South Q1 2014 IND Report

4

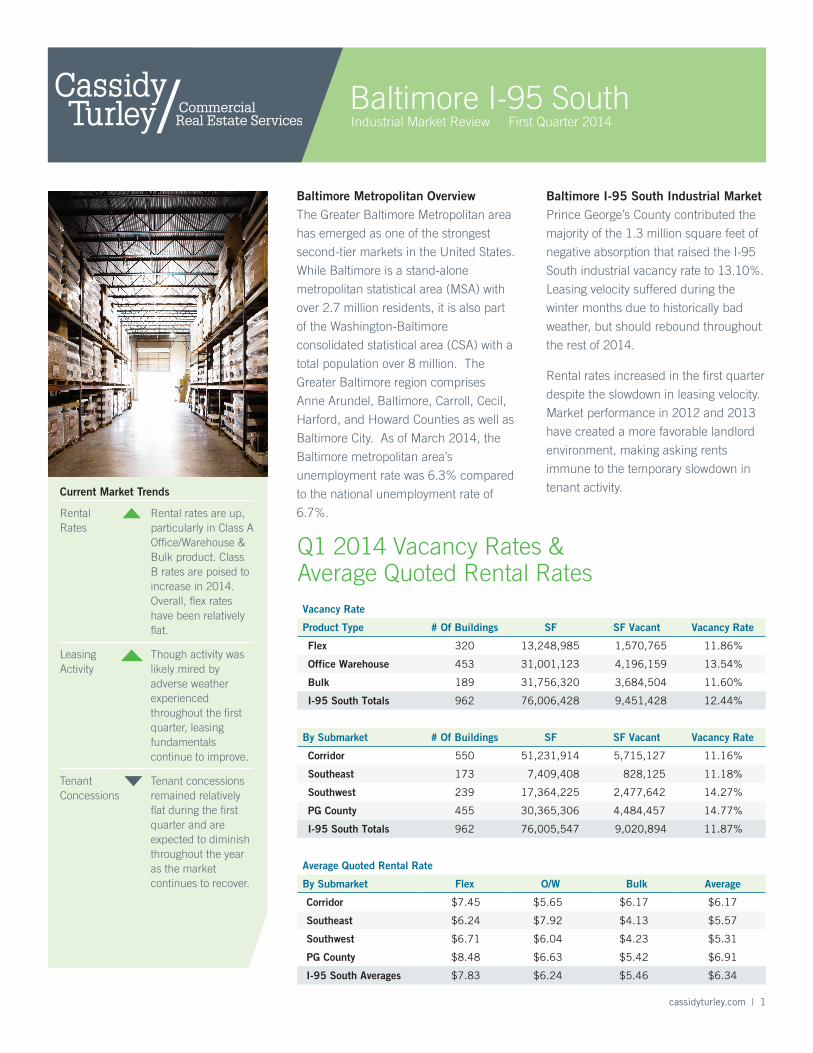

Current Market Trends Rental Rates Rental rates are up, particularly in Class A Office/Warehouse & Bulk product. Class B rates are poised to increase in 2014. Overall, flex rates have been relatively flat. Leasing Activity Though activity was likely mired by adverse weather experienced throughout the first quarter, leasing fundamentals continue to improve. Tenant Concessions Tenant concessions remained relatively flat during the first quarter and are expected to diminish throughout the year as the market continues to recover. cassidyturley.com | 1 Baltimore I-95 South Industrial Market Review First Quarter 2014 Baltimore Metropolitan Overview The Greater Baltimore Metropolitan area has emerged as one of the strongest second-tier markets in the United States. While Baltimore is a stand-alone metropolitan statistical area (MSA) with over 2.7 million residents, it is also part of the Washington-Baltimore consolidated statistical area (CSA) with a total population over 8 million. The Greater Baltimore region comprises Anne Arundel, Baltimore, Carroll, Cecil, Harford, and Howard Counties as well as Baltimore City. As of March 2014, the Baltimore metropolitan area’s unemployment rate was 6.3% compared to the national unemployment rate of 6.7%. Baltimore I-95 South Industrial Market Prince George’s County contributed the majority of the 1.3 million square feet of negative absorption that raised the I-95 South industrial vacancy rate to 13.10%. Leasing velocity suffered during the winter months due to historically bad weather, but should rebound throughout the rest of 2014. Rental rates increased in the first quarter despite the slowdown in leasing velocity. Market performance in 2012 and 2013 have created a more favorable landlord environment, making asking rents immune to the temporary slowdown in tenant activity. Q1 2014 Vacancy Rates & Average Quoted Rental Rates Vacancy Rate Product Type # Of Buildings SF SF Vacant Vacancy Rate Flex 320 13,248,985 1,570,765 11.86% Office Warehouse 453 31,001,123 4,196,159 13.54% Bulk 189 31,756,320 3,684,504 11.60% I-95 South Totals 962 76,006,428 9,451,428 12.44% By Submarket # Of Buildings SF SF Vacant Vacancy Rate Corridor 550 51,231,914 5,715,127 11.16% Southeast 173 