raport roczny ok - pekaobh.pl fileraportroczny 2005 list do udziaŁowcÓw sprawozdanie zarzĄdu...

142

� � � � � � � � � � � � � ��� � � � � �� � � � � 5 0 0 2

Transcript of raport roczny ok - pekaobh.pl fileraportroczny 2005 list do udziaŁowcÓw sprawozdanie zarzĄdu...

�������������

�������������

5 002

RAPORT ROCZNY 2005

LIST DO UDZIAŁOWCÓW

SPRAWOZDANIE ZARZĄDUOPINIA I RAPORT BIEGŁEGO REWIDENTA

�

�

��

SPRAWOZDANIE FINANSOWE��

ANNUAL REPORT 2004

LETTER TO SHAREHOLDERS

MANAGEMENT BOARD REPORTOPINION AND REPORT OF THE AUDITOR

�

��

��

FINANCIAL STATEMENT���

LIST DO UDZIAŁOWCÓWLETTER TO SHAREHOLDERS

2

Szanowni Państwo,

Akcjonariusze i Klienci BPH Banku Hipotecznego S.A.,

Rok 2005 był kolejnym udanym rokiem działalności BPH Banku Hipotecznego S.A., w któ-rym Bank umocnił pozycję konkurencyjną w segmencie specjalistycznych banków hipotecz-nych ze znaczącą poprawą wyników finansowych.

W 2005 roku przeprowadziliśmy, pierwszą w historii Banku, publiczną emisję hipotecznych listów zastawnych na łączną kwotę 600 mln zł. Tym samym Bank wysunął się na pozycję lidera emisji listów zastawnych w obrocie publicznym.

Osiągnęliśmy rekordowy wynik finansowy brutto, który wyniósł 35 163 tys. zł oraz wskaź-nik wypłacalności na poziomie 14,1%, co potwierdza dobrą i stabilną kondyncję naszego Banku. O wysokiej efektywności działania świadczy wskaźnik kosztów do dochodów, który w 2005 roku wyniósł 36%.

Wyrażam przekonanie, że w roku 2006 równie pomyślnie zrealizujemy postawione sobie cele i zamierzenia.

LIST DO UDZIAŁOWCÓW BPH BANKU HIPOTECZNEGO S.A.

3

W imieniu Zarządu Banku przekazuję wszystkim naszym pracownikom i współpracowni-kom podziękowania za zaangażowanie oraz zrozumienie zadań i wyzwań stojących przed Bankiem.

Dziękując Akcjonariuszom i Klientom za okazane zaufanie i wspieranie naszych działań zapraszam do lektury Sprawozdania Rocznego za rok 2005, zawierającego szczegółowe informacje o naszej działalności.

Z wyrazami szacunku,

Irena Stocka

Prezes Zarządu

BPH Banku Hipotecznego S.A.

4

Dear Sirs,

Shareholders and Clients of BPH Bank Hipoteczny S.A.,

Year 2005 was another year of successful activity of BPH Bank Hipoteczny S.A. This year the Bank strengthened its competitive position in the segment of specialised mortgage banks and significantly improved its financial results.

In 2005, for the first time in the Bank’s history, we realised a public issue of mortgage bonds for the total value of 600 million PLN. It gave the Bank a position of a leader in pu-blic issue of mortgage bonds.

We achieved a record gross financial result, reaching 35,163 thousands PLN, and the solvency ratio at the level of 14.1%, which confirms good and balanced condition of our Bank. High efficiency of our operations is reflected by the costs-to-profits ratio, which in 2005 amounted to 36%.

I am convinced that in 2006, we will equally successfully realise our goals and plans.

LETTER TO BPH BANK HIPOTECZNY S.A. SHAREHOLDERS

5

On behalf of the Management Board of the Bank, I would like to thank all our employees and partners for their commitment and understanding of tasks and challenges that the Bank faces.

Expressing my gratitude to Shareholders and Clients for their trust and support for our activity, I am glad to invite you to read the Annual Statement of Accounts for 2005, conta-ining detailed information on our operations.

Yours faithfully,

Irena Stocka

President of the Management Board

BPH Bank Hipoteczny S.A.

SPRAWOZDANIE ZARZĄDU

MANAGEMENT BOARD REPORT

7

1

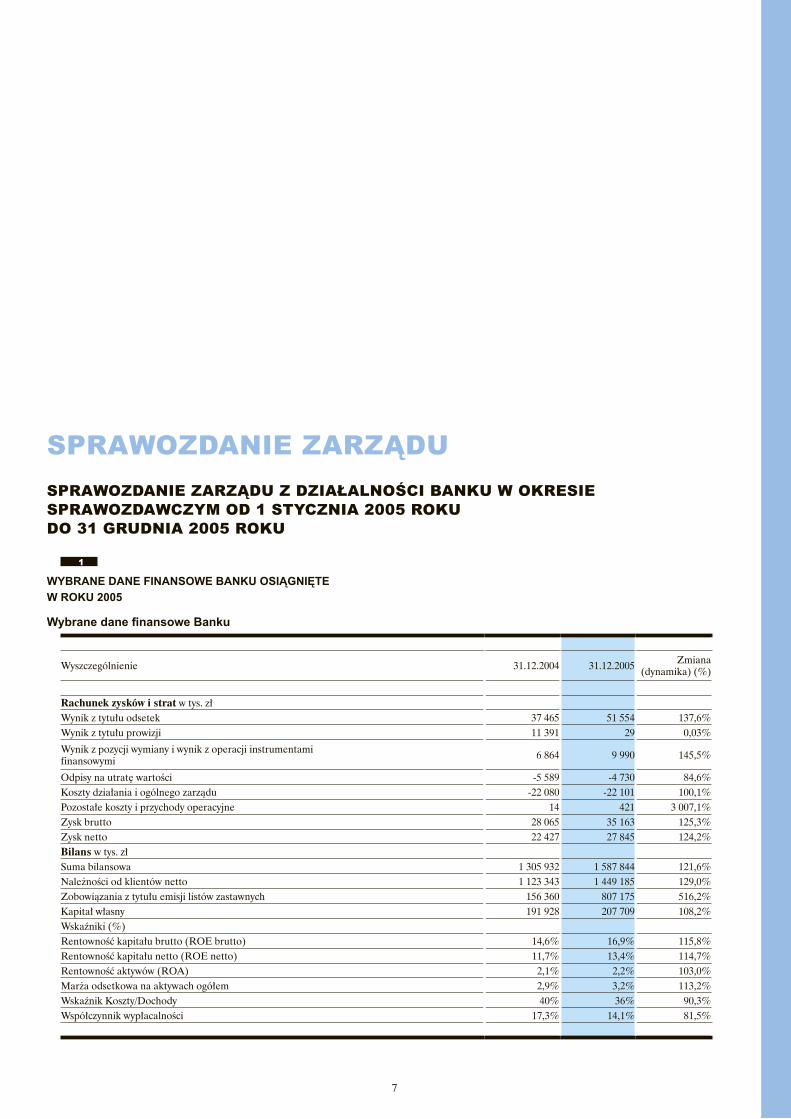

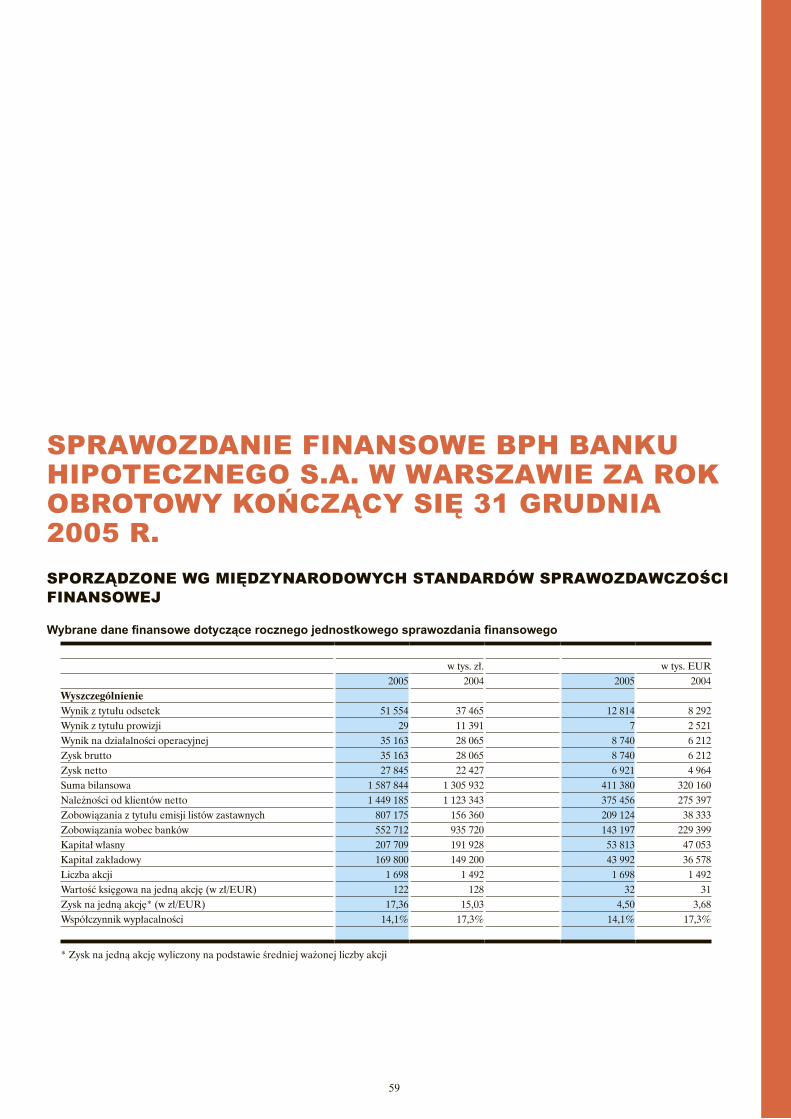

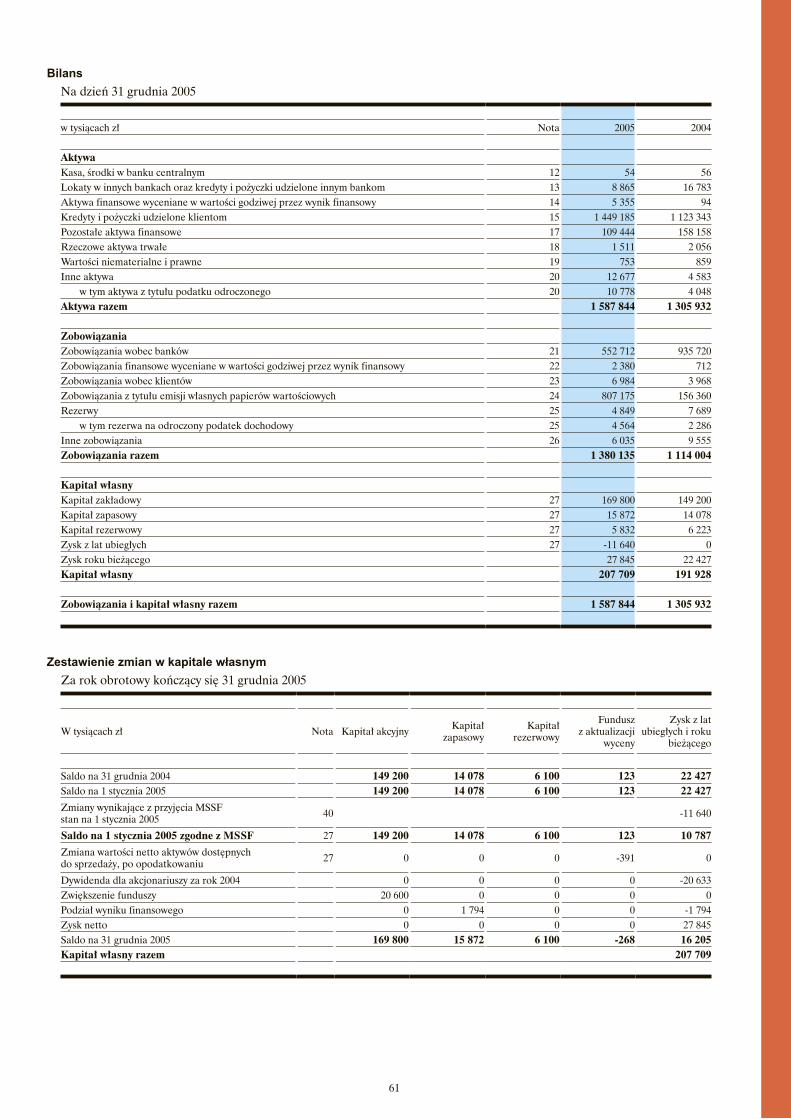

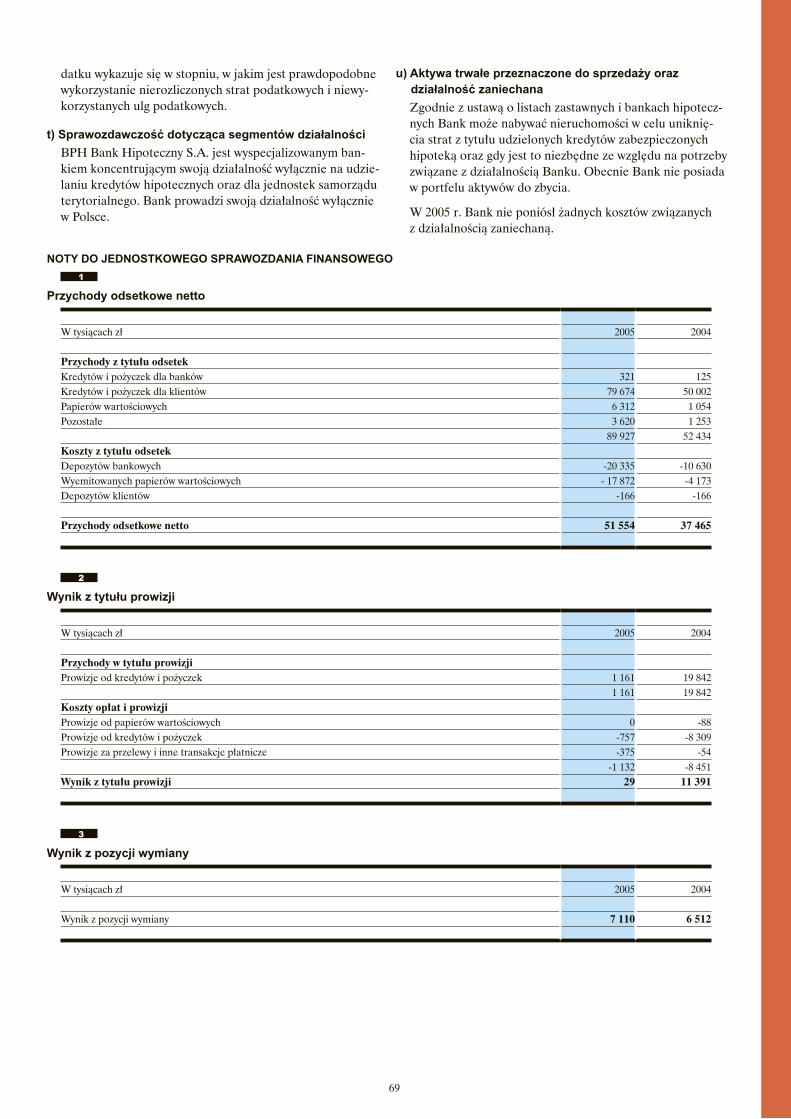

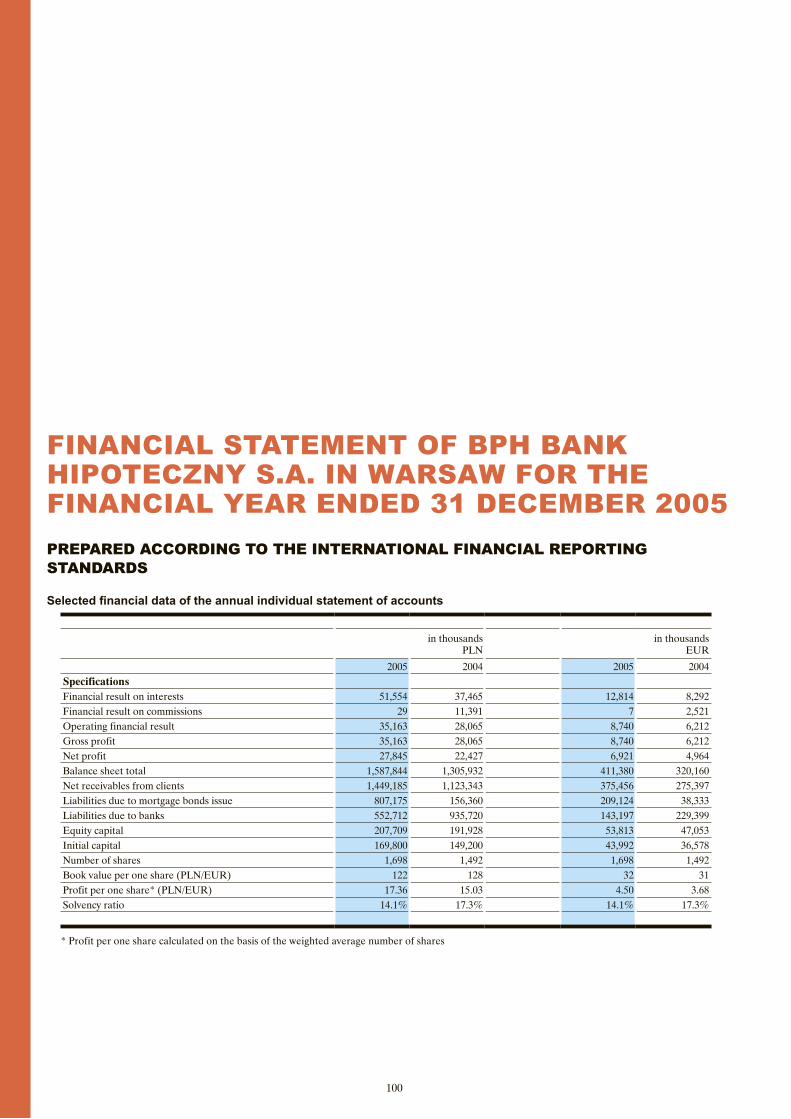

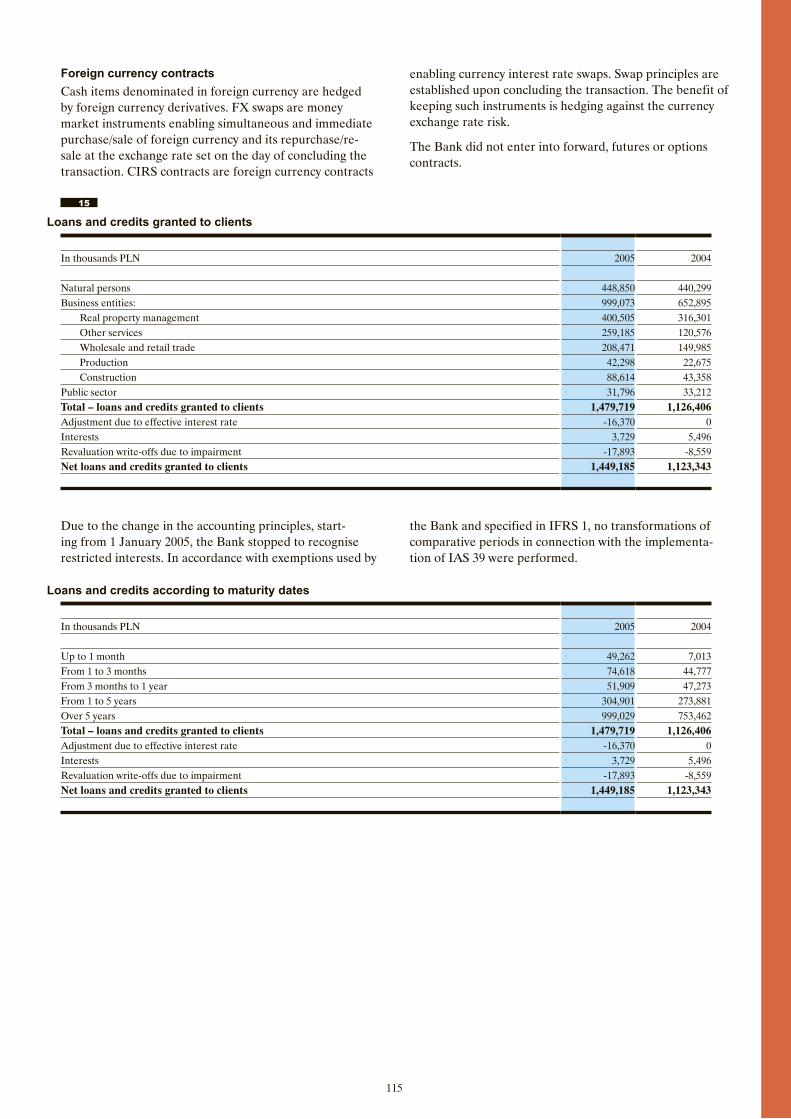

WYBRANE DANE FINANSOWE BANKU OSIĄGNIĘTE W ROKU 2005

SPRAWOZDANIE ZARZĄDU SPRAWOZDANIE ZARZĄDU Z DZIAŁALNOŚCI BANKU W OKRESIE SPRAWOZDAWCZYM OD 1 STYCZNIA 2005 ROKU DO 31 GRUDNIA 2005 ROKU

