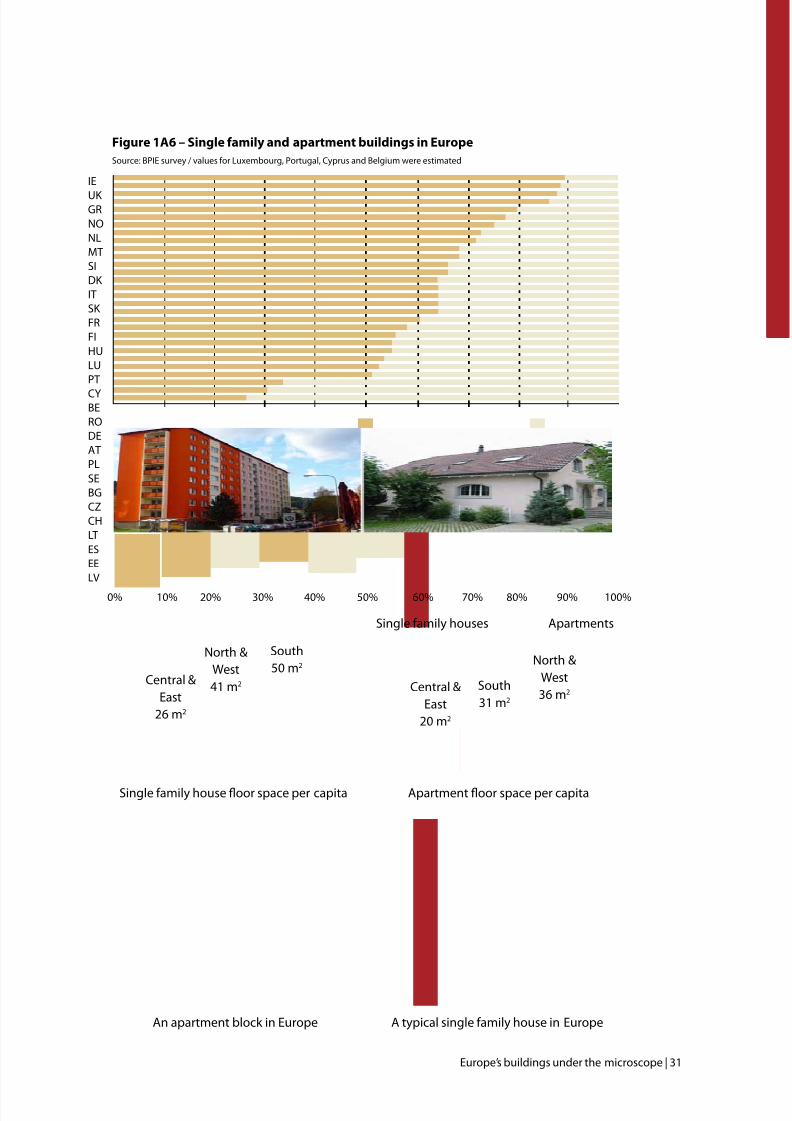

residentiAl buildings

The residential stock is the biggest segment with an EU oor space o 75% o the building stock (Figure1A5). Within the residential sector, diferent types o single amily houses (e.g. detached, semi-detachedand terraced houses) and apartment blocks are ound. Apartment blocks may accommodate severalhouseholds typically ranging rom 2-15 units or in some cases holding more than 20-30 units (e.g. socialhousing units or high rise residential buildings).

An analysis o this data indicates that, across the ocus countries in this study, 64% o the residentialbuilding oor area is associated with single amily houses and 36% with apartments.

Figure 1A5 – Residential oor space or the countries covered in the study

Source: BPIE survey

The split between the two main types o residential properties varies signicantly rom country to countryas shown in Figure 1A6.

Austria, Bulgaria, Czech Republic, Germany, Lithuania, Poland, Sweden and Switzerland could be said tohold more even portolios with similar oor areas or single amily houses and apartments.

Greece, Ireland, Norway and the UK have the smallest proportion o oor area o apartments in theresidential building stock, whilst Estonia, Latvia and Spain have the highest.

In terms o oor space per capita, the Central & East countries are among the countries with the lowestresidential space in terms o both single amily houses and apartment blocks.