7,409,408 828,125 11.18% Southwest 239 17,364,225 2,477,642 14.27% PG County 455 30,365,306 4,484,457 14.77% I-95 South Totals 962 76,005,547 9,020,894 11.87% Average Quoted Rental Rate By Submarket Flex O/W Bulk Average Corridor $7.45 $5.65 $6.17 $6.17 Southeast $6.24 $7.92 $4.13 $5.57 Southwest $6.71 $6.04 $4.23 $5.31 PG County $8.48 $6.63 $5.42 $6.91 I-95 South Averages $7.83 $6.24 $5.46 $6.34

Transcript of South Q1 2014 IND Report

Current Market Trends

Rental Rates

Rental rates are up, particularly in Class A Office/Warehouse & Bulk product. Class B rates are poised to increase in 2014. Overall, flex rates have been relatively flat.

Leasing Activity

Though activity was likely mired by adverse weather experienced throughout the first quarter, leasing fundamentals continue to improve.

Tenant Concessions

Tenant concessions remained relatively flat during the first quarter and are expected to diminish throughout the year as the market continues to recover.

cassidyturley.com | 1

Baltimore I-95 SouthIndustrial Market Review First Quarter 2014

Baltimore Metropolitan OverviewThe Greater Baltimore Metropolitan area

has emerged as one of the strongest

second-tier markets in the United States.

While Baltimore is a stand-alone

metropolitan statistical area (MSA) with

over 2.7 million residents, it is also part

of the Washington-Baltimore

consolidated statistical area (CSA) with a

total population over 8 million. The

Greater Baltimore region comprises

Anne Arundel, Baltimore, Carroll, Cecil,

Harford, and Howard Counties as well as

Baltimore City. As of March 2014, the

Baltimore metropolitan area’s

unemployment rate was 6.3% compared

to the national unemployment rate of

6.7%.

Baltimore I-95 South Industrial MarketPrince George’s County contributed the

majority of the 1.3 million square feet of

negative absorption that raised the I-95

South industrial vacancy rate to 13.10%.

Leasing velocity suffered during the

winter months due to historically bad

weather, but should rebound throughout

the rest of 2014.

Rental rates increased in the first quarter

despite the slowdown in leasing velocity.

Market performance in 2012 and 2013

have created a more favorable landlord

environment, making asking rents

immune to the temporary slowdown in

tenant activity.