Wybrane dane finansowe Banku

Wyszczególnienie 31.12.2004 31.12.2005 Zmiana (dynamika) (%)

Rachunek zysków i strat w tys. zł Wynik z tytułu odsetek 37 465 51 554 137,6%Wynik z tytułu prowizji 11 391 29 0,03%

Wynik z pozycji wymiany i wynik z operacji instrumentami finansowymi 6 864 9 990 145,5%

Odpisy na utratę wartości -5 589 -4 730 84,6%Koszty działania i ogólnego zarządu -22 080 -22 101 100,1%Pozostałe koszty i przychody operacyjne 14 421 3 007,1%Zysk brutto 28 065 35 163 125,3%Zysk netto 22 427 27 845 124,2%Bilans w tys. zł Suma bilansowa 1 305 932 1 587 844 121,6%Należności od klientów netto 1 123 343 1 449 185 129,0%Zobowiązania z tytułu emisji listów zastawnych 156 360 807 175 516,2%Kapitał własny 191 928 207 709 108,2%Wskaźniki (%) Rentowność kapitału brutto (ROE brutto) 14,6% 16,9% 115,8%Rentowność kapitału netto (ROE netto) 11,7% 13,4% 114,7%Rentowność aktywów (ROA) 2,1% 2,2% 103,0%Marża odsetkowa na aktywach ogółem 2,9% 3,2% 113,2%Wskaźnik Koszty/Dochody 40% 36% 90,3%Współczynnik wypłacalności 17,3% 14,1% 81,5%

8

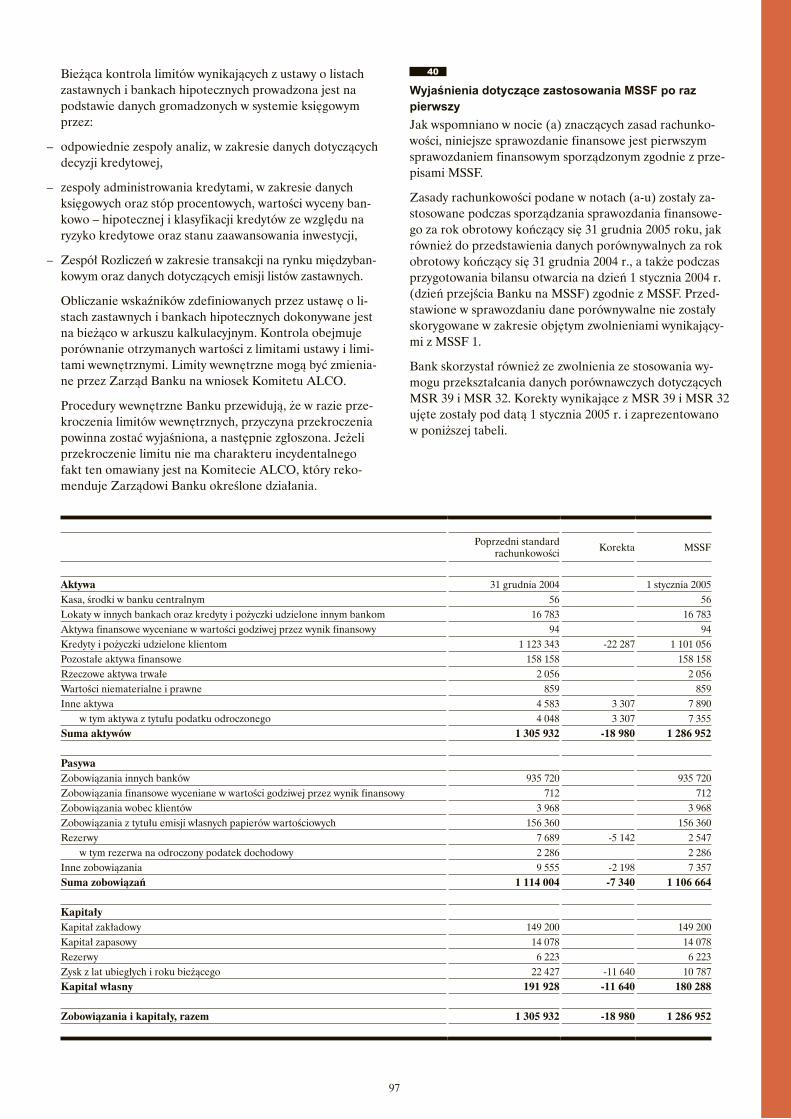

Ze względu na skorzystanie z dopuszczalnych wyłączeń MSSF 1 dane za rok 2005 nie są w pełni porównywalne z danymi za rok 2004. Najważniejsze zmiany wynikające z zastosowania Międzynarodowych Standardów Spra-wozdawczości Finansowej związane są z wprowadzeniem wyceny według efektywnej stopy procentowej oraz zmia-nami zasad tworzenia odpisów z tytułu utraty wartości. Wśród pozycji, których wartości w bilansie otwarcia uległy znacznej zmianie wymienić należy: kredyty i pożyczki udzielone klientom, aktywa z tytułu podatku odroczone-go, rezerwy oraz wynik z lat ubiegłych. Wysokość korekty bilansu otwarcia ujmowana w kapitałach wynosi 11 640 tys. zł (zmniejszenie). Szczegółowe wyjaśnienie, jaki wpływ na poszczególne pozycje sprawozdania finansowego miało przyjęcie MSSF znajduje się w nocie 40 tego sprawozdania.

BPH Bank Hipoteczny S.A. jest drugim, pod względem wielkości aktywów i pod względem wolumenu kredytów, dynamicznie rozwijającym się bankiem specjalistycznym w Polsce. Osiągnięte przez Bank wyniki za 2005 r. zostały opisane w rozdziale Wyniki finansowe za 2005 r.

Głównym akcjonariuszem Banku jest Bank BPH S.A., je-den z największych banków w Polsce, notowany na Giełdzie Papierów Wartościowych w Warszawie (GPW).

Bank należy do Grupy Kapitałowej Banku BPH S.A. i jego sprawozdania finansowe na potrzeby nadzoru są konsolido-wane ze sprawozdaniami fiansowymi Banku BPH S.A.

Sprawozdania Grupy Kapitałowej Banku BPH S.A. podle-gają konsolidacji bezpośrednio ze sprawozdaniami finanso-wymi Banku Austria Creditansatalt AG (BA-CA) z siedzibą w Wiedniu, jako większościowego akcjonariusza Banku BPH S.A. Podmiotem dominującym wobec BA-CA jest Bayerische Hypo-und Vereinsbank AG (HVB), którego jednostką nadrzędną jest UniCredito Italiano S.p.A. (UCI) – podmiot będący większościowym akcjonariuszem HVB.

Działalność Banku w okresie sprawozdawczym, jego dynamika oraz obszary aktywności wynikały z roli i pozycji Banku w Grupie Banku BPH.

2

SYTUACJA MAKROEKONOMICZNA W ROKU 2005, W TYM SEKTOR BANKOWY

Według wstępnych szacunków GUS tempo wzrostu go-spodarczego w 2005 roku wyniosło 3,2%. Na bazie danych rocznych szacuje się, że dynamika realna PKB w czwartym kwartale 2005 roku ukształtowała się na poziomie ok. 4,0% r/r. Tempo wzrostu inwestycji w gospodarce w 2005 roku wyniosło 6,2%, co wskazuje na ich nie notowany od czwartego kwartału 1999 roku dwucyfrowy wzrost w czwar-tym kwartale (ok. 10,0% r/r).

Brak zagrożeń inflacyjnych ze strony popytu wewnętrzne-go, w połączeniu z malejącym wskaźnikiem cen towarów i usług (spadek z 3,7% r/r w styczniu do 0,7% r/r w grudniu) skłoniło RPP do pięciokrotnej obniżki stóp procentowych w 2005 roku łącznie o 200 pb. Stopa referencyjna NBP wynosiła na koniec grudnia 2005 roku 4,50% wobec 6,50% w styczniu. Największe cięcia stóp procentowych miały miejsce w pierwszej połowie roku (łącznie o 150 pb), kiedy

to GUS opublikował dalekie od oczekiwań dane na temat wzrostu gospodarczego w pierwszym kwartale 2005 roku. Wraz z poprawą wskaźników makroekonomicznych RPP stała się bardziej powściągliwa i ostatnich obniżek doko-nała w lipcu i sierpniu łącznie o 50 pb. Redukcjom stóp procentowych towarzyszyły zmiany nastawienia w polityce pieniężnej: z restrykcyjnego w styczniu na łagodne w lutym, następnie w kwietniu zmieniono nastawienie łagodne na neutralne, po czym w czerwcu powrócono do nastawienia łagodnego i utrzymano je do końca roku.

Dynamika inwestycji w 2005 roku na poziomie 6,2% była wyższa od oczekiwań w końcu 2005 roku i jednocześnie dużo niższa od prognoz chociażby jeszcze w pierwszym kwartale 2005 roku. Najwolniejsze tempo wzrostu nakła-dów brutto na środki trwałe zanotowano w pierwszym kwartale (1,2% r/r), po czym w kolejnych kwartałach ulega-ło ono umiarkowanemu przyspieszeniu: do 3,8% r/r w dru-gim kwartale, 5,7% r/r w trzecim kwartale i ok. 10,0% r/r w ostatnim kwartale. Na niską aktywność inwestycyjną przedsiębiorstw (których udział w inwestycjach krajowych ogółem wynosi ok. 53%) w pierwszej połowie roku wpływ miały z jednej strony duże problemy z pozyskaniem środ-ków z funduszy strukturalnych UE, z drugiej zaś niepew-ność odnośnie kształtowania się warunków inwestycyjnych po wyborach prezydenckich i parlamentarnych.

W sektorze bankowym w 2005 roku zaobserwowano dalsze zwiększenie dynamiki kredytów zarówno przedsiębiorstw, jak i gospodarstw domowych. Podobnie jak w 2004 r. szybko rosły wolumeny kredytów hipotecznych – na koniec roku dynamika przekroczyła 40%. Przyczyniły się do tego: łagodniejsza polityka kredytowa banków, obniżanie kosz-tów kredytu oraz poprawa sytuacji finansowej gospodarstw domowych. Najważniejszą przyczyną zmian w polityce kre-dytowej jest wzrost międzybankowej presji konkurencyjnej.

Nasilająca się konkurencja w sektorze bankowym powo-duje, że w walce o klienta banki decydują się na obniżenie marż kredytów, opłat i prowizji związanych z udzieleniem kredytu. Znacznemu uproszczeniu ulegają również pro-cedury przyznawania kredytów, a okresy kredytowania wydłużają się.

3

DZIAŁALNOŚĆ BPH BANKU HIPOTECZNEGO S.A.

BPH Bank Hipoteczny Spółka Akcyjna działa na podstawie Ustawy z dnia 29 sierpnia 1997 roku o listach zastawnych i bankach hipotecznych oraz Uchwały Komisji Nadzoru Bankowego z dnia 1 grudnia 1999 roku Nr 244/KNB/99.

Przywołana podstawa działaności Banku określa, że BPH Bank Hipoteczny S.A. może prowadzić swą działalność w dwóch obszarach: udzielania kredytów hipotecznych i dla jednostek samorzadu terytorialnego oraz emisji hipotecz-nych listów zastawnych.

Działalność kredytowaW roku 2005 Bank koncentrował się na budowie bez-piecznego portfela kredytowego udzielając kredytów na finansowanie nieruchomości komercyjnych i mieszkalnych. Swoją ofertę kredytową Bank kierował zarówno do przed-

9

siębiorców, jak i osób prywatnych. Celami kredytowania były: zakup, budowa, modernizacja, remont nieruchomości komercyjnej lub mieszkalnej przeznaczonych do użytku wła-snego lub na działalność komercyjną. Kredyt mógł być także przeznaczony na refinansowanie kredytu zaciągniętego w in-nym banku lub refinansowania kapitału własnego zainwe-stowanego w nieruchomość. Kredyty udzielane są w złotych i w opcji indeksowanej do walut obcych (USD, EUR, CHF). Sprzedaż prowadzona była przez grupę własnych doradców bankowych i sieć ponad 180 zewnętrznych partnerów sprze-daży, a także przez placówki Banku BPH S.A.

W 2005 r. Bank udzielił 568 kredytów, na łączną kwotę 563 mln PLN. Portfel kredytów hipotecznych wzrósł o 27% w stosunku do 2004 roku i osiągnął wartość 1,48 mld PLN na koniec 2005 roku.

Bank przede wszystkim koncentrował się na finansowaniu nieruchomości komercyjnych. Oferta Banku, dostosowana do oczekiwań klientów komercyjnych, pozwoliła na pozy-skanie 190 nowych klientów, co stanowiło wzrost o 36% w porównaniu z rokiem ubiegłym i zrealizowanie 447 mln zł wolumenu w tym segmencie.

Kluczowe czynniki sukcesu:

– Wysoka atrakcyjność oferty dla przedsiębiorców oraz ela-styczność w dostosowywaniu kredytów do indywidualnych potrzeb i możliwości tych Klientów.

– Rozwijanie współpracy z Partnerami sprzedaży i podnosze-nie ich kwalifikacji w zakresie współpracy z Klientami.

– Wsparcie sprzedaży kredytów mieszkaniowych akcją mar-ketingową dotyczącą refinansowania kredytów mieszkanio-wych.

Kontynuacja trendu wzrostowego przychodów z tego obszaru działalności Banku wspierana była w roku 2005 pozytywnym wpływem rynkowych stóp procentowych na marżę kredytową.

W roku 2005 udział kredytów z rozpoznaną utratą wartości, na które Bank utworzył rezerwy celowe utrzymał się na bezpiecznym poziomie 2,9%, a stosunek rezerw celowych utworzonych na te należności do całości portfela kredyto-wego wyniósł 1,2%.

Ogólna kwota bankowo-hipotecznej wartości nieruchomo-ści, przyjętych przez Bank jako zabezpieczenie kredytów hipotecznych, wg stanu na 31.12.2005 r., wynosi 3 102 763 tys. zł.

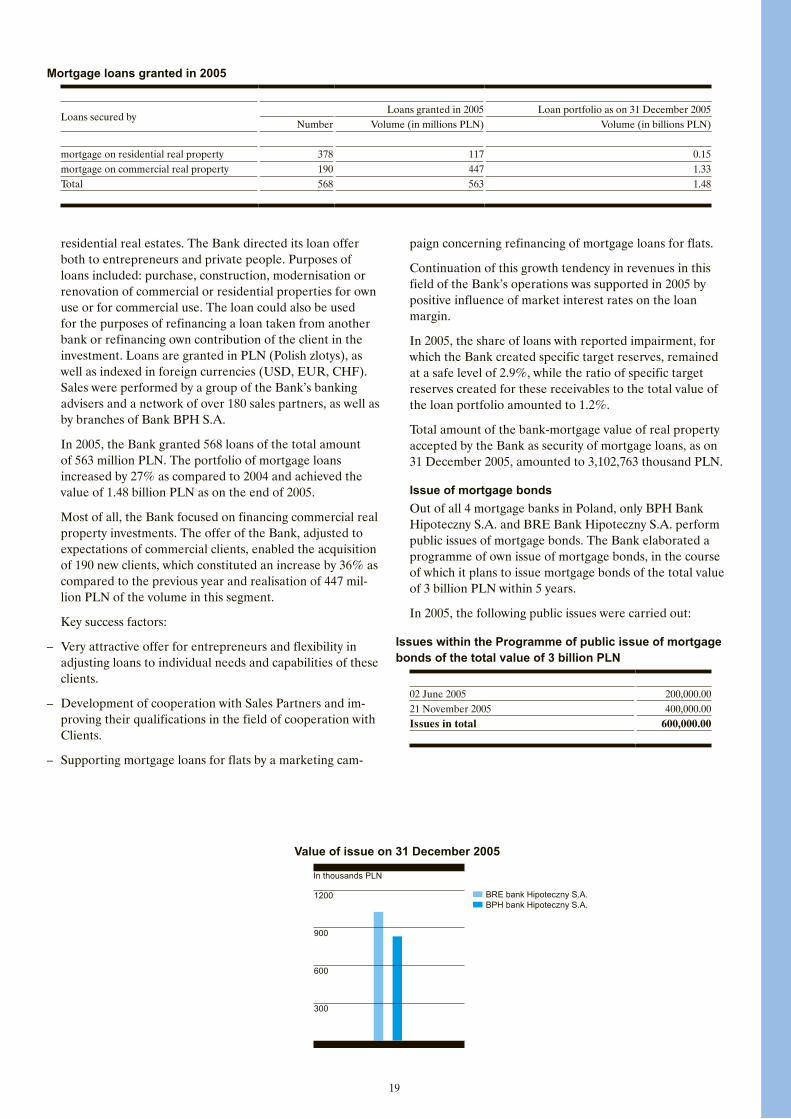

Emisja hipotecznych listów zastawnychW Polsce spośród 4 banków hipotecznych tylko BPH Bank Hipoteczny S.A. oraz BRE Bank Hipoteczny S.A. pro-wadzą publiczną emisję hipotecznych listów zastawnych. Bank przygotował Program publicznej emisji hipotecznych listów zastawnych, w ramach którego planuje przeprowa-dzić w ciągu 5 lat emisję hipotecznych listów zastawnych o wartości 3 mld zł.