North & West countries have the highest residential oor areas per capita compared to other regions.

Countries in the South have the highest single amily house oor space per capita which perhaps indicatesthe requency o holiday houses in those countries.

It is interesting to note that in all regions, the oor space standards in apartments are lower than in singleamily houses, a trend which perhaps reinorces the link between oor space and wealth conditions.

NonResidential

25%Residential

75%

Single amilyhouses

64%

Apartmentblocks

36%

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 31/132

Europe’s buildings under the microscope | 31

Single amily houses Apartments

Single amily house oor space per capita

Central &East

26 m2

North &West41 m2

South50 m2

Apartment oor space per capita

Central &East

20 m2

North &West36 m2

South31 m2

A typical single amily house in EuropeAn apartment block in Europe

Figure 1A6 – Single amily and apartment buildings in Europe

Source: BPIE survey / values or Luxembourg, Portugal, Cyprus and Belgium were estimated

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

IE

UK GRNONLMTSIDK ITSK FRFIHULUPT

CYBERODEATPLSEBGCZCHLTESEELV

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 32/132

32 | Europe’s buildings under the microscope

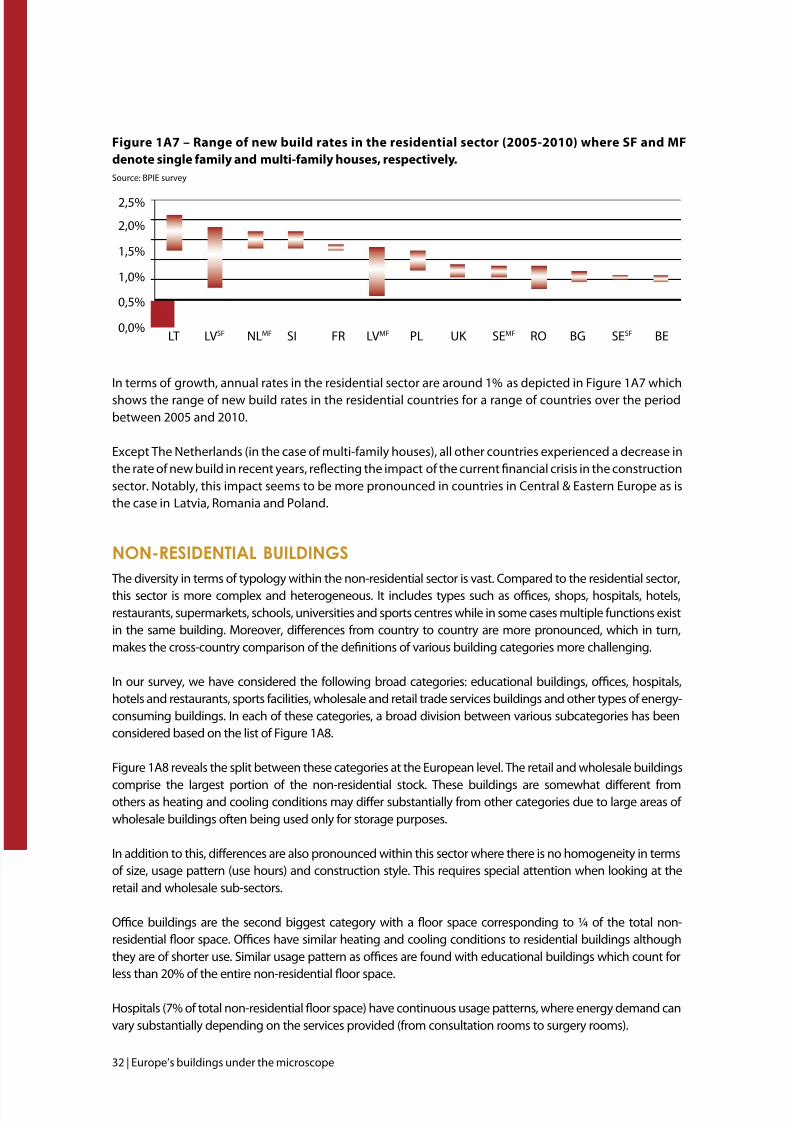

Fiure1A7–Raneofnewbuildratesintheresidentialsector(2005-2010)whereSFandMFdenote single amily and multi-amily houses, respectively.