Q1 2014 Vacancy Rates & Average Quoted Rental RatesVacancy Rate

Product Type # Of Buildings SF SF Vacant Vacancy Rate

Flex 320 13,248,985 1,570,765 11.86%

Office Warehouse 453 31,001,123 4,196,159 13.54%

Bulk 189 31,756,320 3,684,504 11.60%

I-95 South Totals 962 76,006,428 9,451,428 12.44%

By Submarket # Of Buildings SF SF Vacant Vacancy Rate

Corridor 550 51,231,914 5,715,127 11.16%

Southeast 173 7,409,408 828,125 11.18%

Southwest 239 17,364,225 2,477,642 14.27%

PG County 455 30,365,306 4,484,457 14.77%

I-95 South Totals 962 76,005,547 9,020,894 11.87%

Average Quoted Rental Rate

By Submarket Flex O/W Bulk Average

Corridor $7.45 $5.65 $6.17 $6.17

Southeast $6.24 $7.92 $4.13 $5.57

Southwest $6.71 $6.04 $4.23 $5.31

PG County $8.48 $6.63 $5.42 $6.91

I-95 South Averages $7.83 $6.24 $5.46 $6.34

BALTIMORE I-95 SOUTH • INDUSTRIAL • FIRST QUARTER 2014

About Cassidy TurleyCassidy Turley is a leading commercial real estate services provider with more than 4,000 professionals in more than 60 offices nationwide. With headquarters in Washington, DC, the company represents a wide range of clients—from small businesses to Fortune 500 companies, from local non-profits to major institutions. The firm completed transactions valued at $25.8 billion in 2013, manages approximately 400 million square feet on behalf of institutional, corporate and private clients and supports more than 24,000 domestic corporate services locations. Cassidy Turley serves owners, investors and tenants with a full spectrum of integrated commercial real estate services—including capital markets, tenant representation, corporate services, project leasing, property management, project and development services, and research and consulting. Cassidy Turley enhances its global service delivery outside North America through a partnership with GVA, giving clients access to commercial real estate professionals in 65 international markets. Please visit www.cassidyturley.com for more information about Cassidy Turley. cassidyturley.com | 2

Notable Q1 2014 Lease Transactions

Property 7460 New Ridge Road Hanover, MD

3051 Washington Boulevard Baltimore, MD

Size 30,000 SF 60,000 SF

Term 10 Years 3 Years

Yr. 1 Rent/Esc. $8.50 / 2.5% $4.85 / 3.0%

TI PSF $11.00 from “cold, dark shell” Minimal

Tenant Kawneer Nexius

Landlord Liberty Property Trust FRP Development

Type New New

15.10% Vacancy Rate of 20’-23’ clear buildings in the BW Corridor submarket at the end of Q1 2014.

9.20% Vacancy Rate of 24’-28’ clear buildings in the BW Corridor submarket at the end of Q1 2014.

For more information, contact one of our Industrial Brokers:

Cassidy Turley 100 Light Street Suite 1400 Baltimore, MD 21202 Tel: 410.752.4285 Fax: 410.576.9031

www.cassidyturley.com

Notable Q1 2014 Sales Transactions

Property 1811 Cabin Branch Drive Landover, MD

1701 Brightseat Road Landover, MD

Size 360,550 SF 216,000 SF

Seller Oakmont Industrial Group Finmarc

Buyer TIAA Salus Property Investments

Price +/-$34,250,000 $31,650,000

Behind the Numbers

Submarket Cassidy Turley Classification Number of Buildings Total Size (SF) Total Available (SF) Vacancy Rate QTR Absorption (SF)