W 2005 r. przeprowadzono następujące emisje publiczne:

Emisje w ramach Programu publicznej emisji hipotecz-nych listów zastawnych na kwotę 3 mld PLN

02 czerwca 2005 roku 200 000,0021 listopada 2005 roku 400 000,00Łącznie emisje 600 000,00

Wartość emisji na 31 grudnia 2005 roku

BRE bank Hipoteczny S.A.BPH bank Hipoteczny S.A.

1200

900

600

300

w tys. zł

Kredyty hipoteczne udzielone w 2005 r.

Kredyty zabezpieczoneKredyty udzielone w 2005 r Portfel kredytów wg stanu na 31.12.2005 r.

Liczba Wolumen (mln zł) Wolumen (mld zł)

hipoteką na nieruchomości mieszkalnej 378 117 0,15hipoteką na nieruchomości komercyjnej 190 447 1,33Łącznie 568 563 1,48

10

W roku 2005 Bank przeprowadził niepubliczną emisję hipotecznych listów zastawnych w wysokości 150 mln PLN. Wartość wyemitowanych listów zastawnych w formie emisji niepublicznej na koniec roku wynosi 190 000 tys. zł oraz 3 630 tys. EUR. Emisja listów zastawnych w złotych przeprowadzona jest zgodnie z Umową o przeprowadzenie programu emisji papierów dłużnych z 2003 r., natomiast emisja w walucie obcej oparta jest o przepisy Umowy Emi-syjnej z 2000 r.

Podstawę do przeprowadzenia emisji publicznej lub niepublicznej stanowią wierzytelności wpisane do rejestru zabezpieczenia hipotecznych listów zastawnych. Wartość wierzytelności stanowiących zabezpieczenie emisji, wg sta-nu na koniec 2005 roku, wynosi 1 030 179 tys. zł.

Pozyskane z emisji hipotecznych listów zastawnych środki umożliwiają refinansowanie działalności Banku w obszarze działalności kredytowej, bez konieczności podnoszenia kapitału zakładowego.

4

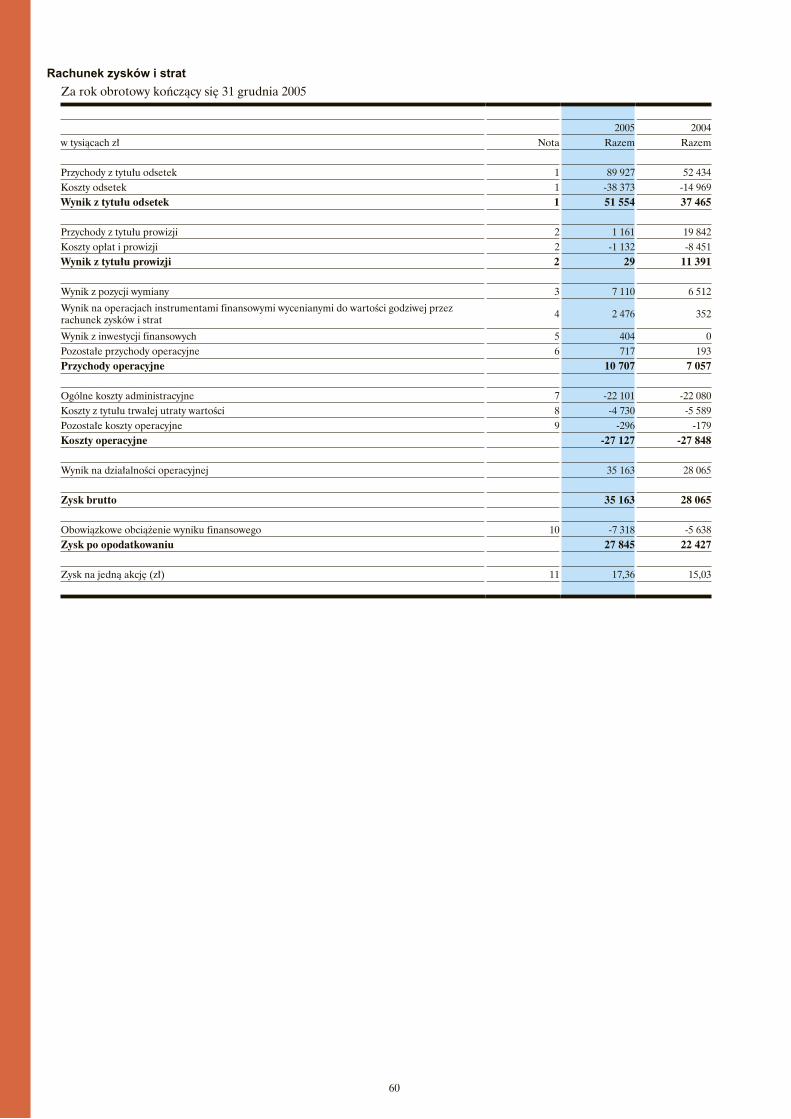

WYNIKI FINANSOWE ZA ROK 2005

W roku 2005 Bank osiągnął bardzo dobre wyniki finanso-we, dzięki którym umocnił swoją pozycję konkurencyjną w segmencie specjalistycznych banków hipotecznych.

Wzrost sumy bilansowej Banku w stosunku do poprzednie-go roku wyniósł 281 912 tys. zł. Zysk netto osiągnął poziom 27 845 tys. zł, co oznacza wzrost o 5 418 tys. zł.

Największy wpływ na uzyskany wynik finansowy miał wynik z tytułu odsetek. Wzrost wyniku odsetkowego nastąpił wskutek zwiększenia wolumenu kredytowego oraz wzrostu marży z tytułu efektywnego rozliczania prowizji. Innym istotnym czynnikiem, który przyczynił się do osiągnięcia dobrego wyniku finansowego było utrzymanie restrykcyjnej polityki kosztowej.

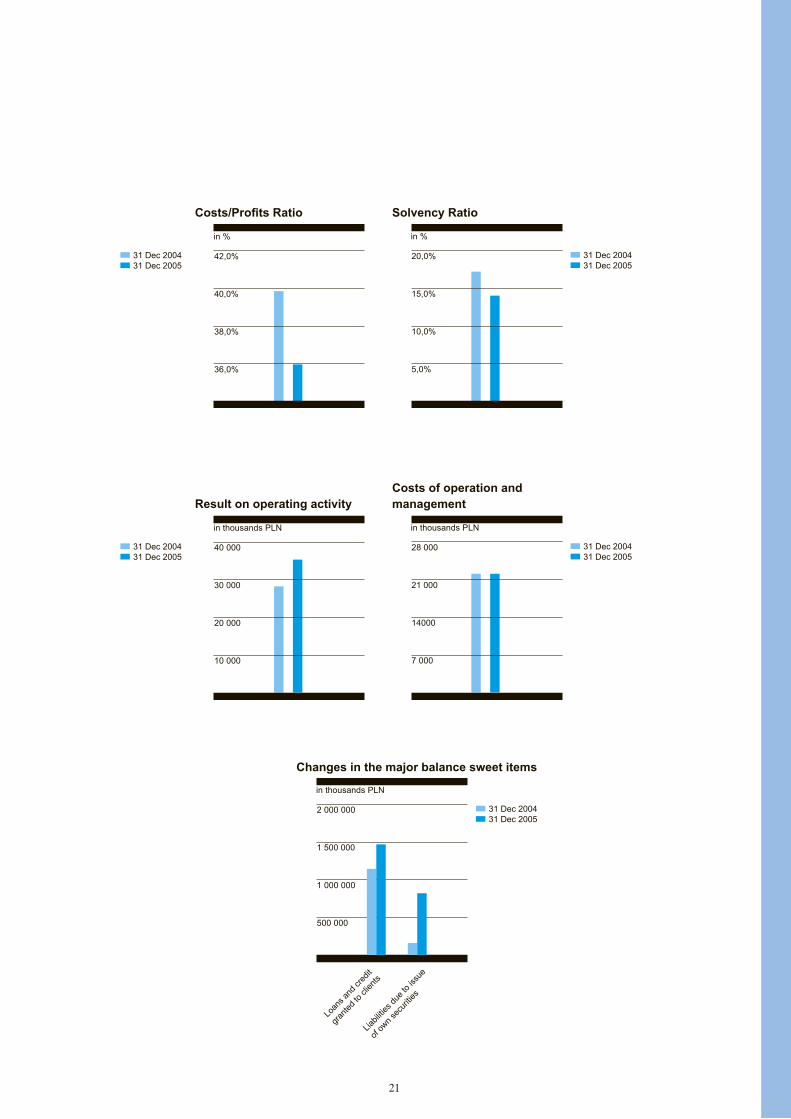

Najważniejsze wskaźniki ekonomiczne oraz wielkości wy-branych pozycji rachunku wyników zostały zaprezentowane na poniższych diagramach.

31 grudnia 2004 r.31 grudnia 2005 r.

2,22%

2,19%

2,16%

2,13%

w %

Wskaźnik ROA

31 grudnia 2004 r.31 grudnia 2005 r.

3,4%

3,2%

3,0%

2,8%

w %

Marża odsetkowa na aktywach ogółem

31 grudnia 2004 r.31 grudnia 2005 r.

18,0%

16,5%

15,0%

13,5%

w %

Wskaźnik ROE brutto

31 grudnia 2004 r.31 grudnia 2005 r.

14,0%

13,0%

12,0%

11,0%

w %

Wskaźnik ROE netto

11

31 grudnia 2004 r.31 grudnia 2005 r.

28 000

21 000

14000

7 000

w tys. zl

31 grudnia 2004 r.31 grudnia 2005 r.

40 000

30 000

20 000

10 000

w tys. zl

Wynik na działalności operacyjnej Koszty działalności

31 grudnia 2004 r.31 grudnia 2005 r.

2 000 000

1 500 000

1 000 000

500 000

w tys. zl

Kredyty

i poż

yczk

i

udzie

lone k

liento

m

Zabow

iązan

ia z t

ytułu

emisj

i włas

nych

papie

rów

wartśc

iowyc

h

Zmiany w głównych pozycjach bilansowych

31 grudnia 2004 r.31 grudnia 2005 r.

20,0%

15,0%

10,0%

5,0%

w %

31 grudnia 2004 r.31 grudnia 2005 r.

42,0%

40,0%

38,0%

36,0%

w %

Wskaźnik koszty/dochody Współczynik wypłacalności

12

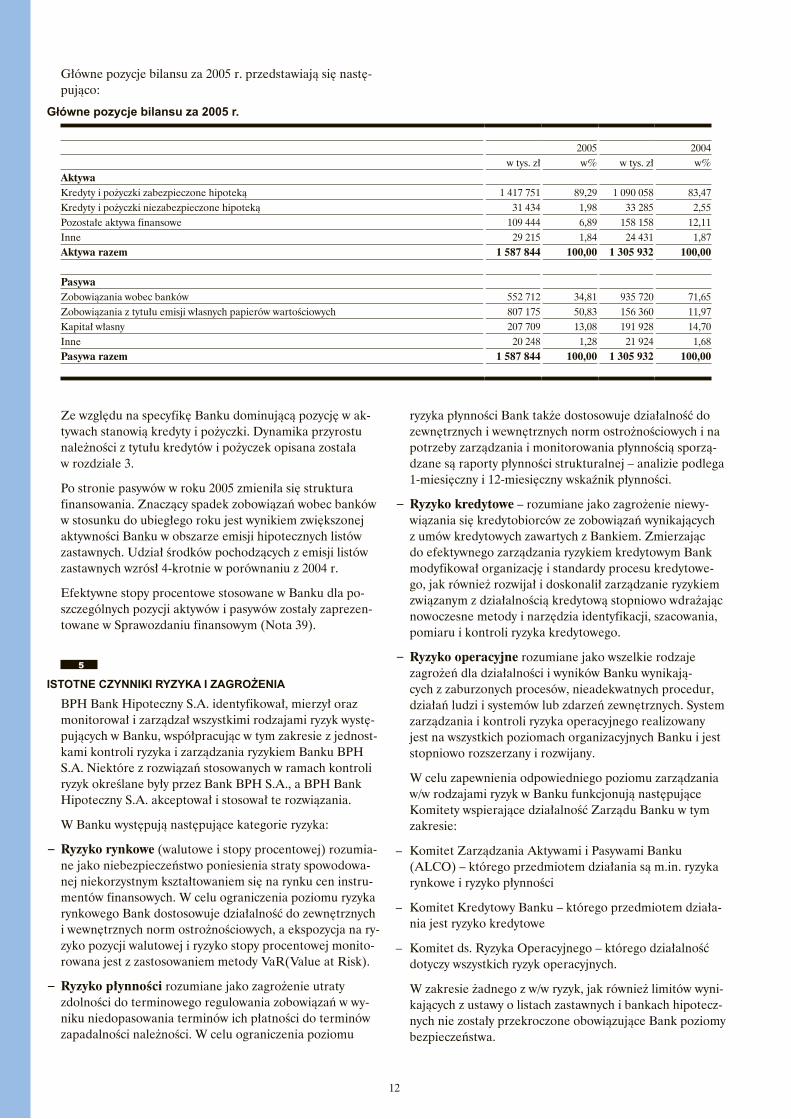

Główne pozycje bilansu za 2005 r. przedstawiają się nastę-pująco:

ryzyka płynności Bank także dostosowuje działalność do zewnętrznych i wewnętrznych norm ostrożnościowych i na potrzeby zarządzania i monitorowania płynnością sporzą-dzane są raporty płynności strukturalnej – analizie podlega 1-miesięczny i 12-miesięczny wskaźnik płynności.

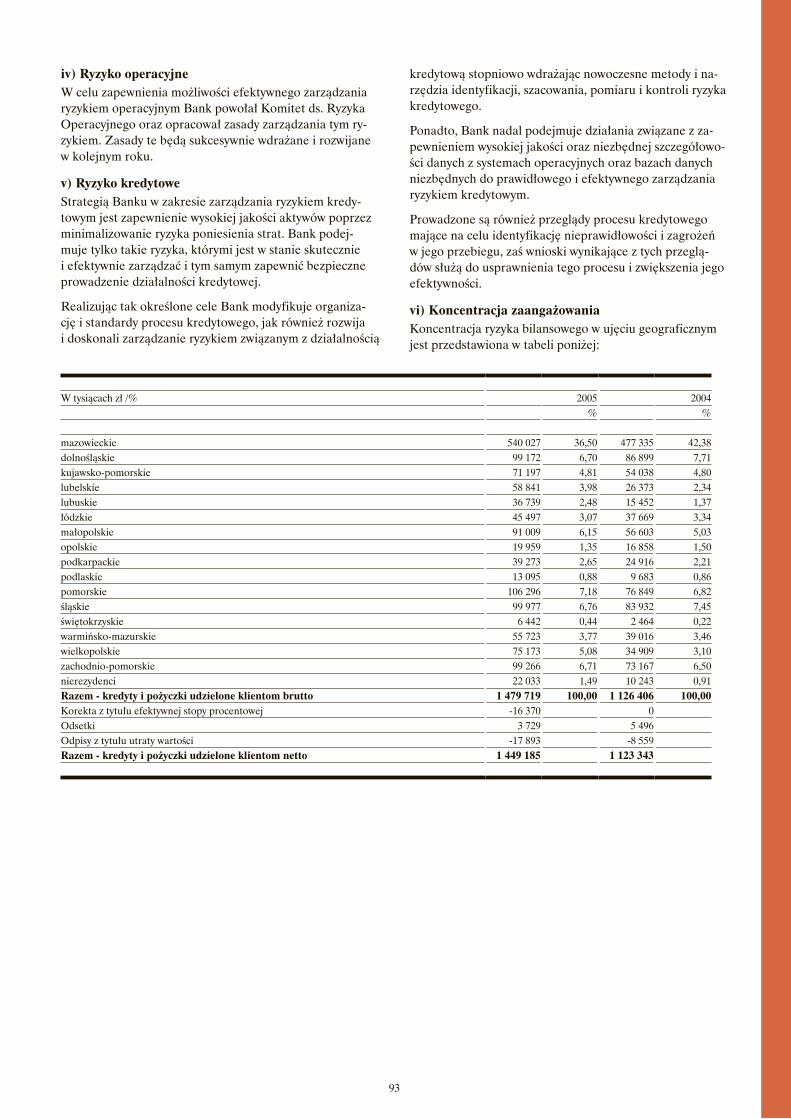

− Ryzyko kredytowe – rozumiane jako zagrożenie niewy-wiązania się kredytobiorców ze zobowiązań wynikających z umów kredytowych zawartych z Bankiem. Zmierzając do efektywnego zarządzania ryzykiem kredytowym Bank modyfikował organizację i standardy procesu kredytowe-go, jak również rozwijał i doskonalił zarządzanie ryzykiem związanym z działalnością kredytową stopniowo wdrażając nowoczesne metody i narzędzia identyfikacji, szacowania, pomiaru i kontroli ryzyka kredytowego.

− Ryzyko operacyjne rozumiane jako wszelkie rodzaje zagrożeń dla działalności i wyników Banku wynikają-cych z zaburzonych procesów, nieadekwatnych procedur, działań ludzi i systemów lub zdarzeń zewnętrznych. System zarządzania i kontroli ryzyka operacyjnego realizowany jest na wszystkich poziomach organizacyjnych Banku i jest stopniowo rozszerzany i rozwijany.

W celu zapewnienia odpowiedniego poziomu zarządzania w/w rodzajami ryzyk w Banku funkcjonują następujące Komitety wspierające działalność Zarządu Banku w tym zakresie:

– Komitet Zarządzania Aktywami i Pasywami Banku (ALCO) – którego przedmiotem działania są m.in. ryzyka rynkowe i ryzyko płynności

– Komitet Kredytowy Banku – którego przedmiotem działa-nia jest ryzyko kredytowe

– Komitet ds. Ryzyka Operacyjnego – którego działalność dotyczy wszystkich ryzyk operacyjnych.

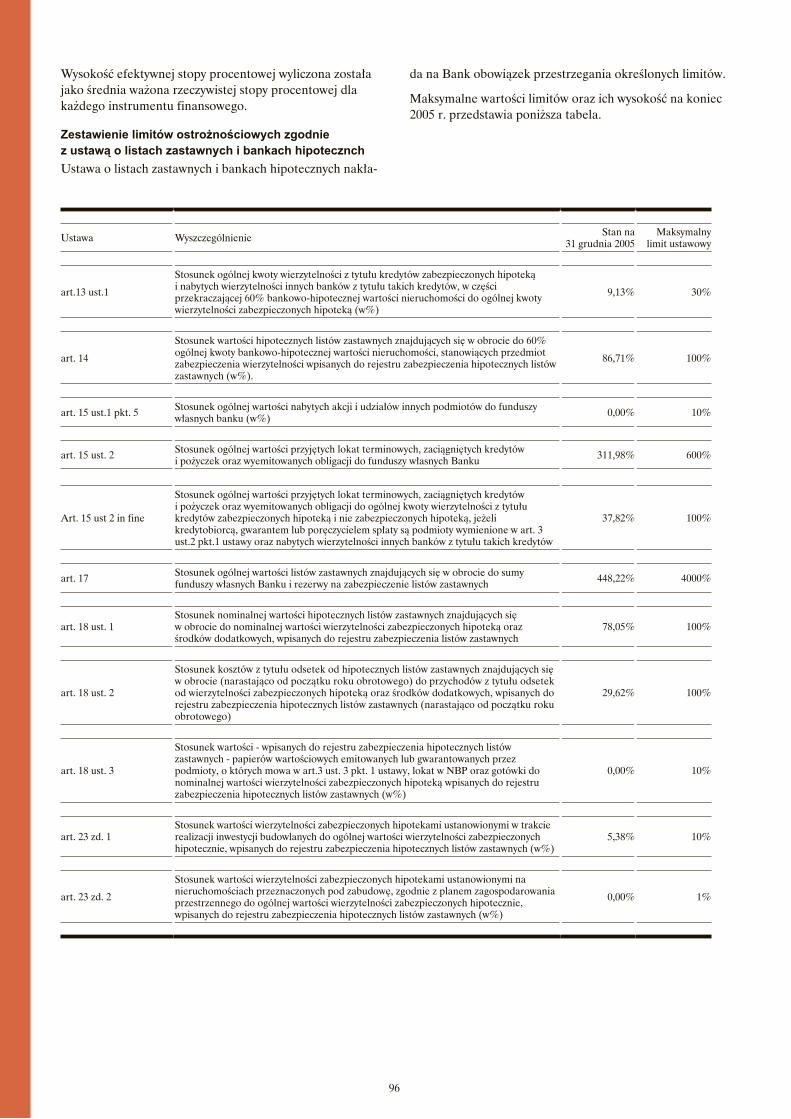

W zakresie żadnego z w/w ryzyk, jak również limitów wyni-kających z ustawy o listach zastawnych i bankach hipotecz-nych nie zostały przekroczone obowiązujące Bank poziomy bezpieczeństwa.