Source: BPIE survey

In terms o growth, annual rates in the residential sector are around 1% as depicted in Figure 1A7 whichshows the range o new build rates in the residential countries or a range o countries over the periodbetween 2005 and 2010.

Except The Netherlands (in the case o multi-amily houses), all other countries experienced a decrease inthe rate o new build in recent years, reecting the impact o the current nancial crisis in the constructionsector. Notably, this impact seems to be more pronounced in countries in Central & Eastern Europe as isthe case in Latvia, Romania and Poland.

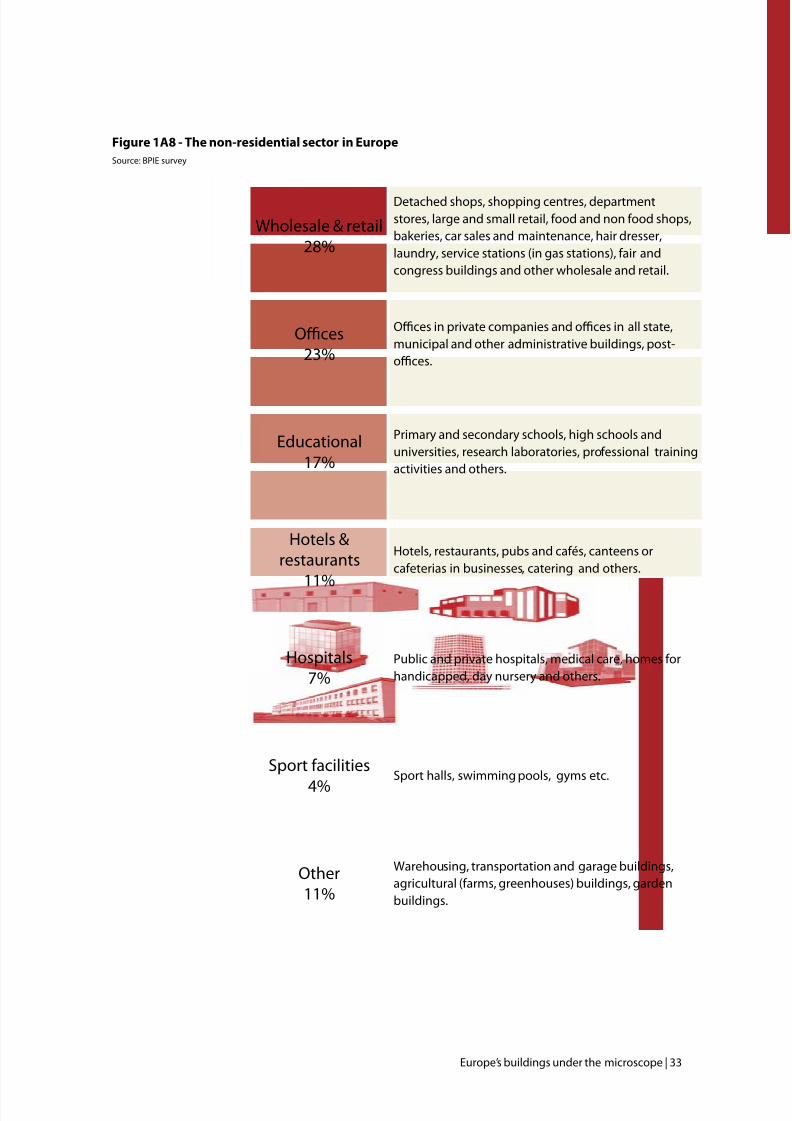

non-residentiAl buildings

The diversity in terms o typology within the non-residential sector is vast. Compared to the residential sector,this sector is more complex and heterogeneous. It includes types such as oces, shops, hospitals, hotels,restaurants, supermarkets, schools, universities and sports centres while in some cases multiple unctions existin the same building. Moreover, diferences rom country to country are more pronounced, which in turn,makes the cross-country comparison o the denitions o various building categories more challenging.