Corridor

Airport 100 3 737,600 0 0.00% 0

Arundel Crossing 11 1,706,054 67,070 3.93% 0

Baltimore Commons 33 3,748,920 580,704 15.49% 2,400

Baymeadow 17 2,073,594 87,285 4.21% -24,000

Brandon Woods 17 1,973,886 46,956 2.38% 3,935

BWI Commerce Park 14 511,658 39,300 7.68% -5,700

BWIP 96 7,709,179 823,480 10.68% -176,533

Columbia Gateway 4 2,168,713 356,891 16.46% 0

Corridor Industrial 18 2,050,248 90,174 4.40% 0

Cromwell Business Park 14 707,632 67,679 9.56% 6,020

Guilford Industrial 34 2,681,778 436,290 16.27% 70,445

Harwood Industrial Park 9 159,645 4,900 3.07% -3,400

Hillside/Preston Gateway 8 1,566,168 26,208 1.67% 0

Industrial Trade Center 14 669,887 112,790 16.84% -37,400

Junction Business Park 18 1,205,248 155,826 12.93% 0

Marley Neck 8 1,755,835 230,398 13.12% 0

MD Wholesale Food Center 17 2,979,319 853,842 28.66% 0

Meadowridge 13 1,707,670 73,295 4.29% 20,654

Montevideo/Dorsey Run 18 1,830,248 316,645 17.30% -15,495

Oakland Ridge 17 961,632 25,409 2.64% 0

Park 100 5 484,450 224,000 46.24% 0

Parkway Industrial 24 1,397,839 130,995 9.37% -21,348

Patapsco Valley 7 1,195,772 180,229 15.07% 0

Race Road 4 277,855 40,716 14.65% -14,064

Route 1 Corridor 33 1,633,889 69,165 4.23% 3,600

Route 1 Laurel 21 1,346,020 99,640 7.40% 14,067

Route 100 30 2,726,585 404,413 14.83% 22,666

Sieling Industrial 27 1,265,308 154,783 12.23% 19,014

Troy Hill 16 1,999,180 184,805 9.24% -33,622

Total 550 51,231,812 5,883,888 11.48% -168,761

Southeast

Annapolis Industrial 23 778,629 71,622 9.20% -6,894

Brooklyn 19 1,717,159 380,291 22.15% -68,400

I-97 Industrial 56 1,756,607 87,480 4.98% 12,030

Route 2 Industrial 34 1,078,403 107,594 9.98% -31,914

Route 3 Industrial 21 594,486 23,429 3.94% 21,963

Route 170 17 1,360,024 458,651 33.72% -227,727

Telegraph Rd Business Pk 3 125,083 15,000 11.99% -15,000

Total 173 7,410,391 1,144,067 15.44% -315,942

Southwest

Arbutus Industrial 69 6,385,507 1,016,277 15.92% -61,952

Baltimore City Southwest 35 2,117,863 360,770 17.03% 2,500

Camden Industrial Park 24 2,908,697 451,629 15.53% 26,295

Caton Research Center 41 1,709,154 228,515 13.37% 8,042

DeSoto 25 1,448,506 111,850 7.72% -47,250

Hammonds Ferry 43 2,560,612 168,432 6.58% 111,534

West Port, Camden 2 233,886 86,000 36.77% 15,000

Total 239 17,364,225 2,423,473 13.96% 54,169

Cassidy Turley Industrial Market Statistical OverviewJanuary 1, 2014 - March 31, 2014

BALTIMORE I-95 SOUTH • INDUSTRIAL • FIRST QUARTER 2014

cassidyturley.com | 3

Cassidy Turley Industrial Market Statistical OverviewJanuary 1, 2014 - March 31, 2014

BALTIMORE I-95 SOUTH • INDUSTRIAL • FIRST QUARTER 2014

Submarket Cassidy Turley Classification Number of Buildings Total Size (SF) Total Available (SF) Vacancy Rate QTR Absorption (SF)

PG County

Beltsville 86 4,300,031 642,600 14.94% 29,923

Bowie 57 4,386,656 604,943 13.79% -147,508

Branch Ave Corridor 31 1,528,440 463,115 30.30% -245,663

Brandywine/PG South 7 1,095,228 166,500 15.20% -150,300

Capitol Heights 37 2,267,872 349,914 15.43% -100,882

Cheverly/Hyattsville 26 989,789 101,194 10.22% 15,852

Greenbelt 4 348,842 138,065 39.58% -52,875

Landover/Largo 81 8,668,183 1,014,877 11.71% -132,044

Lanham 37 2,447,813 342,384 13.99% -124,434

Laurel 32 1,556,111 239,182 15.37% 31,394

NatHbr/OxnHill/FtWash 7 127,690 15,400 12.06% -1,180

Penn Ave Corridor 36 1,830,010 350,100 19.13% 14,310

Takoma Pk/College Pk 10 715,618 48,833 6.82% 497

Upper Marlboro 4 103,023 7,350 7.13% -1,150

Total 455 30,365,306 4,484,457 14.77% -864,060

Grand Total 1,417 106,371,734 13,935,885 13.10% -1,294,594

cassidyturley.com | 4

![PREZENTACJA WYNIKOWA za 1 kwartał 2016 roku · 2016-08-18 · Q1 2014 Q1 2016 ROE [%] 122,1 131,5 133,0 13,4 15,7 17,7 0 5 10 15 0 50 100 150 Q1 2014 Q1 2015 Q1 2016 mln z ... WYNIKI](https://static.fdocuments.pl/doc/165x107/5f57034afb6cbe52ea12d716/prezentacja-wynikowa-za-1-kwarta-2016-roku-2016-08-18-q1-2014-q1-2016-roe-.jpg)