Ze względu na specyfikę Banku dominującą pozycję w ak-tywach stanowią kredyty i pożyczki. Dynamika przyrostu należności z tytułu kredytów i pożyczek opisana została w rozdziale 3.

Po stronie pasywów w roku 2005 zmieniła się struktura finansowania. Znaczący spadek zobowiązań wobec banków w stosunku do ubiegłego roku jest wynikiem zwiększonej aktywności Banku w obszarze emisji hipotecznych listów zastawnych. Udział środków pochodzących z emisji listów zastawnych wzrósł 4-krotnie w porównaniu z 2004 r.

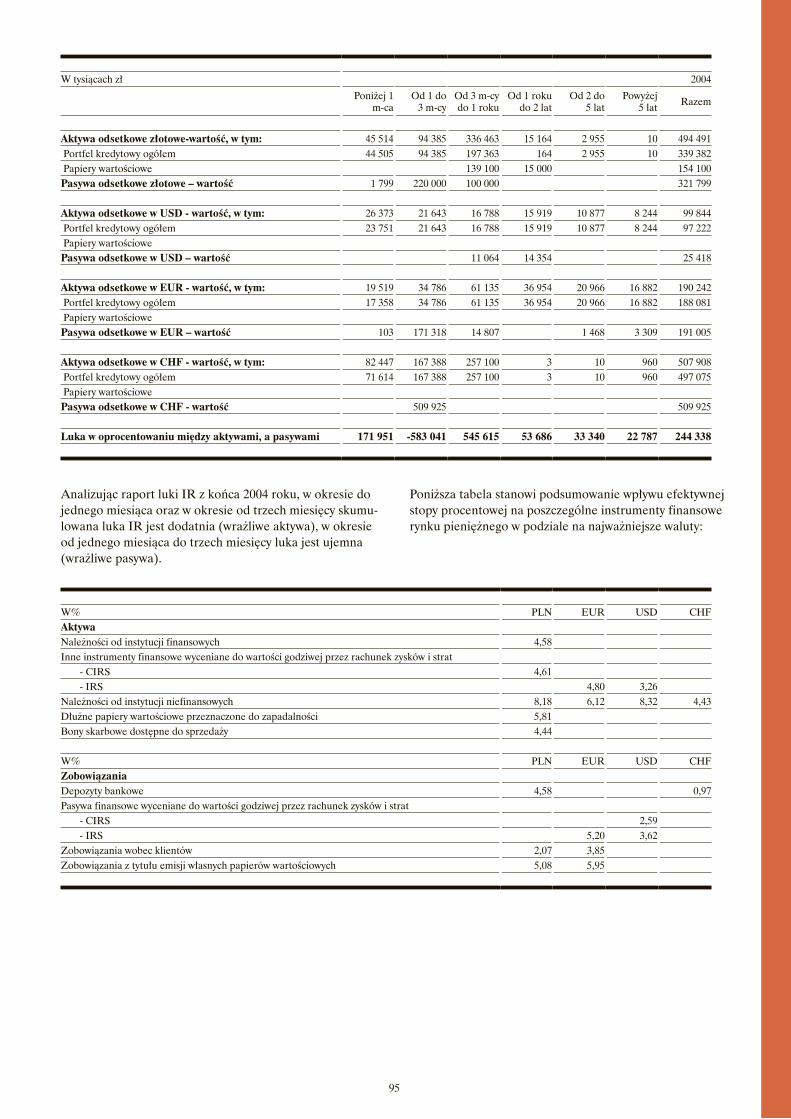

Efektywne stopy procentowe stosowane w Banku dla po-szczególnych pozycji aktywów i pasywów zostały zaprezen-towane w Sprawozdaniu finansowym (Nota 39).

5

ISTOTNE CZYNNIKI RYZYKA I ZAGROŻENIA

BPH Bank Hipoteczny S.A. identyfikował, mierzył oraz monitorował i zarządzał wszystkimi rodzajami ryzyk wystę-pujących w Banku, współpracując w tym zakresie z jednost-kami kontroli ryzyka i zarządzania ryzykiem Banku BPH S.A. Niektóre z rozwiązań stosowanych w ramach kontroli ryzyk określane były przez Bank BPH S.A., a BPH Bank Hipoteczny S.A. akceptował i stosował te rozwiązania.

W Banku występują następujące kategorie ryzyka:

− Ryzyko rynkowe (walutowe i stopy procentowej) rozumia-ne jako niebezpieczeństwo poniesienia straty spowodowa-nej niekorzystnym kształtowaniem się na rynku cen instru-mentów finansowych. W celu ograniczenia poziomu ryzyka rynkowego Bank dostosowuje działalność do zewnętrznych i wewnętrznych norm ostrożnościowych, a ekspozycja na ry-zyko pozycji walutowej i ryzyko stopy procentowej monito-rowana jest z zastosowaniem metody VaR(Value at Risk).

− Ryzyko płynności rozumiane jako zagrożenie utraty zdolności do terminowego regulowania zobowiązań w wy-niku niedopasowania terminów ich płatności do terminów zapadalności należności. W celu ograniczenia poziomu

Główne pozycje bilansu za 2005 r.

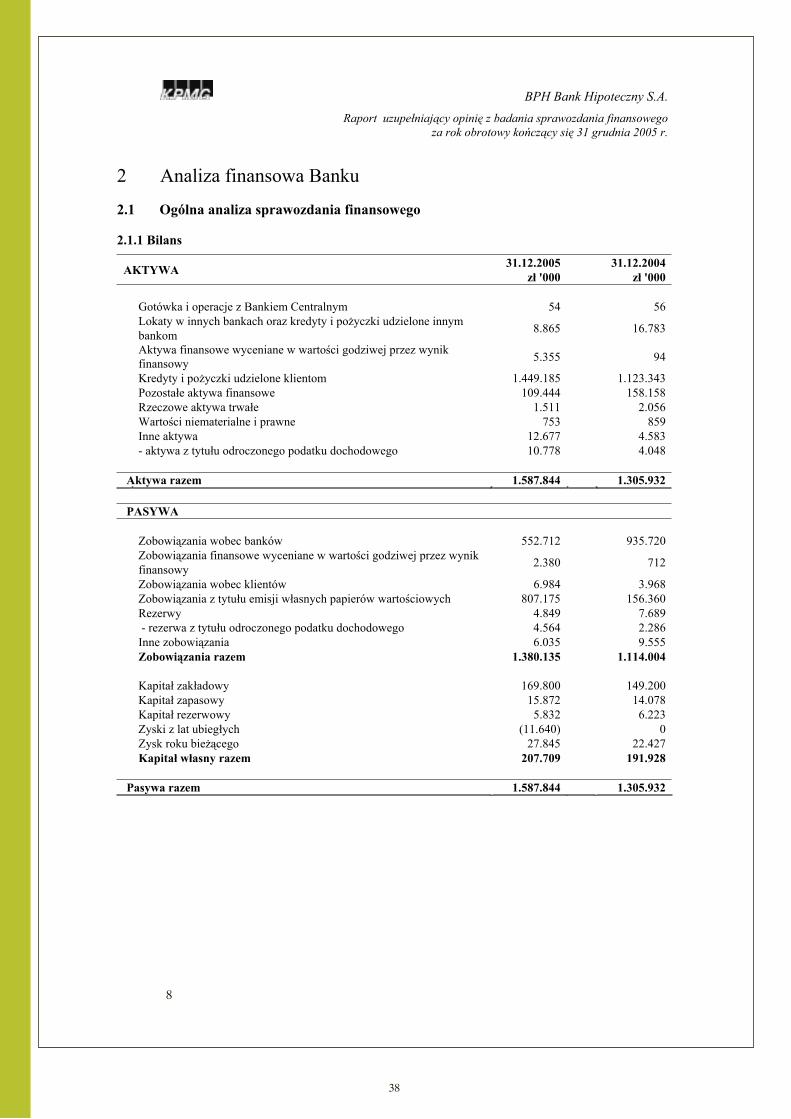

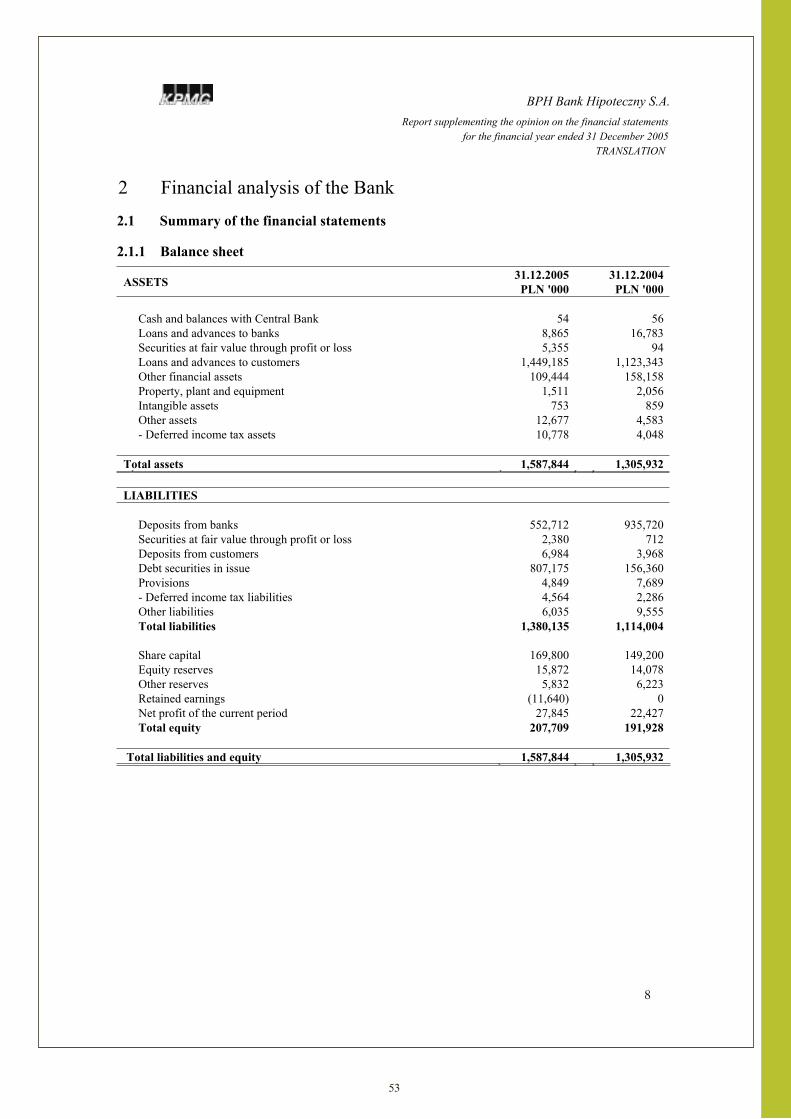

2005 2004w tys. zł w% w tys. zł w%

AktywaKredyty i pożyczki zabezpieczone hipoteką 1 417 751 89,29 1 090 058 83,47Kredyty i pożyczki niezabezpieczone hipoteką 31 434 1,98 33 285 2,55Pozostałe aktywa finansowe 109 444 6,89 158 158 12,11Inne 29 215 1,84 24 431 1,87Aktywa razem 1 587 844 100,00 1 305 932 100,00

PasywaZobowiązania wobec banków 552 712 34,81 935 720 71,65Zobowiązania z tytułu emisji własnych papierów wartościowych 807 175 50,83 156 360 11,97Kapitał własny 207 709 13,08 191 928 14,70Inne 20 248 1,28 21 924 1,68Pasywa razem 1 587 844 100,00 1 305 932 100,00

13

Szczegółowy opis istotnych czynników ryzyka i zagrożeń (ryzyko stóp procentowych, ryzyko płynności, ryzyko wymiany walutowej, ryzyko operacyjne, ryzyko kredytowe) oraz wysokość limitów wynikających z ustawy o listach zastawnych i bankach hipotecznych zamieszczony został w sprawozdaniu finansowym.

6

KIERUNKI ROZWOJU I NAJWAŻNIEJSZE ELEMENTY STRATEGII BANKU NA ROK 2006

W 2005 roku BPH Bank Hipoteczny S.A. kontynuował działania wynikające z założeń strategii Banku na lata 2004 – 2006 oraz dążył do osiągnięcia wyników przyjętych w pla-nie finansowym na 2005 rok.

W roku 2006 Bank będzie dostosowywał swą działalność do istniejących i przewidywanych uwarunkowań ekono-micznych i prawnych, oczekiwań głównego akcjonariusza i klientów oraz własnych możliwości, mając szczególnie na uwadze jakościowy aspekt rozwoju, tj. trwałą poprawę efektywności działania.

Główne cele finansowe przyjęte na rok 2006 to:

Wskaźnik ROE brutto - 20%

Cost/Income – poniżej 35%Perspektywy dalszego rozwoju Banku rysują się dobrze.

Bank posiada atrakcyjną ofertę produktową oraz efektywne procesy. Postępuje rozwój rynku nieruchomości i wzrasta zapotrzebowanie na długoterminowe kredyty na nierucho-mości komercyjne. Utrzymuje się popyt na rynku kredytów mieszkaniowych, które są istotnym instrumentem dywersy-fikacji portfela kredytowego. Współpraca w ramach Grupy BPH, zwłaszcza w związku z wysokim udziałem Banku BPH S.A. w rynku finansowania nieruchomości, pozytywnie rokuje na powodzenie programu emisji.

Na osiągnięcie planowanego wyniku brutto 2006 roku będą miały wpływ m.in. następujące założenia:

– przyspieszenie tempa wzrostu gospodarczego – wzrost PKB szacuje się na ok. 4,6%;

– przewidywane zwiększenie inwestycji przedsiębiorstw, po-prawa kondycji gospodarstw domowych (stopniowy spadek stopy bezrobocia), ustabilizowana na niskim poziomie inflacja wspierana przez niski poziom rynkowych stóp pro-centowych;

– prosprzedażowe działania Banku mające na celu zwiększe-nie akcji kredytowej, takie jak np.: dostosowywanie oferty do potrzeb i oczekiwań Klientów, podnoszenie efektywno-ści procesu udzielania kredytów itp.;

– ścisła kontrola kosztów administracyjnych w celu utrzyma-nia kosztów działania Banku na poziomie zbliżonym do 2005 r.

Na potencjalne zmniejszenie wyniku może natomiast wpły-nąć m.in. spodziewana presja na obniżanie marż, wynikają-ca ze zwiększającej się konkurencji na rynku bankowym.

7

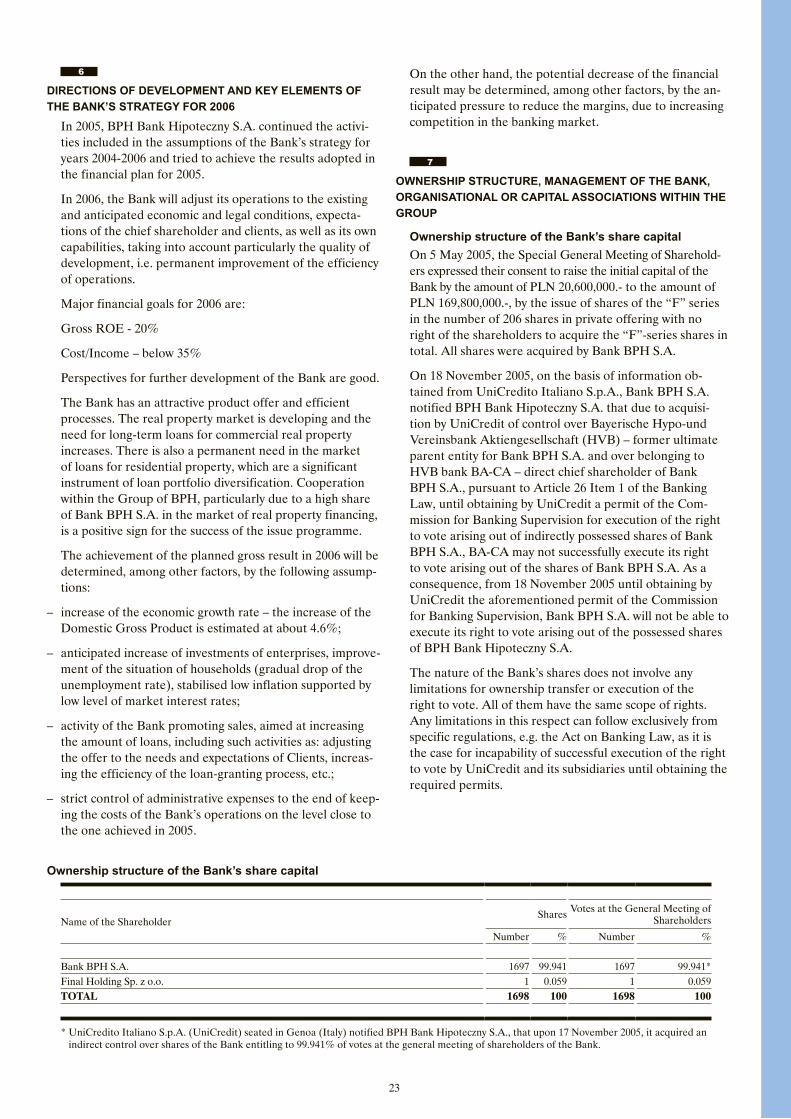

STRUKTURA WŁASNOŚCIOWA, WŁADZE BANKU, POWIĄZANIA ORGANIZACYJNE LUB KAPITAŁOWE W RAMACH GRUPY

W dniu 5 maja 2005 r. Nadzwyczajne Walne Zgromadzenie Akcjonariuszy wyraziło zgodę na podwyższenie kapitału zakładowego Banku, o kwotę 20 600 000,- PLN do kwoty 169 800 000,-PLN, poprzez emisję akcji serii „F” w ilości 206 akcji w drodze subskrypcji prywatnej z pozbawieniem akcjonariuszy prawa poboru akcji serii „F” w całości. Akcje w całości objął Bank BPH S.A.