In our survey, we have considered the ollowing broad categories: educational buildings, oces, hospitals,hotels and restaurants, sports acilities, wholesale and retail trade services buildings and other types o energy-consuming buildings. In each o these categories, a broad division between various subcategories has beenconsidered based on the list o Figure 1A8.

Figure 1A8 reveals the split between these categories at the European level. The retail and wholesale buildings

comprise the largest portion o the non-residential stock. These buildings are somewhat diferent romothers as heating and cooling conditions may difer substantially rom other categories due to large areas o wholesale buildings oten being used only or storage purposes.

In addition to this, diferences are also pronounced within this sector where there is no homogeneity in termso size, usage pattern (use hours) and construction style. This requires special attention when looking at theretail and wholesale sub-sectors.

Oce buildings are the second biggest category with a oor space corresponding to ¼ o the total non-residential oor space. Oces have similar heating and cooling conditions to residential buildings althoughthey are o shorter use. Similar usage pattern as oces are ound with educational buildings which count orless than 20% o the entire non-residential oor space.

Hospitals (7% o total non-residential oor space) have continuous usage patterns, where energy demand canvary substantially depending on the services provided (rom consultation rooms to surgery rooms).

2,5%

2,0%

1,5%

1,0%

0,5%

0,0%LT LVSF NLMF SI FR LVMF PL UK SEMF RO BG SESF BE

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 33/132

Europe’s buildings under the microscope | 33

Figure 1A8 - The non-residential sector in Europe

Source: BPIE survey

Wholesale & retail28%

Detached shops, shopping centres, departmentstores, large and small retail, ood and non ood shops,bakeries, car sales and maintenance, hair dresser,laundry, service stations (in gas stations), air andcongress buildings and other wholesale and retail.

Oces23%

Oces in private companies and oces in all state,municipal and other administrative buildings, post-oces.

Educational17%

Primary and secondary schools, high schools anduniversities, research laboratories, proessional trainingactivities and others.

Hotels &restaurants

11%

Hotels, restaurants, pubs and caés, canteens orcaeterias in businesses, catering and others.

Hospitals7%

Public and private hospitals, medical care, homes orhandicapped, day nursery and others.

Sport acilities

4%Sport halls, swimming pools, gyms etc.

Other11%

Warehousing, transportation and garage buildings,agricultural (arms, greenhouses) buildings, gardenbuildings.