W dniu 18 listopada 2005 r., na podstawie informacji uzyskanej z UniCredito Italiano S.p.A., Bank BPH S.A. po-informował BPH Bank Hipoteczny S.A. o tym, iż w związku z przejęciem przez UniCredit kontroli nad Bayerische Hy-po-und Vereinsbank Aktiengesellschaft (HVB) – dotych-czasowym ostatecznym podmiotem dominującym dla Ban-ku BPH S.A. oraz nad należącym do HVB bankiem BA-CA – bezpośrednim większościowym akcjonariuszem Banku BPH S.A. zgodnie z Art. 26 ust. 1 Prawa bankowego, do czasu uzyskania przez UniCredit zgody Komisji Nadzoru Bankowego (KNB) na wykonywanie prawa głosu z posia-danych pośrednio akcji Banku BPH S.A., BA-CA nie może wykonywać skutecznie prawa głosu z akcji Banku BPH S.A. Oznacza to w konsekwencji, iż od dnia 18 listopada 2005 r. do czasu uzyskania przez UniCredit wymienionej zgody KNB, Bank BPH S.A. nie będzie mógł wykonywać prawa głosu z posiadanych akcji BPH Banku Hipotecznego S.A.

Z istoty akcji Banku nie wynikają ograniczenia przenosze-nia własności oraz wykonywania prawa głosu. Wszystkie charakteryzuje ten sam zakres uprawnień. Ograniczenia w tym zakresie mogą mieć miejsce jedynie na gruncie prze-pisów szczególnych, np. na gruncie ustawy Prawo bankowe,

Struktura własnościowa kapitału akcyjnego Banku

Nazwa akcjonariuszaAkcje Głosy na WZA

Ilość % Ilość %

Bank BPH S.A. 1697 99,941 1697 99,941*Final Holding Sp. z o.o. 1 0,059 1 0,059Razem 1698 100 1698 100

* UniCredito Italiano S.p.A. (UniCredit) z siedzibą w Genui (Włochy) poinformował BPH Bank Hipoteczny S.A., iż z dniem 17 listopada 2005 r. nabył pośrednio kontrolę nad akcjami Banku stanowiącymi 99,941% głosów na walnym zgromadzeniu akcjonariuszy Banku.

14

– Rada NadzorczaW okresie 01.01.2005 r. – 31.12.2005 r. Rada Nadzorcza BPH Bank Hipoteczny S.A. działała w składzie:

jak ma to miejsce w przypadku braku możliwości skutecz-nego wykonywania prawa głosu przez UniCredit i jego pod-mioty zależne do czasu uzyskania niezbędnych zezwoleń.

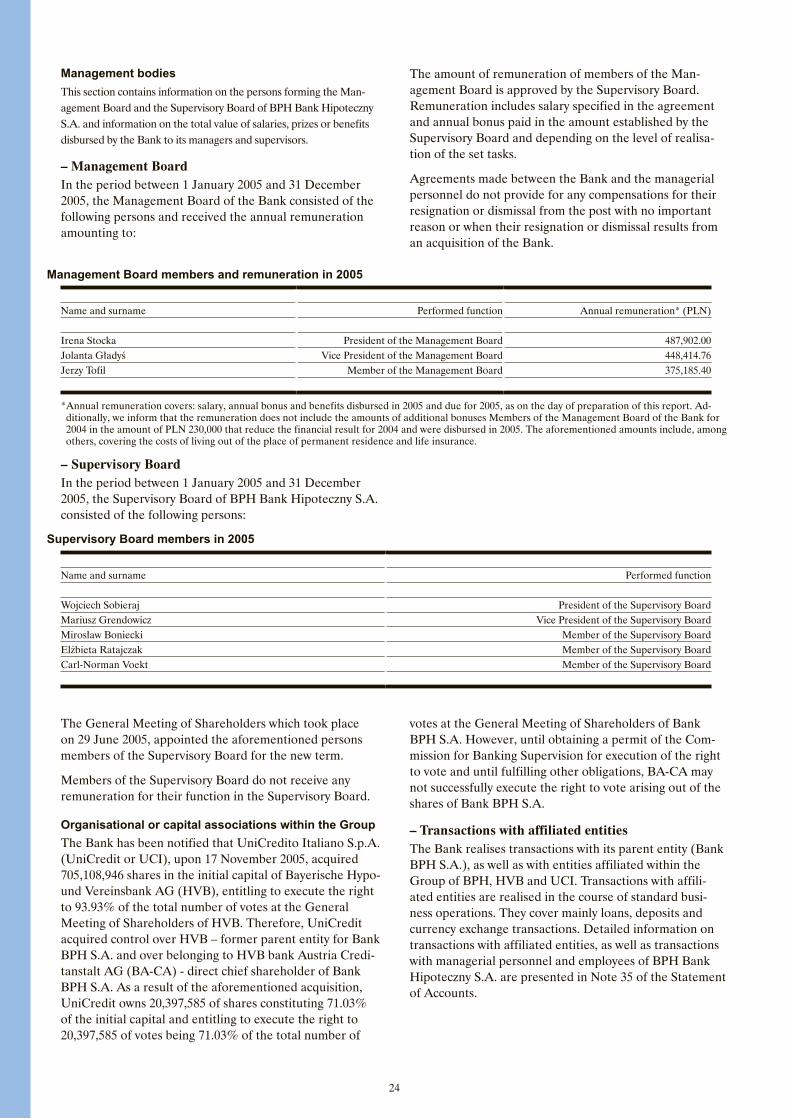

Organy władzyW tej części zawarte są informacje dotyczące składu osobo-wego Zarządu i Rady Nadzorczej BPH Bank Hipoteczny S.A. oraz informacje dotyczące łącznej wartości wynagro-dzeń, nagród lub korzyści wypłaconych przez Bank dla osób zarządzających i nadzorujących.

– ZarządW okresie 01.01.2005 r. – 31.12.2005 r. Zarząd Banku dzia-łał w następującym składzie i uzyskał roczne wynagrodzenie w wysokości:

Wysokość wynagrodzeń członków Zarządu zatwierdza Rada Nadzorcza. Wynagrodzenie składa się z wynagrodze-nia zasadniczego w wysokości określonej w umowie oraz premii rocznej wypłacanej w wysokości ustalanej przez Radę Nadzorczą i uzależnionej od stopnia realizacji wyzna-czonych zadań.

Umowy zawarte pomiędzy Bankiem a osobami zarządzają-cymi nie przewidują rekompensat w przypadku ich rezygna-cji lub zwolnienia z zajmowanego stanowiska bez ważnej przyczyny lub gdy ich odwołanie lub zwolnienie następuje z powodu połączenia Banku przez przejęcie.

Skład oraz wynagrodzenie Zarządu Banku w 2005 r.

Imię i nazwisko Pełniona funkcja Roczne wynagrodzenie* (zł)

Irena Stocka Prezes Zarządu 487 902,00Jolanta Gładyś Wiceprezes Zarządu 448 414,76Jerzy Tofil Członek Zarządu 375 185,40

* Roczne wynagrodzenie obejmuje: wynagrodzenie zasadnicze, premię roczną i korzyści, wypłacone w roku 2005 oraz należne za rok 2005, wg stanu na dzień sporządzenia niniejszego sprawozdania. Dodatkowo informujemy, iż wynagrodzenie nie obejmuje kwot premii rocznych dla Członków Zarządu

Banku za rok 2004 w kwocie 230 000,- zł obciążających wynik roku 2004, a wypłaconych w 2005 r. W wymienionych kwotach uwzględniono m.in. pokry-cie kosztów utrzymania poza miejscem zamieszkania oraz ubezpieczenie na życie.

Skład Rady Nadzorczej Banku w 2005 r.

Imię i nazwisko Pełniona funkcja

Wojciech Sobieraj Przewodniczący Rady NadzorczejMariusz Grendowicz Wiceprzewodniczący Rady NadzorczejMirosław Boniecki Członek Rady NadzorczejElżbieta Ratajczak Członek Rady NadzorczejCarl-Norman Voekt Członek Rady Nadzorczej

Zwyczajne Walne Zgromadzenie Akcjonariuszy, które mia-ło miejsce 29 czerwca 2005 r. powołało wyżej wymienione osoby do składu Rady Nadzorczej na nową kadencję.

Członkowie Rady Nadzorczej nie pobierają wynagrodzenia z tytułu pełnionej w Radzie Nadzorczej funkcji.

Powiązania organizacyjne lub kapitałowe w ramach GrupyBank został powiadomiony, że UniCredito Italiano S.p.A. (UniCredit lub UCI) nabył w dniu 17 listopada 2005 r. 705.108.946 akcji w kapitale zakładowym Bayerische Hypo- und Vereinsbank AG (HVB), uprawniających do wykony-wania 93,93% całkowitej liczby głosów na Walnym Zgroma-dzeniu HVB. W związku z tym UniCredit zyskał kontrolę nad HVB – dotychczasowym ostatecznym podmiotem dominującym dla Banku BPH S.A. oraz nad należącym do HVB Bankiem Austria Creditanstalt AG (BA-CA) – bez-pośrednim większościowym akcjonariuszem Banku BPH

S.A. W wyniku powyższego nabycia UniCredit pośrednio posiada 20.397.585 akcji stanowiących 71,03% kapitału zakładowego, uprawniających do wykonywania 20.397.585 głosów i stanowiących 71,03% całkowitej liczby głosów na Walnym Zgromadzeniu Banku BPH S.A., z zastrzeżeniem że do czasu uzyskania zezwolenia Komisji Nadzoru Banko-wego na wykonywanie prawa głosu oraz do czasu wypeł-nienia innych obowiązków, BA-CA nie może wykonywać skutecznie prawa głosu z akcji Banku BPH S.A.

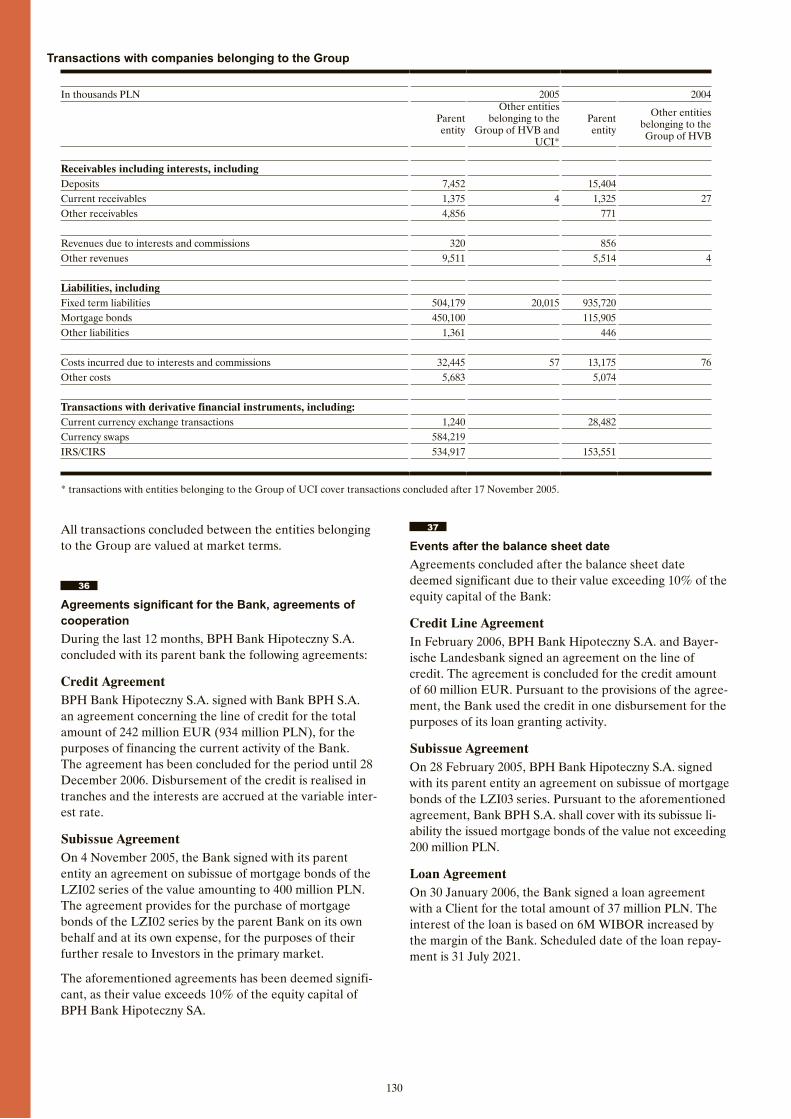

– Transakcje z jednostkami powiązanymi Bank przeprowadza transakcje z podmiotem dominującym (Bank BPH S.A.), oraz podmiotami powiązanymi w ra-mach Grupy BPH, HVB i UCI. Transakcje z jednostkami powiązanymi dokonywane są w ramach normalnej działal-ności biznesowej. Obejmują one głównie kredyty, depozyty, transakcje wymiany walut obcych. Szczegółowe informacje na temat transakcji z podmiotami powiązanymi, jak rów-

15

Zobowiązania warunkowe– Wszczęte postępowania sądowe

Na dzień 31 grudnia 2005 r. nie występują postępowa-nia przed sądem lub organami administracji państwowej dotyczące zobowiązań lub wierzytelności Banku, których wartość stanowiłaby, co najmniej 10% kapitałów własnych Banku.

Łącznie wartość wszystkich prowadzonych spraw sądowych wynosi 22 021 tys. zł, co stanowi 10,60% kapitałów własnych Banku. Wyżej wymieniona kwota stanowi wartość przed-miotu sporu w sprawach z powództwa (wniosku) Banku.

Na dzień 31 grudnia 2005 r. nie występują postępowania przed sądem lub organami administracji państwowej, w których Bank jest pozwanym.

W 2005 r. bank wystawił 9 tytułów egzekucyjnych na łączną kwotę 4 975 tys. zł. wartość zabezpieczeń ustanowionych na majątku kredytobiorców (hipoteki), wobec których zostały wystawione tytuły egzekucyjne, ukształtowała się na pozio-mie 6 574 tys. zł.

– Zobowiązania warunkowe do udzielenia kredytów

Bank posiada zobowiązania do udzielenia kredytów na łaczną kwotę 23 683 tys. zł.

– Inne zobowiązania związane z transakcjami pozabilansowymi

Wartość zobowiązań z tytułu zawartych transakcji instru-mentami fiansowymi bieżącymi i terminowymi wynosi 1 120 375 tys. zł.

W roku 2005 Bank nie udzielił żadnych gwarancji i porę-czeń.

Pozostałe informacje– Bank nie zawierał i nie zna umów, w wyniku których

w przyszłości mogłyby nastąpić zmiany w proporcjach posiadanych akcji przez dotychczasowych akcjonariuszy i obligatariuszy.

– Nie zawarto istotnych umów pomiędzy Bankiem a Bankiem Centralnym lub organami nadzoru.

Podmiot uprawniony do badania sprawozdania finansowegoW dniu 21 listopda 2005 r. Bank zawarł z KPMG Audyt Spółka z o.o. umowę o badanie sprawozdania finansowego. Łączna wysokość wynagrodzenia, wynikająca z ww umowy, wynosi brutto 103 700,00 zł. Zapłacono I ratę w wysokości 51 850,00 zł. Druga rata, zgodnie z umową, będzie zapła-cona po przedstawieniu ostatecznej wersji opinii i raportu w kwocie 51 850,00 zł.

Podmiotem przeprowadzajacym badanie sprawozdania finansowego Banku w 2004 r. był KPMG Audyt Spółka z o.o., a łączna wartość wynagrodzenia wyniosła brutto 89 182,00 zł.

W 2005 roku Bank zawarł z KPMG Sp. z o.o. umowy na usługi doradcze.

nież transakcje z personelem zarządczym oraz z pracowni-kami BPH Banku Hipotecznego S.A. znajdują się w nocie 35 Sprawozdania finansowego.

– Umowy znaczące zawarte w ramach jednostek powią-zanych

W 2005 r. BPH Bank Hipoteczny S.A. zawarł z Bankiem BPH S.A. następujące umowy:

– Umowa linii kredytowej

na łączną kwotę 242 mln EUR (934 mln zł), w celu fi-nansowania działalności kredytowej. Umowa przewiduje udostępnianie kredytu w transzach, jego oprocentowanie jest zmienne. Termin spłaty przewidziany jest na 28 grudnia 2006 r.

Wg stanu na koniec roku zobowiązanie z tytułu zaciągnię-tego kredytu wynosiło 504 187 tys. zł. Termin spłaty zadłu-żenia tej transzy nie przekraczał 1 miesiąca.

– Umowa o subemisję

zawarta w dniu 4 listopada 2005 r. umowa o subemisję usłu-gową hipotecznych listów zastawnych Serii LZI02 na kwotę 400 mln zł. Umowa przewiduje nabycie listów zastawnych serii LZI02 przez Bank BPH S.A we własnym imieniu i na własny rachunek w celu dalszego ich zbywania Inwestorom w obrocie pierwotnym.

Powyższe umowy zostały uznane za znaczące, ponieważ ich wartośc przekracza 10% funduszy własnych Banku.

8

DODATKOWE INFORMACJE

Umowy znaczące dla Banku zawarte po dacie bilansowejUmowy zawarte po dniu bilansowym przekraczajace 10% kapitałów własnych Banku:

– Umowa dotycząca linii kredytowej

podpisana w lutym 2006 r. pomiędzy BPH Bank Hipotecz-ny S.A. i Bayerische Landesbank. Umowa opiewa na kwotę 60 mln EUR. Zgodnie z warunkami umowy Bank wyko-rzystał kredyt jednorazowo i przeznaczył na finansowanie działalności kredytowej.

Termin spłaty kredytu - 24 lutego 2009 r.

– Umowa o subemisję

zawarta w dniu 28 lutego 2006 r. z Bankiem BPH S.A. umo-wa o subemisję usługową hipotecznych listów zastawnych serii LZI03. Zgodnie z ww umową Bank BPH S.A. obejmie zobowiązaniem subemisyjnym wyemitowane listy zastawne o wartości nie większej niż 200 mln zł.

– Umowa dotycząca udzielenia kredytu

W dniu 30 stycznia 2006 r. Bank zawarł z Klientem umowę kredytową na łączną kwotę 37 mln zł. Oprocentowanie kredytu oparte jest o stawkę 6M WIBOR powiększoną o marżę Banku. Termin spłaty kredytu przewidziany jest na 31 lipca 2021 r.

16

9

OŚWIADCZENIA ZARZĄDU

Zasady ładu korporacyjnego i społecznej odpowiedzialnościBPH Bank Hipoteczny S.A. kieruje się w swej działalności zasadami społecznej odpowiedzialności i jest wrażliwy na potrzeby klientów i akcjonariuszy.

Bank w pełni stosuje zasady zawarte, w przyjętych przez Zarząd Banku:

– „Instrukcji - Zachowania pracowników oraz przestrzegania przepisów przy zawieraniu transakcji związanych z nieru-chomościami”;

– „Regulaminie udzielania kredytów oraz otwierania rachun-ków lokat terminowych akcjonariuszom, członkom orga-nów i pracownikom”;

– „Regulaminie Compliance w zakresie obrotu papierami wartościowymi emitowanymi przez Bank”.

Prawdziwość i rzetelność prezentowanych sprawozdańWedle najlepszej wiedzy Zarząd BPH Banku Hipotecznego S.A. prezentuje roczne dane finansowe i dane porównywal-ne za rok 2004. Dane sporządzone zostały zgodnie z obo-wiązującymi zasadami rachunkowości oraz odzwierciedlają w sposób prawdziwy, rzetelny i jasny sytuację majątkową i finansową Banku oraz osiągnięty wynik finansowy. Zawar-te w niniejszym dokumencie roczne sprawozdanie Zarządu zawiera prawdziwy obraz rozwoju, osiągnięć oraz sytuacji Banku, w tym opis istotnych ryzyk i zagrożeń.