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 34/132

34 | Europe’s buildings under the microscope

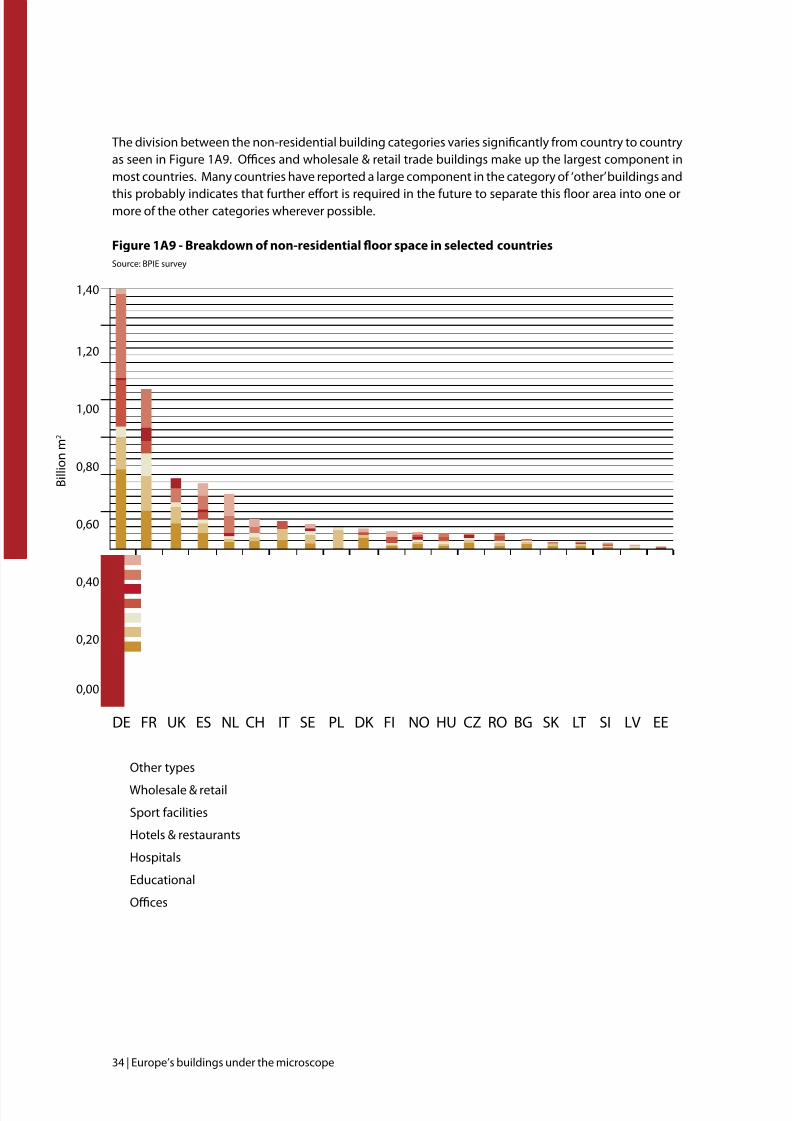

The division between the non-residential building categories varies signicantly rom country to countryas seen in Figure 1A9. Oces and wholesale & retail trade buildings make up the largest component inmost countries. Many countries have reported a large component in the category o ‘other’ buildings and

this probably indicates that urther efort is required in the uture to separate this oor area into one ormore o the other categories wherever possible.

Figure 1A9 - Breakdown o non-residential oor space in selected countries

Source: BPIE survey

Other types

Wholesale & retail

Sport acilities

Hotels & restaurants

Hospitals

Educational

Oces

DE FR UK ES NL CH IT SE PL DK FI NO HU CZ RO BG SK LT SI LV EE

1,40

1,20

1,00

0,80

0,60

0,40

0,20

0,00

B i l l i o n m 2

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 35/132

Europe’s buildings under the microscope | 35

While the dataset o residential buildings is airly comprehensive, the non-residential stock is ar lesscovered, as the sector is associated with higher uncertainty levels due to the diculties in tracking theexisting stock o all diferent non-residential types and developing an appropriate statistical database.

Public buildings are in the limelight at the moment due to the policies requiring the public sector to leadby example where all new constructions in the sector are required to be o nearly zero energy standardsby end o 20189 while a sectoral renovation rate o at least 3% is recommended10.

The exercise carried out by BPIE has reinorced the need or collecting better data and urge a call or theestablishment o guidelines and requirements under which Member States should gather more extensiveand consistent data on the typology o their non-residential stock.

b. chArActeristics

In addition to typology, buildings vary greatly in terms o age, size and location. The data collected through oursurvey has allowed us to draw up a picture o these characteristics. These are discussed in more detail below.

Age

Buildings across Europe are associated with diferent time periods dating even beore the 1900s. Historicalbuildings certainly have a signicant heritage value while construction techniques and building regulationssuch as building codes imposed at the design phase have a great inuence on the energy perormance o abuilding built in a specic period.

In the residential sector, the age o a building is likely to be strongly linked to the level o energy use or themajority o buildings that have not undergone renovation to improve energy perormance.