Irena Stocka Prezes Zarządu

Jolanta Gładyś Wiceprezes Zarządu

Jerzy Tofil Członek Zarządu

Warszawa, 24 marca 2006 roku

17

1

SELECTED FINANCIAL DATA OF THE BANK ACHIEVED IN 2005

MANAGEMENT BOARD REPORT MANAGEMENT BOARD REPORT ON OPERATIONS OF THE BANK IN THE REPORTING PERIOD FROM 1 JANUARY 2005 TO 31 DECEMBER 2005

Selected financial data of the Bank

Specification 31.12.2004 31.12.2005 Change (dynamics) (%)

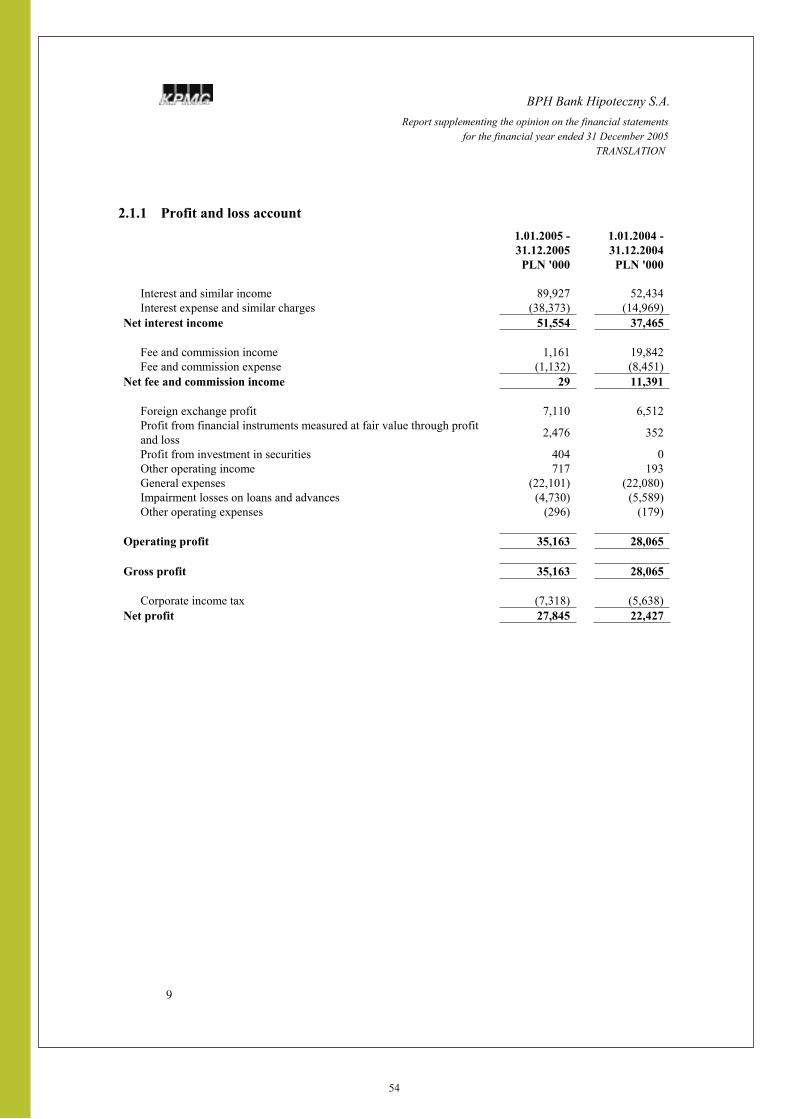

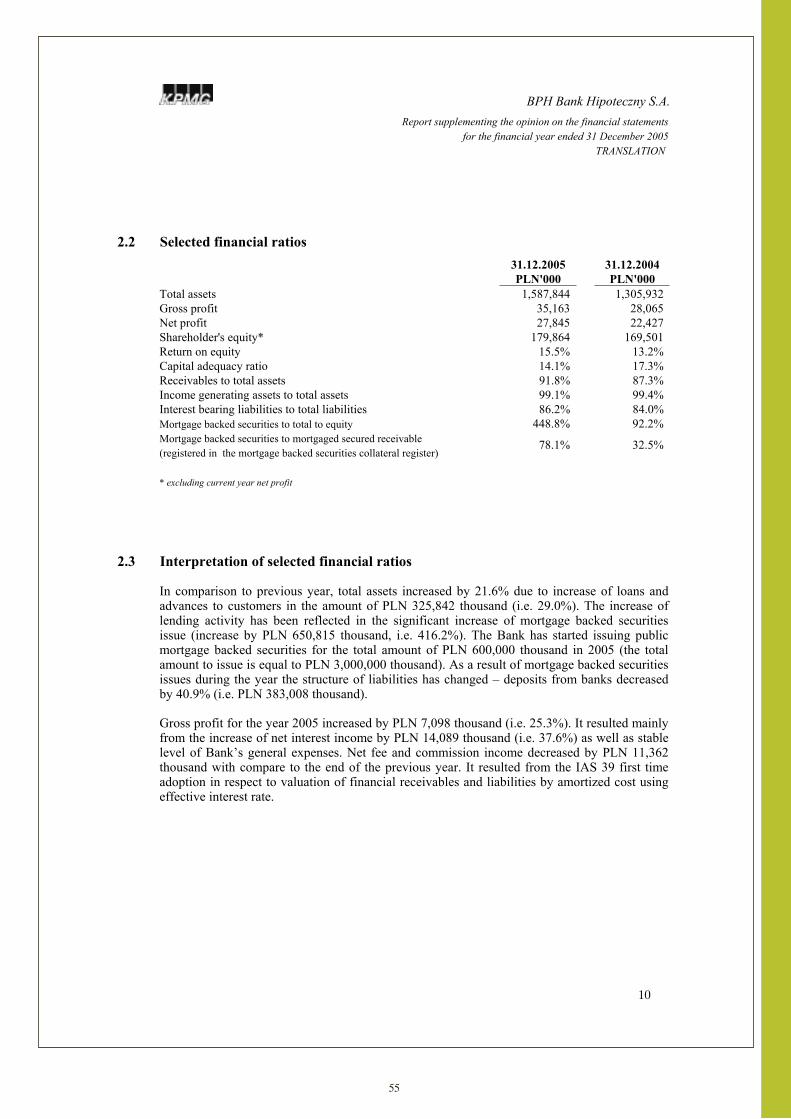

Profit and loss account in thousands PLN Financial result on interests 37,465 51,554 137.6%Financial result on commissions 11,391 29 0.03%Financial result on currency exchange and operations with financial instruments 6,864 9,990 145.5%Revaluation write-offs due to impairment -5,589 -4,730 84.6%Costs of operation and general management -22,080 -22,101 100.1%Other operating costs and revenues 14 421 3 007.1%Gross profit 28,065 35,163 125.3%Net profit 22,427 27,845 124.2%Balance sheet in thousands PLN Balance sheet total 1,305,932 1,587,844 121.6%Net receivables from clients 1,123,343 1,449,185 129.0%Liabilities due to the issue of mortgage bonds 156,360 807,175 516.2%Own capital 191,928 207,709 108.2%Ratios (%) Gross Return on Equity (Gross ROE) 14.6% 16.9% 115.8%Net Return on Equity (Net ROE) 11.7% 13.4% 114.7%Return on Assets (ROA) 2.1% 2.2% 103.0%Interest margin on assets - total 2.9% 3.2% 113.2%Costs-to-Revenues ratio 40% 36% 90.3%Solvency ratio 17.3% 14.1% 81.5%

18

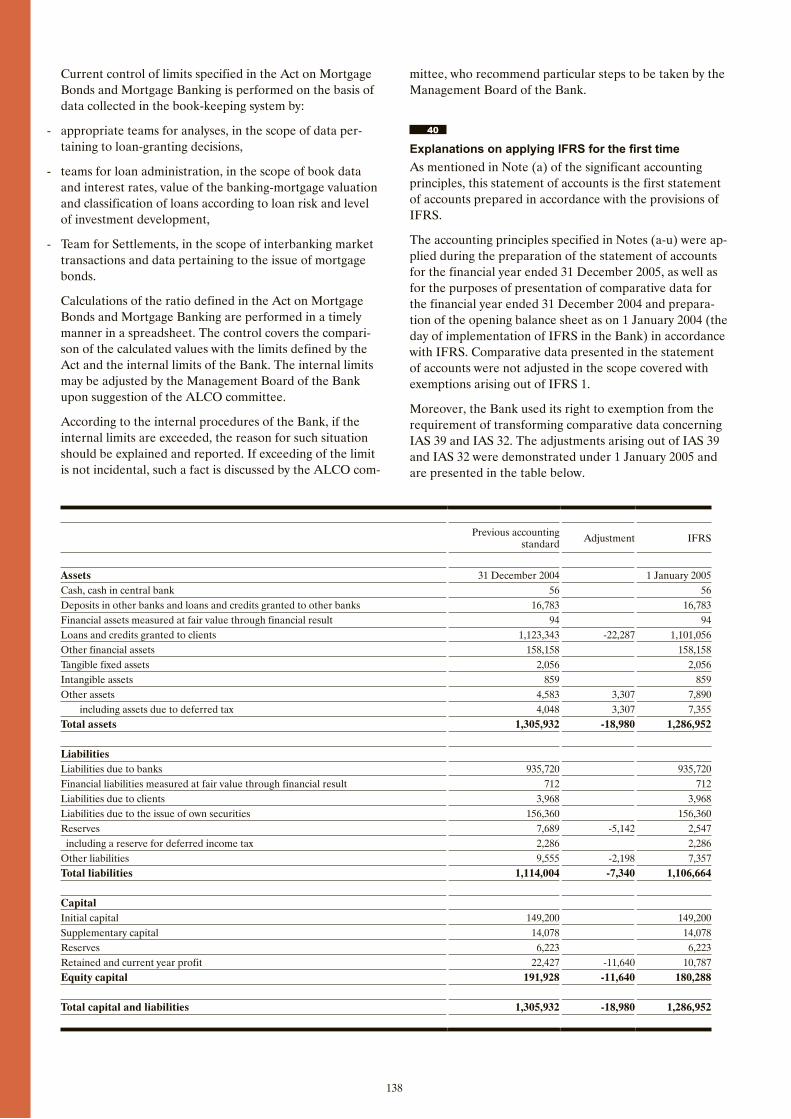

Due to using the allowable exemptions provided by IFRS 1, the data for 2005 are not fully comparable to the data for 2004. The most significant changes resulting from the implementation of the International Financial Reporting Standards are connected with the introduction of valua-tion according to the effective interest rate and changes of the principles of creating revaluation write-offs due to impairment. Items whose values in the opening balance sheet has been subject to significant changes include: loans and credits granted to clients, assets due to deferred tax, reserves and retained profit/loss. The amount of the adjust-ment to the opening balance sheet demonstrated in capitals amounts to 11,640 thousands PLN (reduction). Detailed explanation of the influence of the implementation of IFRS on particular items of the statement of accounts is presented in Note 40.

BPH Bank Hipoteczny S.A. is the second largest, taking into account the amount of assets and the volume of loans, dynamically developing specialised bank in Poland. Finan-cial results of the Bank for 2005 are demonstrated in the chapter Financial Results for 2005.

Chief shareholder of the Bank is Bank BPH S.A., one of the largest banks in Poland, listed in the Warsaw Stock Exchange (GPW).

The Bank belongs to the Capital Group of Bank BPH S.A. and its statements of accounts, for the purposes of supervi-sion, are consolidated with the statements of accounts of Bank BPH S.A.

The statements of the Capital Group of Bank BPH S.A. are directly consolidated with the statements of accounts of Austria Creditanstalt AG (BA-CA) Bank seated in Vienna, which is the chief shareholder of Bank BPH S.A. The par-ent entity for BA-CA is Bayerische Hypo- und Vereinsbank AG (HVB), whose parent entity is UniCredito Italiano S.p.A. (UCI) – the chief shareholder of HVB.

The operations of the Bank in the reporting period, its dynamics and fields of activity were determined by the role and position of the Bank in the Group of Bank BPH.

2

MACROECONOMIC SITUATION IN 2005, INCLUDING THE BANKING SECTOR

According to the initial estimations of the Central Sta-tistical Office (GUS), the economic growth rate in 2005 amounted to 3.2%. On the basis of the annual data, it is estimated that the real dynamics of the GDP in the fourth quarter of 2005 amounted to about 4.0% YoY. The rate of return on investments in business in 2005 reached 6.2%, which indicates their two-digit increase, not observed since the fourth quarter of 1999, in the fourth quarter (about 10.0% YoY).

No inflation threats due to external demand, connected with the decreasing rate of prices of goods and services (a decrease from 3.7% YoY in January to 0.7% YoY in De-cember) encouraged the Monetary Policy Council (RPP) to reduce interest rates by five times in 2005, by 200 bps in total. As on the end of December 2005, the reference

rate of the National Bank of Poland amounted to 4.50% in January (in January, it was 6.50%). The most significant reductions of interest rates took place in the first half of the year (by 150 bps in total), when the Central Statistical Office published data on the economic growth in the first quarter of 2005, which were far from expectations. While the macroeconomic ratios improved, the Monetary Policy Council adopted a more reserved attitude and introduced last reductions in July and August, by 50 bps in total. Reductions of the interest rates were accompanied by the changes of attitude in monetary policy: from restrictive in January to mild in February; next, in April, the mild atti-tude changed to a neutral one, while in June, mild attitude returned and prevailed until the end of the year.

The dynamics of investments in 2005 at the level of 6.2% was higher than the expectations in the end of 2005 and, at the same time, much lower than the former prognoses, e.g. in the first quarter of 2005. The lowest rate of increase of gross expenses on fixed assets was reported in the first quarter (1.2% YoY), while in the following quarters it gradually increased: to 3.8% YoY in the second quarter, 5.7% in the third quarter and about 10.0% YoY in the last quarter. Low investment activity of companies (whose total share in domestic investments amounts to about 53%) in the first quarter of the year was determined by serious problems with obtaining EU structural funds, as well as un-certainty concerning the shaping of investment conditions after the presidential and parliamentary elections.

In the banking sector in 2005, further boost of the loan dynamics for both business entities and households was observed. Similarly as in 2004, volumes of mortgage loans increased rapidly – the dynamics exceeded 40% by the end of the year. It was a result of milder loan-granting poli-cies of banks, reduction of costs of loans, as well as the improvement of financial situation of households. The most significant reason for changes in loan policies is the increase of the pressure of competition between the banks.

Due to increasing competition in the banking sector, the banks, struggling to acquire new clients, decide to lower their margins on loans, as well as fees and commissions involved in the loan-granting process. The loan-granting procedures are simplified and loan periods are extended.

3

OPERATIONS OF BPH BANK HIPOTECZNY S.A.

BPH Bank Hipoteczny Spółka Akcyjna (Joint-Stock Com-pany) operates on the basis of the Act on Mortgage Bonds and Mortgage Banking of 29 August 1997 and the Reso-lution No. 244/KNB/99 of the Commission for Banking Supervision of 1 December 1999.

The aforementioned basis for the Bank’s operations states that BPH Bank Hipoteczny S.A. may operate in two fields: granting mortgage loans and loans for territorial self-gov-ernment units and issuing mortgage bonds.

Loan activityIn 2005, the Bank focused on developing a safe loan port-folio through granting loans for financing commercial and

19

residential real estates. The Bank directed its loan offer both to entrepreneurs and private people. Purposes of loans included: purchase, construction, modernisation or renovation of commercial or residential properties for own use or for commercial use. The loan could also be used for the purposes of refinancing a loan taken from another bank or refinancing own contribution of the client in the investment. Loans are granted in PLN (Polish zlotys), as well as indexed in foreign currencies (USD, EUR, CHF). Sales were performed by a group of the Bank’s banking advisers and a network of over 180 sales partners, as well as by branches of Bank BPH S.A.

In 2005, the Bank granted 568 loans of the total amount of 563 million PLN. The portfolio of mortgage loans increased by 27% as compared to 2004 and achieved the value of 1.48 billion PLN as on the end of 2005.

Most of all, the Bank focused on financing commercial real property investments. The offer of the Bank, adjusted to expectations of commercial clients, enabled the acquisition of 190 new clients, which constituted an increase by 36% as compared to the previous year and realisation of 447 mil-lion PLN of the volume in this segment.

Key success factors:

– Very attractive offer for entrepreneurs and flexibility in adjusting loans to individual needs and capabilities of these clients.

– Development of cooperation with Sales Partners and im-proving their qualifications in the field of cooperation with Clients.

– Supporting mortgage loans for flats by a marketing cam-

paign concerning refinancing of mortgage loans for flats.

Continuation of this growth tendency in revenues in this field of the Bank’s operations was supported in 2005 by positive influence of market interest rates on the loan margin.

In 2005, the share of loans with reported impairment, for which the Bank created specific target reserves, remained at a safe level of 2.9%, while the ratio of specific target reserves created for these receivables to the total value of the loan portfolio amounted to 1.2%.

Total amount of the bank-mortgage value of real property accepted by the Bank as security of mortgage loans, as on 31 December 2005, amounted to 3,102,763 thousand PLN.

Issue of mortgage bondsOut of all 4 mortgage banks in Poland, only BPH Bank Hipoteczny S.A. and BRE Bank Hipoteczny S.A. perform public issues of mortgage bonds. The Bank elaborated a programme of own issue of mortgage bonds, in the course of which it plans to issue mortgage bonds of the total value of 3 billion PLN within 5 years.

In 2005, the following public issues were carried out:

Issues within the Programme of public issue of mortgage bonds of the total value of 3 billion PLN

02 June 2005 200,000.0021 November 2005 400,000.00Issues in total 600,000.00

Mortgage loans granted in 2005

Loans secured byLoans granted in 2005 Loan portfolio as on 31 December 2005

Number Volume (in millions PLN) Volume (in billions PLN)

mortgage on residential real property 378 117 0.15mortgage on commercial real property 190 447 1.33Total 568 563 1.48

Value of issue on 31 December 2005

BRE bank Hipoteczny S.A.BPH bank Hipoteczny S.A.

1200

900

600

300

In thousands PLN

20

In 2005, the Bank carried out the non-public issue of mort-gage bonds of the total value of 150 million PLN. The value of the issued mortgage bonds in the form of a non-public issue, as on the end of the year, amounts to 190,000 thou-sand PLN and 3,630 EUR. The issue of mortgage bonds in PLN is performed in accordance with the provisions of the Agreement on Realisation of the Programme of Debt Securities Issue of 2003, while the issue in foreign currency is based on the Issue Agreement of 2000.

The public or non-public issue is based on debts registered in the mortgage bonds hedging register. The value of debts that hedge the issue, as on the end of 2005, amounts to 1,030,179 thousands PLN.

The resources obtained owing to the issue of mortgage bonds enable refinancing of the Bank’s operations in the field of loans, without the necessity to increase the initial capital.

4

FINANCIAL RESULTS FOR 2005

In 2005, the Bank managed to achieve very good financial results, which enabled strengthening its competitive posi-tion in the market segment of specialised mortgage banks.

The increase of the balance sheet amount of the Bank, as compared to the previous year, amounted to 281,912 thou-sand PLN. Net profit reached the level of 27,845 thousand PLN, i.e. the increase amounted to 5,418 thousand PLN.

What had the most significant influence on the achieved financial result was the result on interests. The increase of the financial result on interests was possible owing to the increase of the loan volume and the increase of the margin due to effective commission calculation. Another important factor, which had its influence on achieving good financial result, was keeping a restrictive policy of expenses.

Major economic ratios and values of selected items of the financial results are demonstrated in the diagrams below.

31 Dec 2004 31 Dec 2005

3,4%

3,2%

3,0%

2,8%

in %

31Dec 200431Dec 2005

2,22%

2,19%

2,16%

2,13%

in %

ROATotal interest margin on assets

31 Dec 200431 Dec 2005

14,0%

13,0%

12,0%

11,0%

in %

31 Dec 200431 Dec 2005

18,0%

16,5%

15,0%

13,5%

in %

ROE - gross ROE - nett

21

31 Dec 200431 Dec 2005

20,0%

15,0%

10,0%

5,0%

in %

31 Dec 200431 Dec 2005

42,0%

40,0%

38,0%

36,0%

in %

Costs/Profits Ratio Solvency Ratio

31 Dec 200431 Dec 2005

28 000

21 000

14000

7 000

in thousands PLN

31 Dec 200431 Dec 2005

40 000

30 000

20 000

10 000

in thousands PLN

Result on operating activityCosts of operation and management

31 Dec 200431 Dec 2005

2 000 000

1 500 000

1 000 000

500 000

in thousands PLN

Loan

s and

cred

it

grante

d to c

lients

Liabil

ities d

ue to

issu

e

of ow

n sec

uritie

s

Changes in the major balance sweet items

22

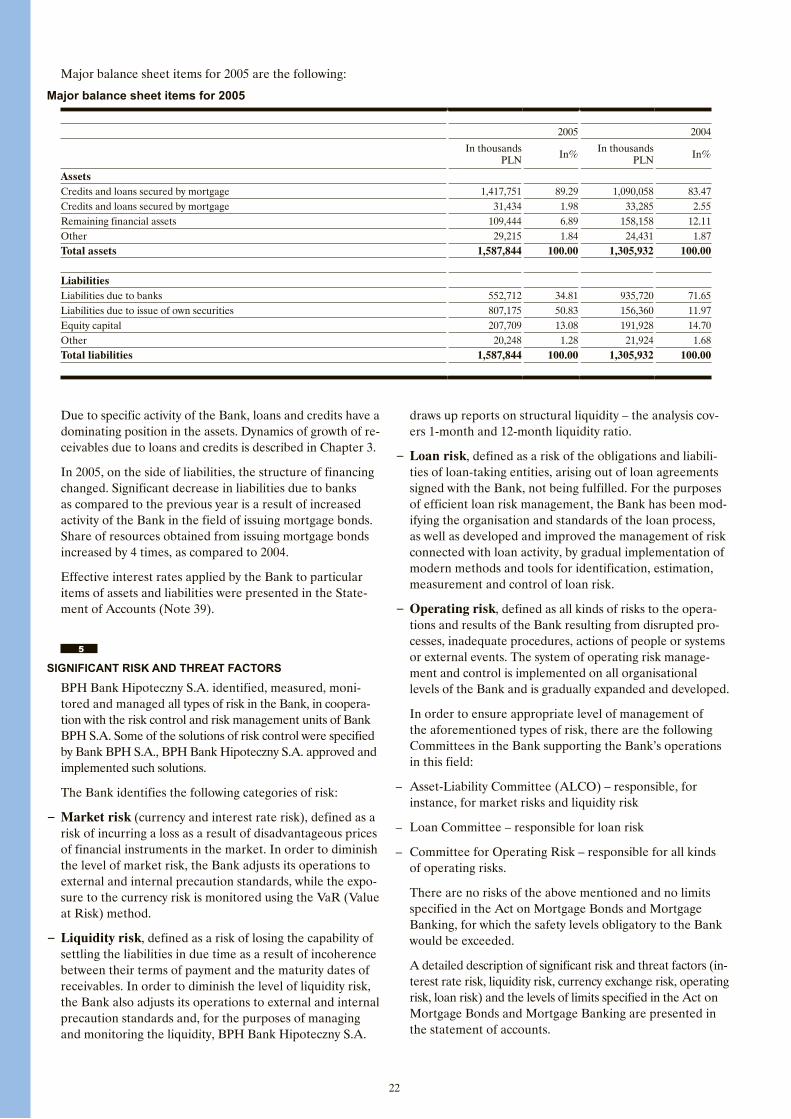

Major balance sheet items for 2005 are the following:

draws up reports on structural liquidity – the analysis cov-ers 1-month and 12-month liquidity ratio.

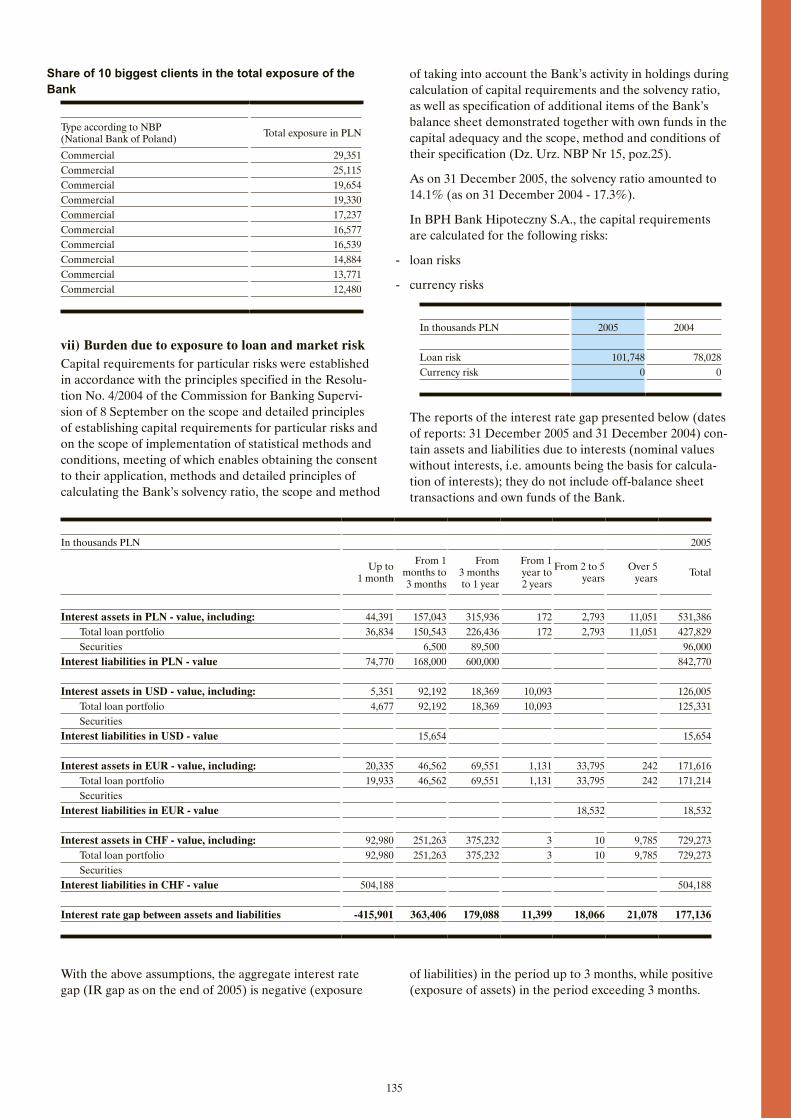

− Loan risk, defined as a risk of the obligations and liabili-ties of loan-taking entities, arising out of loan agreements signed with the Bank, not being fulfilled. For the purposes of efficient loan risk management, the Bank has been mod-ifying the organisation and standards of the loan process, as well as developed and improved the management of risk connected with loan activity, by gradual implementation of modern methods and tools for identification, estimation, measurement and control of loan risk.

− Operating risk, defined as all kinds of risks to the opera-tions and results of the Bank resulting from disrupted pro-cesses, inadequate procedures, actions of people or systems or external events. The system of operating risk manage-ment and control is implemented on all organisational levels of the Bank and is gradually expanded and developed.

In order to ensure appropriate level of management of the aforementioned types of risk, there are the following Committees in the Bank supporting the Bank’s operations in this field:

– Asset-Liability Committee (ALCO) – responsible, for instance, for market risks and liquidity risk

– Loan Committee – responsible for loan risk

– Committee for Operating Risk – responsible for all kinds of operating risks.

There are no risks of the above mentioned and no limits specified in the Act on Mortgage Bonds and Mortgage Banking, for which the safety levels obligatory to the Bank would be exceeded.

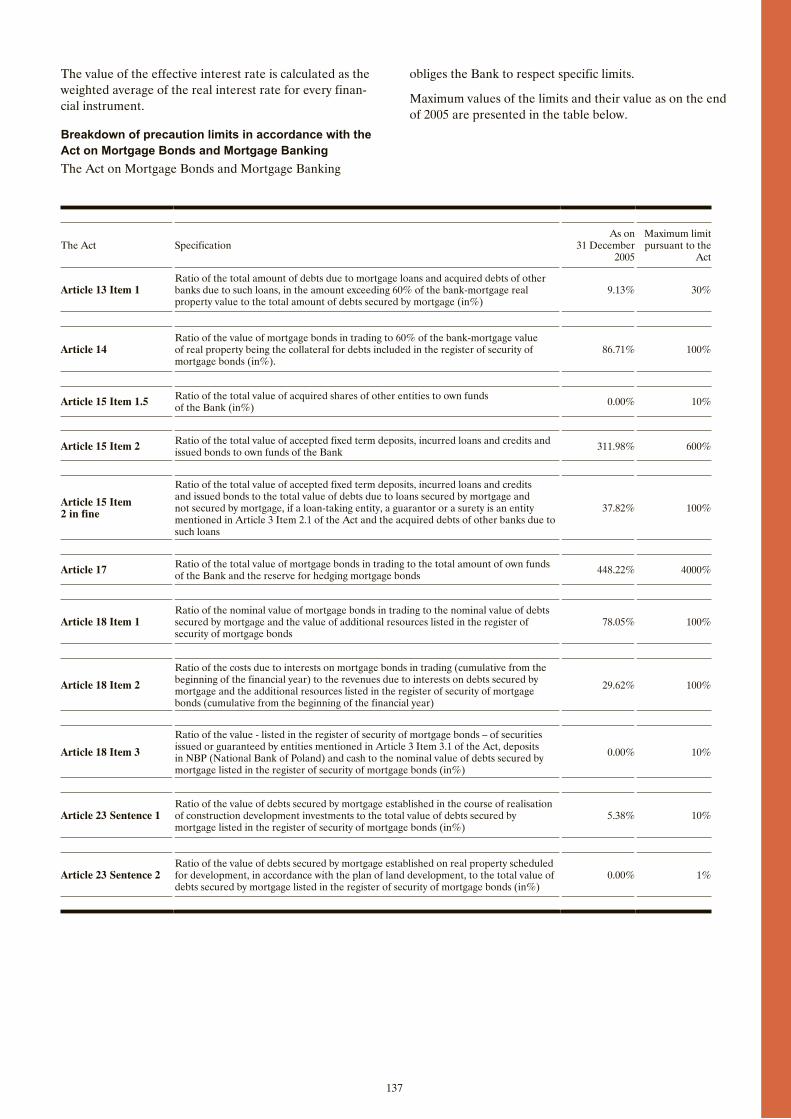

A detailed description of significant risk and threat factors (in-terest rate risk, liquidity risk, currency exchange risk, operating risk, loan risk) and the levels of limits specified in the Act on Mortgage Bonds and Mortgage Banking are presented in the statement of accounts.

Major balance sheet items for 2005

2005 2004

In thousands PLN In% In thousands

PLN In%

AssetsCredits and loans secured by mortgage 1,417,751 89.29 1,090,058 83.47Credits and loans secured by mortgage 31,434 1.98 33,285 2.55Remaining financial assets 109,444 6.89 158,158 12.11Other 29,215 1.84 24,431 1.87Total assets 1,587,844 100.00 1,305,932 100.00

LiabilitiesLiabilities due to banks 552,712 34.81 935,720 71.65Liabilities due to issue of own securities 807,175 50.83 156,360 11.97Equity capital 207,709 13.08 191,928 14.70Other 20,248 1.28 21,924 1.68Total liabilities 1,587,844 100.00 1,305,932 100.00

Due to specific activity of the Bank, loans and credits have a dominating position in the assets. Dynamics of growth of re-ceivables due to loans and credits is described in Chapter 3.

In 2005, on the side of liabilities, the structure of financing changed. Significant decrease in liabilities due to banks as compared to the previous year is a result of increased activity of the Bank in the field of issuing mortgage bonds. Share of resources obtained from issuing mortgage bonds increased by 4 times, as compared to 2004.

Effective interest rates applied by the Bank to particular items of assets and liabilities were presented in the State-ment of Accounts (Note 39).

5

SIGNIFICANT RISK AND THREAT FACTORS

BPH Bank Hipoteczny S.A. identified, measured, moni-tored and managed all types of risk in the Bank, in coopera-tion with the risk control and risk management units of Bank BPH S.A. Some of the solutions of risk control were specified by Bank BPH S.A., BPH Bank Hipoteczny S.A. approved and implemented such solutions.

The Bank identifies the following categories of risk:

− Market risk (currency and interest rate risk), defined as a risk of incurring a loss as a result of disadvantageous prices of financial instruments in the market. In order to diminish the level of market risk, the Bank adjusts its operations to external and internal precaution standards, while the expo-sure to the currency risk is monitored using the VaR (Value at Risk) method.

− Liquidity risk, defined as a risk of losing the capability of settling the liabilities in due time as a result of incoherence between their terms of payment and the maturity dates of receivables. In order to diminish the level of liquidity risk, the Bank also adjusts its operations to external and internal precaution standards and, for the purposes of managing and monitoring the liquidity, BPH Bank Hipoteczny S.A.

23

6

DIRECTIONS OF DEVELOPMENT AND KEY ELEMENTS OF THE BANK’S STRATEGY FOR 2006

In 2005, BPH Bank Hipoteczny S.A. continued the activi-ties included in the assumptions of the Bank’s strategy for years 2004-2006 and tried to achieve the results adopted in the financial plan for 2005.

In 2006, the Bank will adjust its operations to the existing and anticipated economic and legal conditions, expecta-tions of the chief shareholder and clients, as well as its own capabilities, taking into account particularly the quality of development, i.e. permanent improvement of the efficiency of operations.

Major financial goals for 2006 are:

Gross ROE - 20%

Cost/Income – below 35%

Perspectives for further development of the Bank are good.

The Bank has an attractive product offer and efficient processes. The real property market is developing and the need for long-term loans for commercial real property increases. There is also a permanent need in the market of loans for residential property, which are a significant instrument of loan portfolio diversification. Cooperation within the Group of BPH, particularly due to a high share of Bank BPH S.A. in the market of real property financing, is a positive sign for the success of the issue programme.

The achievement of the planned gross result in 2006 will be determined, among other factors, by the following assump-tions:

– increase of the economic growth rate – the increase of the Domestic Gross Product is estimated at about 4.6%;

– anticipated increase of investments of enterprises, improve-ment of the situation of households (gradual drop of the unemployment rate), stabilised low inflation supported by low level of market interest rates;

– activity of the Bank promoting sales, aimed at increasing the amount of loans, including such activities as: adjusting the offer to the needs and expectations of Clients, increas-ing the efficiency of the loan-granting process, etc.;

– strict control of administrative expenses to the end of keep-ing the costs of the Bank’s operations on the level close to the one achieved in 2005.

On the other hand, the potential decrease of the financial result may be determined, among other factors, by the an-ticipated pressure to reduce the margins, due to increasing competition in the banking market.

7

OWNERSHIP STRUCTURE, MANAGEMENT OF THE BANK, ORGANISATIONAL OR CAPITAL ASSOCIATIONS WITHIN THE GROUP

Ownership structure of the Bank’s share capitalOn 5 May 2005, the Special General Meeting of Sharehold-ers expressed their consent to raise the initial capital of the Bank by the amount of PLN 20,600,000.- to the amount of PLN 169,800,000.-, by the issue of shares of the “F” series in the number of 206 shares in private offering with no right of the shareholders to acquire the “F”-series shares in total. All shares were acquired by Bank BPH S.A.

On 18 November 2005, on the basis of information ob-tained from UniCredito Italiano S.p.A., Bank BPH S.A. notified BPH Bank Hipoteczny S.A. that due to acquisi-tion by UniCredit of control over Bayerische Hypo-und Vereinsbank Aktiengesellschaft (HVB) – former ultimate parent entity for Bank BPH S.A. and over belonging to HVB bank BA-CA – direct chief shareholder of Bank BPH S.A., pursuant to Article 26 Item 1 of the Banking Law, until obtaining by UniCredit a permit of the Com-mission for Banking Supervision for execution of the right to vote arising out of indirectly possessed shares of Bank BPH S.A., BA-CA may not successfully execute its right to vote arising out of the shares of Bank BPH S.A. As a consequence, from 18 November 2005 until obtaining by UniCredit the aforementioned permit of the Commission for Banking Supervision, Bank BPH S.A. will not be able to execute its right to vote arising out of the possessed shares of BPH Bank Hipoteczny S.A.

The nature of the Bank’s shares does not involve any limitations for ownership transfer or execution of the right to vote. All of them have the same scope of rights. Any limitations in this respect can follow exclusively from specific regulations, e.g. the Act on Banking Law, as it is the case for incapability of successful execution of the right to vote by UniCredit and its subsidiaries until obtaining the required permits.

Ownership structure of the Bank’s share capital

Name of the ShareholderShares Votes at the General Meeting of

Shareholders

Number % Number %

Bank BPH S.A. 1697 99.941 1697 99.941*Final Holding Sp. z o.o. 1 0.059 1 0.059TOTAL 1698 100 1698 100

* UniCredito Italiano S.p.A. (UniCredit) seated in Genoa (Italy) notified BPH Bank Hipoteczny S.A., that upon 17 November 2005, it acquired an indirect control over shares of the Bank entitling to 99.941% of votes at the general meeting of shareholders of the Bank.

24

Management bodiesThis section contains information on the persons forming the Man-agement Board and the Supervisory Board of BPH Bank Hipoteczny S.A. and information on the total value of salaries, prizes or benefits disbursed by the Bank to its managers and supervisors.

– Management BoardIn the period between 1 January 2005 and 31 December 2005, the Management Board of the Bank consisted of the following persons and received the annual remuneration amounting to:

The amount of remuneration of members of the Man-agement Board is approved by the Supervisory Board. Remuneration includes salary specified in the agreement and annual bonus paid in the amount established by the Supervisory Board and depending on the level of realisa-tion of the set tasks.

Agreements made between the Bank and the managerial personnel do not provide for any compensations for their resignation or dismissal from the post with no important reason or when their resignation or dismissal results from an acquisition of the Bank.

Management Board members and remuneration in 2005

Name and surname Performed function Annual remuneration* (PLN)

Irena Stocka President of the Management Board 487,902.00Jolanta Gładyś Vice President of the Management Board 448,414.76Jerzy Tofil Member of the Management Board 375,185.40

* Annual remuneration covers: salary, annual bonus and benefits disbursed in 2005 and due for 2005, as on the day of preparation of this report. Ad-ditionally, we inform that the remuneration does not include the amounts of additional bonuses Members of the Management Board of the Bank for 2004 in the amount of PLN 230,000 that reduce the financial result for 2004 and were disbursed in 2005. The aforementioned amounts include, among others, covering the costs of living out of the place of permanent residence and life insurance.