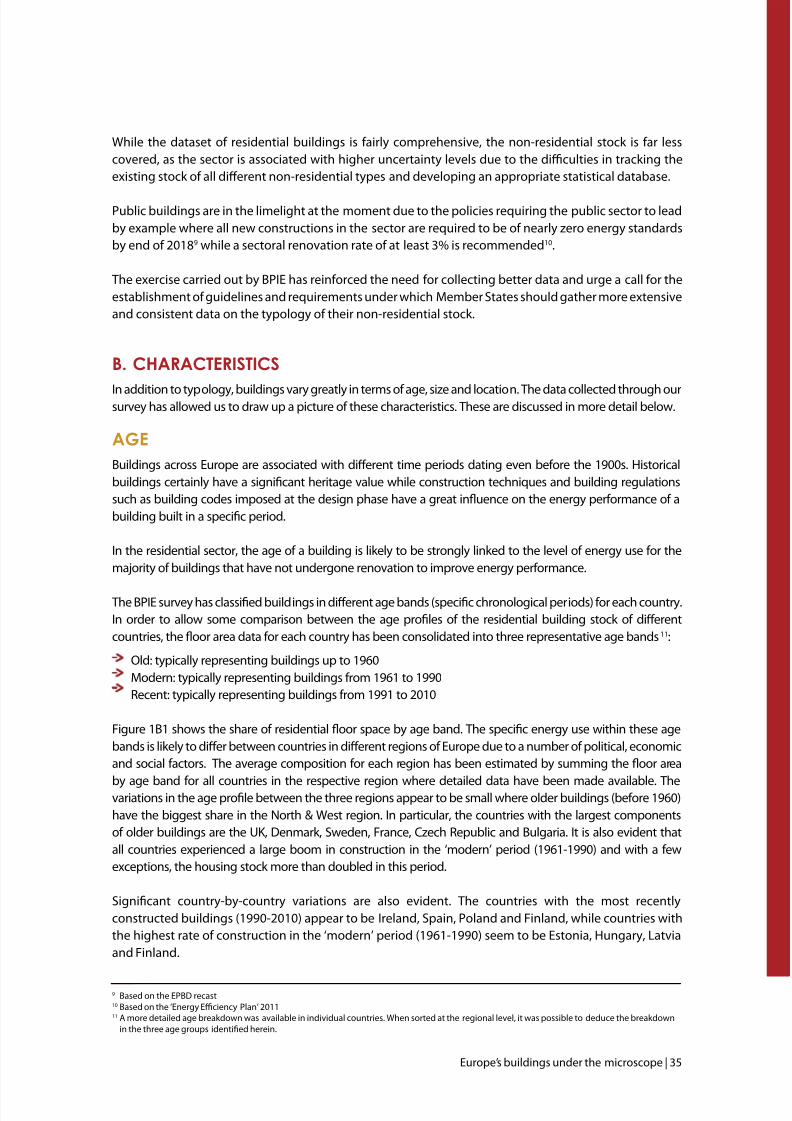

The BPIE survey has classied buildings in diferent age bands (specic chronological periods) or each country.In order to allow some comparison between the age proles o the residential building stock o diferentcountries, the oor area data or each country has been consolidated into three representative age bands 11:

Old: typically representing buildings up to 1960 Modern: typically representing buildings rom 1961 to 1990 Recent: typically representing buildings rom 1991 to 2010

Figure 1B1 shows the share o residential oor space by age band. The specic energy use within these agebands is likely to difer between countries in diferent regions o Europe due to a number o political, economicand social actors. The average composition or each region has been estimated by summing the oor area

by age band or all countries in the respective region where detailed data have been made available. Thevariations in the age prole between the three regions appear to be small where older buildings (beore 1960)have the biggest share in the North & West region. In particular, the countries with the largest componentso older buildings are the UK, Denmark, Sweden, France, Czech Republic and Bulgaria. It is also evident thatall countries experienced a large boom in construction in the ‘modern’ period (1961-1990) and with a ewexceptions, the housing stock more than doubled in this period.

Signicant country-by-country variations are also evident. The countries with the most recentlyconstructed buildings (1990-2010) appear to be Ireland, Spain, Poland and Finland, while countries withthe highest rate o construction in the ‘modern’ period (1961-1990) seem to be Estonia, Hungary, Latviaand Finland.

9 Based on the EPBD recast10 Based on the ‘Energy Eciency Plan’ 201111 A more detailed age breakdown was available in individual countries. When sorted at the regional level, it was possible to deduce the breakdown

in the three age groups identied herein.

7/29/2019 LR CbC Study

http://slidepdf.com/reader/full/lr-cbc-study 36/132

36 | Europe’s buildings under the microscope

Pre 1960

1961-1990

1991-2010

North & West

Central & East

42%

19%

39%

17%

35%

48%

Average per region

NOTES

BG: Based on estimationsEE: Data rom 1951 onwards.GR: Data only till 2000.IT: Values exclude heritage buildings beore the 1950.LT: Data rom 1941 onwards.

MT: Based on a sample survey with data until 2002.