– Supervisory BoardIn the period between 1 January 2005 and 31 December 2005, the Supervisory Board of BPH Bank Hipoteczny S.A. consisted of the following persons:

votes at the General Meeting of Shareholders of Bank BPH S.A. However, until obtaining a permit of the Com-mission for Banking Supervision for execution of the right to vote and until fulfilling other obligations, BA-CA may not successfully execute the right to vote arising out of the shares of Bank BPH S.A.

– Transactions with affiliated entitiesThe Bank realises transactions with its parent entity (Bank BPH S.A.), as well as with entities affiliated within the Group of BPH, HVB and UCI. Transactions with affili-ated entities are realised in the course of standard busi-ness operations. They cover mainly loans, deposits and currency exchange transactions. Detailed information on transactions with affiliated entities, as well as transactions with managerial personnel and employees of BPH Bank Hipoteczny S.A. are presented in Note 35 of the Statement of Accounts.

Supervisory Board members in 2005

Name and surname Performed function

Wojciech Sobieraj President of the Supervisory BoardMariusz Grendowicz Vice President of the Supervisory BoardMirosław Boniecki Member of the Supervisory BoardElżbieta Ratajczak Member of the Supervisory BoardCarl-Norman Voekt Member of the Supervisory Board

The General Meeting of Shareholders which took place on 29 June 2005, appointed the aforementioned persons members of the Supervisory Board for the new term.

Members of the Supervisory Board do not receive any remuneration for their function in the Supervisory Board.

Organisational or capital associations within the GroupThe Bank has been notified that UniCredito Italiano S.p.A. (UniCredit or UCI), upon 17 November 2005, acquired 705,108,946 shares in the initial capital of Bayerische Hypo- und Vereinsbank AG (HVB), entitling to execute the right to 93.93% of the total number of votes at the General Meeting of Shareholders of HVB. Therefore, UniCredit acquired control over HVB – former parent entity for Bank BPH S.A. and over belonging to HVB bank Austria Credi-tanstalt AG (BA-CA) - direct chief shareholder of Bank BPH S.A. As a result of the aforementioned acquisition, UniCredit owns 20,397,585 of shares constituting 71.03% of the initial capital and entitling to execute the right to 20,397,585 of votes being 71.03% of the total number of

25

– Significant agreements made between affiliated entities

In 2005, BPH Bank Hipoteczny S.A. made with Bank BPH S.A. the following agreements:

– Credit line agreement

for the total amount of 242 million EUR (934 million PLN), for the purposes of financing the loan activity of the Bank. Pursuant to the agreement, disbursement of the credit is to be realised in tranches and the interests are ac-crued at the variable interest rate. Term of full repayment is established on 28 December 2006.

As on the end of the year, the liability due to this credit amounted to 504,187 thousands PLN. Term of payment of this tranche did not exceed 1 month.

– Subissue agreement

made on 4 November 2005, an agreement on subissue of mortgage bonds of the LZI02 series of the value amounting to 400 million PLN. The agreement provides for the purchase of mortgage bonds of the LZI02 series by Bank BPH S.A. on its own behalf and at its own expense, for the purposes of their further resale to Investors in the primary market.

The aforementioned agreements has been deemed signifi-cant, as their value exceeds 10% of the equity capital of the Bank.

8

ADDITIONAL INFORMATION

Agreements significant for the Bank concluded after thebalance sheet dateAgreements concluded after the balance sheet date of the value exceeding 10% of the equity capital of the Bank:

– Credit line agreement

signed in February 2006 by and between BPH Bank Hipotec-zny S.A. and Bayerische Landesbank. The agreement is con-cluded for the amount of 60 million EUR. Pursuant to the provisions of the agreement, the Bank used the credit in one disbursement for the purposes of its loan granting activity.

Term of repayment - 24 February 2009

– Subissue agreement

made on 28 February 2006 with Bank BPH S.A., an agree-ment on subissue of mortgage bonds of the LZI03 series. Pur-suant to the aforementioned agreement, Bank BPH S.A. shall cover with its subissue liability the issued mortgage bonds of the value not exceeding 200 million PLN.

– Loan agreement

On 30 January 2006, the Bank signed a loan agreement with a Client for the total amount of 37 million PLN. The interest of the loan is based on 6M WIBOR increased by the margin of the Bank. Scheduled date of the loan repay-ment is 31 July 2021.

Contingent liabilities– Initiated court proceedings

As on 31 December 2005, there are no proceedings initi-ated by court or any state administration body concern-ing any liabilities or debts of the Bank whose value would amount to at least 10% of the equity capital of the Bank.

Total value of all court proceedings in progress amounts to 22,021 thousands PLN, which constitutes 10.60% of the equity capital of the Bank. The aforementioned amount is the value of the subject of dispute in court proceedings brought by the Bank.

As on 31 December 2005, there are no proceedings initi-ated by court or any state administration body in which the Bank would act as a respondent.

In 2005, the Bank issued 9 execution titles for the total amount of 4,975 thousands PLN. The value of property of loan taking entities established as security (mortgage), for which execution titles were issued, amounted to 6,574 thousands PLN.

– Contingent liabilities to grant loans

The Bank has liabilities to grant loans for the total amount of 23,683 thousands PLN.

– Other liabilities due to off-balance sheet transactions

The value of liabilities due to transactions using current and fixed term financial instruments amounts to 1,120,375 thousands PLN.

In 2005, the Bank did not grant any warranties or sureties.

Other information– The Bank has not entered into and does not have any

knowledge of any agreements due to which any changes in the proportions of shares owned by current shareholders and bondholders might occur in the future.

– No significant agreements between the Bank and the Cen-tral Bank or supervisory bodies have been signed.

Entity entitled to audit the statement of accountsOn 21 November 2005, the Bank signed with KPMG Audyt Spółka z o.o. an agreement on auditing the statement of accounts. Total amount of remuneration specified in the aforementioned agreement is PLN 103,700.00 gross. First instalment amounting to PLN 51,850.00 has been paid. The second instalment, pursuant to the agreement, will be paid after the final version of the auditor’s opinion and report is submitted and will amount to PLN 51,850.00.

The entity that performed the audit of the statement of ac-counts of the Bank in 2004 was KPMG Audyt Spółka z o.o., and the total amount of remuneration was PLN 89,182.00 gross.

In 2005, the Bank signed with KPMG Sp. z o.o. an agree-ment on advisory services.

26

9

STATEMENTS OF THE BOARD

Principles of corporate governance and social responsibilityIn its operations, BPH Bank Hipoteczny S.A. follows the principles of social responsibility and is sensitive to the needs of clients and shareholders.

The Bank fully implements the principles specified in the following documents adopted by the Management Board of the Bank:

– “Instructions – Conduct of employers and respecting the regulations in making transactions connected with real property”;

– “Regulations on granting loans to and opening fixed-term deposit accounts for shareholders, members of manage-ment bodies and employees”;

– “Compliance regulations on trade with securities issued by the Bank”.

Accuracy and reliability of the presented statementsAccording to their best knowledge, the Management Board of BPH Bank Hipoteczny S.A. presents the annual finan-cial data and comparative data for 2004. The data has been prepared in accordance with the prevailing accounting principles and accurately, reliably and clearly reflect the property and financial position of the Bank, as well as the achieved financial result. The annual management report included herein presents a true image of development, achievements and position of the Bank, including a descrip-tion of significant risks and threats.

Irena Stocka President of the Management Board

Jolanta Gładyś Vice President

of the Management Board

Jerzy Tofil Member of the Management Board

Warsaw, 24 March 2006

OPINIA I RAPORT BIEGŁEGO REWIDENTA

OPINION AND REPORT OF THE AUDITOR

28

�����

BPH Bank Hipoteczny S.A.

Opinia i RaportNiezale�nego Bieg�ego Rewidenta

Rok obrotowy ko�cz�cy si�31 grudnia 2005 r.

KPMG Audyt Sp. z o.o. Ta opinia zawiera 2 strony

Raport uzupe�niaj�cy opini� zawiera 12 stronOpinia niezale�nego bieg�ego rewidenta

oraz raport uzupe�niaj�cy opini�z badania sprawozdania finansowego

za rok obrotowy ko�cz�cy si�31 grudnia 2005 r.

29

OPINIA NIEZALE�NEGO BIEG�EGO REWIDENTA

Dla Walnego Zgromadzenia Akcjonariuszy BPH Banku Hipotecznego S.A.

Przeprowadzili�my badanie za��czonego sprawozdania BPH Banku Hipotecznego S.A.z siedzib� w Warszawie, ul. Chmielna 132/134, 00-805 Warszawa, na które sk�ada si� bilans sporz�dzony na dzie� 31 grudnia 2005 r., który po stronie aktywów i pasywów wykazuje sum�1.587.844 tys. z�otych, rachunek zysków i strat za rok obrotowy ko�cz�cy si� tego dniawykazuj�cy zysk netto w kwocie 27.845 tys. z�otych, zestawienie zmian w kapitale w�asnym za rok obrotowy ko�cz�cy si� tego dnia wykazuj�ce zwi�kszenie kapita�u w�asnego o kwot�15.781 tys. z�otych, rachunek przep�ywów pieni��nych za rok obrotowy ko�cz�cy si� tego dniawykazuj�cy zmniejszenie stanu �rodków pieni��nych netto o kwot� 7.920 tys. z�otychoraz informacje dodatkowe o przyj�tych zasadach (polityce) rachunkowo�ci oraz inne informacje obja�niaj�ce.

Zarz�d Banku jest odpowiedzialny za prawid�owo�� ksi�g rachunkowych oraz rzetelno��i jasno�� sprawozdania finansowego sporz�dzonego zgodnie z Mi�dzynarodowymi StandardamiSprawozdawczo�ci Finansowej, które zosta�y zatwierdzone przez Uni� Europejsk�, a w sprawach nieuregulowanych powy�szymi standardami, zgodnie z wymogami ustawy z dnia 29 wrze�nia 1994 r. o rachunkowo�ci (Dz. U. z 2002 r., nr 76, poz. 694 z pó�niejszymizmianami) oraz wydanymi na jej podstawie przepisami wykonawczymi jak równie� wymogamiodnosz�cymi si� do emitentów papierów warto�ciowych dopuszczonych lub b�d�cychprzedmiotem ubiegania si� o dopuszczenie do obrotu na rynku pozagie�dowym. Naszymzadaniem jest, w oparciu o przeprowadzone badanie, wyra�enie opinii odno�nie tego sprawozdania finansowego oraz prawid�owo�ci ksi�g rachunkowych i dokumentacjiuzupe�niaj�cej, stanowi�cych podstaw� jego sporz�dzenia.

Badanie sprawozdania finansowego przeprowadzili�my stosownie do postanowie� rozdzia�u7 ustawy z dnia 29 wrze�nia 1994 r. o rachunkowo�ci, norm wykonywania zawodu bieg�egorewidenta, wydanych przez Krajow� Rad� Bieg�ych Rewidentów w Polsceoraz Mi�dzynarodowych Standardów Rewizji Sprawozda� Finansowych. Przepisy te wymagaj�, aby badanie zosta�o zaplanowane i przeprowadzone w taki sposób, aby uzyska�racjonaln� pewno��, �e sprawozdanie finansowe nie zawiera istotnych nieprawid�owo�ci.Badanie obejmuje sprawdzenie w oparciu o metod� wyrywkow� dowodów i zapisów ksi�gowych, z których wynikaj� kwoty i informacje zawarte w sprawozdaniu finansowym.Badanie obejmuje równie� ocen� poprawno�ci stosowanych zasad rachunkowo�ci, znacz�cychszacunków dokonanych przez Zarz�d Banku oraz ocen� ogólnej prezentacji sprawozdania finansowego. Wyra�amy przekonanie, �e przeprowadzone przez nas badanie stanowi wystarczaj�c� podstaw� dla naszej opinii.

30

Naszym zdaniem, za��czone sprawozdanie finansowe BPH Banku Hipotecznego S.A. zosta�osporz�dzone na podstawie prawid�owo prowadzonych, ksi�g rachunkowych oraz dokumentacjiuzupe�niaj�cej i przedstawia rzetelnie i jasno, we wszystkich istotnych aspektach, sytuacj�maj�tkow� i finansow� Banku na dzie� 31 grudnia 2005 r., wynik finansowy oraz przep�ywypieni��ne za rok obrotowy ko�cz�cy si� tego dnia 31 grudnia 2005 r. zgodniez Mi�dzynarodowymi Standardami Sprawozdawczo�ci Finansowej, które zosta�y zatwierdzone przez Uni� Europejsk�, a w sprawach nieuregulowanych powy�szymi standardami, zgodniez wymogami ustawy z dnia 29 wrze�nia 1994 r. o rachunkowo�ci oraz wydanymi na jej podstawie przepisami wykonawczymi jak równie� wymogami odnosz�cymi si� do emitentówpapierów warto�ciowych dopuszczonych lub b�d�cych przedmiotem ubiegania si� o dopuszczenie do obrotu na rynku pozagie�dowym, oraz jest zgodne z wp�ywaj�cymi na tre��sprawozdania finansowego przepisami prawa i postanowieniami statutu Banku.

Ponadto, zgodnie z wymogami ustawy z dnia 29 wrze�nia 1994 r. o rachunkowo�ci,stwierdzamy, �e sprawozdanie z dzia�alno�ci Banku uwzgl�dnia, we wszystkich istotnychaspektach, informacje, o których mowa w art. 49 powy�szej ustawy oraz wymogiRozporz�dzenia Ministra Finansów z dnia 19 pa�dziernika 2005 r. w sprawie informacjibie��cych i okresowych przekazywanych przez emitentów papierów warto�ciowych(Dz.U. z 2005 r., nr 209, poz. 1744) i s� one zgodne z informacjami zawartymi w sprawozdaniu finansowym.

....................................................... .......................................................Bieg�y rewident nr 9941/7390,Bo�ena Graczyk

Za KPMG Audyt Sp. z o.o. ul. Ch�odna 51, 00-867 Warszawa Bieg�y rewident nr 9941/7390 Bo�ena GraczykCz�onek Zarz�du

.......................................................Za KPMG Audyt Sp. z o.o. ul. Ch�odna 51, 00-867 Warszawa Robert J. WiddowsonDyrektor

Warszawa, 24 marca 2006 r.

31

����

BPH Bank Hipoteczny S.A.

Raport uzupe�niaj�cy opini�z badania

sprawozdania finansowegoRok obrotowy ko�cz�cy si�

31 grudnia 2005 r.

KPMG Audyt Sp. z o.o. Raport uzupe�niaj�cy opini� zawiera 13 stron

Raport uzupe�niaj�cy opini�z badania sprawozdania finansowego

za rok obrotowy ko�cz�cy si�31 grudnia 2005 r.

32

� BPH Bank Hipoteczny S.A.Raport uzupe�niaj�cy opini� z badania sprawozdania finansowego

za rok obrotowy ko�cz�cy si� 31 grudnia 2005 r.

Spis tre�ci

1 Cz��� ogólna raportu 31.1 Dane identyfikuj�ce Bank 31.2 Dane identyfikuj�ce bieg�ego rewidenta 31.3 Podstawy prawne 31.4 Informacje o sprawozdaniu finansowym za poprzedni rok obrotowy 61.5 Zakres prac i odpowiedzialno�ci 6

2 Analiza finansowa Banku 82.1 Ogólna analiza sprawozdania finansowego 82.2 Wybrane wska�niki finansowe 102.3 Interpretacja wska�ników 10

3 Cz��� szczegó�owa raportu 113.1 Ksi�gi rachunkowe i ochrona danych 113.2 Inwentaryzacja 113.3 Stosowanie si� do norm ostro�no�ciowych 113.4 Wska�niki istotno�ci przyj�te do badania 113.5 Informacje dodatkowe o przyj�tych zasadach (polityce) rachunkowo�ci oraz inne

informacje obja�niaj�ce 113.6 Sprawozdanie z dzia�alno�ci Banku 123.7 Informacja o opinii niezale�nego bieg�ego rewidenta 12

2

2

33

� BPH Bank Hipoteczny S.A.Raport uzupe�niaj�cy opini� z badania sprawozdania finansowego

za rok obrotowy ko�cz�cy si� 31 grudnia 2005 r.

1 Cz��� ogólna raportu

1.1 Dane identyfikuj�ce Bank

1.1.1 Nazwa Banku

BPH Bank Hipoteczny S.A.

1.1.2 Siedziba Banku

ul. Chmielna 132/134 00-805 Warszawa

1.1.3 Rejestracja w Krajowym Rejestrze S�dowym

Siedziba s�du: S�d Rejonowy dla Miasta Sto�ecznego Warszawy, XIX Wydzia� GospodarczyKrajowego Rejestru S�dowego

Data: 12 lipca 2001 r. Numer rejestru: 0000027441

1.1.4 Rejestracja w Urz�dzie Skarbowym i Wojewódzkim Urz�dzie Statystycznym

NIP: 527-10-28-697 REGON: 011183360

1.2 Dane identyfikuj�ce bieg�ego rewidentaKPMG Audyt Sp. z o.o. ul. Ch�odna 51, 00-867 Warszawa

KPMG Audyt Sp. z o.o. jest podmiotem uprawnionym do badania sprawozda� finansowychwpisanym na list� pod numerem 458.

1.3 Podstawy prawne

1.3.1 Kapita� zak�adowy

BPH Bank Hipoteczny S.A. z siedzib� w Warszawie zosta� za�o�ony zgodnie z aktemnotarialnym z dnia 24 sierpnia 1995 r. na czas nieokre�lony.

Na mocy decyzji Nadzwyczajnego Walnego Zgromadzenia Akcjonariuszy 5 maja 2005 r.nast�pi�o podwy�szenie kapita�u zak�adowego Spó�ki z kwoty 149.200 tys. z�. o kwot� 20.600 tys. z�. do kwoty 169.800 tys. z�.

Kapita� zak�adowy Banku na dzie� 31 grudnia 2005 r. wynosi� 169.800 tys. z�. i dzieli� si� na 1.698 akcji o warto�ci nominalnej 100 tys. z� ka�da.

3 3

34

� BPH Bank Hipoteczny S.A.Raport uzupe�niaj�cy opini� z badania sprawozdania finansowego

za rok obrotowy ko�cz�cy si� 31 grudnia 2005 r.

Struktura w�asno�ciowa Banku wed�ug stanu na dzie� 31 grudnia 2005 r. przedstawia�a si�nast�puj�co:

Nazwa akcjonariusza Ilo�� akcjiIlo��

g�osów(w %)

Warto��nominalnaakcji z�'000

Udzia� w kapitale

zak�adowym(w %)

Bank BPH Spó�ka Akcyjna 1.697 99,94% 1.697.000 99,94%Final Holding sp. z o.o. 1 0,06% 1.000 0,06%

1.698 100,0% 1.698.000 100,0%

1.3.2 Jednostki powi�zane

Bank nale�y do grupy kapita�owej Grupa Kapita�owa Banku BPH S.A.

1.3.3 Kierownik jednostki

Funkcje kierownika jednostki sprawuje Zarz�d.

W sk�ad Zarz�du Banku na dzie� 31 grudnia 2005 r. wchodzili:

� Irena Stocka – Prezes Zarz�du� Jolanta G�ady� – Wiceprezes Zarz�du� Jerzy Tofil – Cz�onek Zarz�du

W porównaniu ze stanem z dnia 31 grudnia 2004 r. w sk�adzie Zarz�du nie wyst�pi�y zmiany.